DOWNLOAD

DATE

MEET THE AUTHORS

Contact

After years of decline, telecom operators are being lured by promising opportunities around the smart-home. But empirical experience reveals that product-focused activities struggled to contribute to top line growth, and will continue to do so, whereas end-to-end smart-life services seem to be the solution: they are attractive to high-value convergent customers, contribute higher margins, are easier to market, adapt to telcos’ unique assets as service providers and present considerable growth potential. With their assets as well as natural and excellent position to partner with equipment manufacturers and home-service aggregators, telecom operators have the keys to effectively provide the long-promised “smart-life” service at home

After years of revenue decline for telcos, devicebased smart-home initiatives were unable to deliver on their promises

Over the last five years, the European telecom industry has seen a substantial decline in revenues. While most drivers of this decline have reached their culminating point1 , the growth perspectives are not enthusiastic for the years to come: considering the maturity levels of the fixed broadband, mobile broadband and digital TV markets, and the revenue risk from discount-driven bundling, a slight growth or stabilization of revenues is expected at best.

Therefore, telecom operators have been looking for new revenue opportunities. With its strong growth forecasts of €2 bn in 2015 to €10 bn in 2020 in Europe2 , the smart-home appears particularly appealing. The golden question becomes how and with which value proposition telecom operators can get a share of the market.

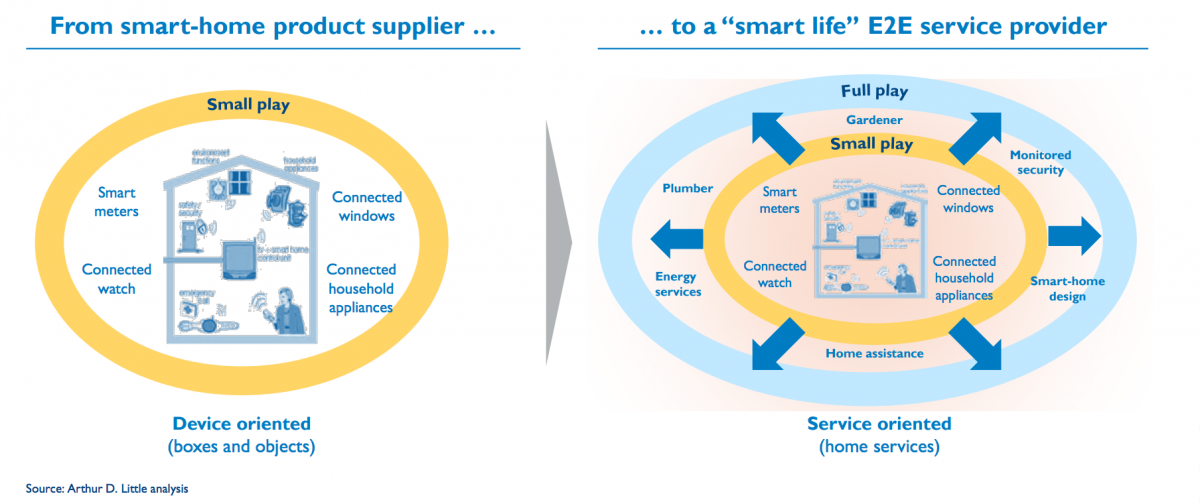

Initially, operators entered the smart-home business by selling home-related connected devices, possibly complementing them with basic value-added services. Willing to disrupt the market and rapidly increase adoption rates, they opted for low-cost and mass-market positioning. Their offerings were usually characterized by being device-centric and promoting self installation. Furthermore, they generally addressed only one customer need (security, light, temperature control, etc.) and required self-action and self-monitoring from the client, e.g. the client needing to check the security/automation of his house himself. In addition, the user usually was responsible for maintenance and upgrading of his devices.

As expected, customers welcomed these “small-play,” devicecentric solutions with mixed feelings - many perceived them as “geeky” products that were complex to manage and with limited value. Consequently, results were mostly disappointing for telecom operators: weak penetration (<1% of customer base), low pricing (but still expensive compared to the value created), low usage, low loyalty and overall limited revenue generation and profit potential.

Capturing the smart-life value potential requires a more ambitious proposition

Currently, customers are still facing three unmet needs, and without addressing these, any smart-life value proposition has little chances of convincing them:

- Helping customers equip their homes, i.e. help them navigate through the multitude of available connected objects and select the most relevant ones, assist the customer to manage the compatibility & interoperability of devices and to make choices that are at least future proof, and eventually ensure simple installation processes

- Coach the customer on how to use effectively and efficiently their connected objects, i.e. providing tailored use cases and proactive support lines or tips, as well as offering community practice sharing (from simple forums to gamification)

- Act/react when needed: sensors are fine, but valueless if no action is undertaken. Providing non-automated services at the right time is the only way of moving from a smarthome product to a smart-life experience:

- Upon request, provide home-related professionals (painters, plumbers, electricians, security agents, etc.) at fair quality/cost conditions

- Proactively maintain or repair, e.g. schedule preventive or predictive maintenance (wanted or imposed) for chimneys, batteries, gutters, etc.

- React in cases of incidents: sensor triggering-specific action/intervention, e.g. call for police or firemen, or an electrician, gardener or neighbor

In summary, a “smart-life service” provider would offer a “burden-avoidance” solution to customers, bringing life serenity. Through its wide portfolio of smart-life end-to-end services, it could aim at addressing close to 90% of events related to customer needs at home, with a rapid solution based on human interaction.

Building on this vision, several telecom operators started to implement the building blocks of the home life-service provider. In 2011, Comcast launched the Xfinity Home offering around home security. Since then, its ambition has widened to become the single point of contact for all matters involving home-control systems (offering energy control, lighting and shade control, and home access control services), with price tags ranging between $20 and $40 per month.

Going a step further, PCCW-HKT provides home entertainment (e.g. audio-visual products and installation service), home automation and e-health services (e.g. install and maintenance of post-operative care devices) to its Hong Kong customers. Offering a service that is less expected from a telecom operator, PCCW-HKT is also active in home-networking and smart-living consultancy services, helping customers to design and build smart-homes.

It is interesting to note that so far most successful smart-life full-play offerings started with end-to-end monitored security services, extending the scope only after gaining customers’ trust on this highly emotive topic.

High value-creation potential

Our evidence reveals that customers highly value a zero burden solution offered by a smart-life service at home, as these require minimal effort to adopt and provide tangible benefits in the short term. Such a notion is also quickly growing in the automotive world, with an increase in car leasing, including maintenance and assistance; “car-as-a-service” to “home-as-a-service” appears to be an obvious path.

In simple terms, the addressable end-user market relates primarily to 40- to 70-year-old end users, many of whom are already interested in the convenience fixed-mobile convergence offers and have a high propensity to pay for reactive human services that ensure life serenity.

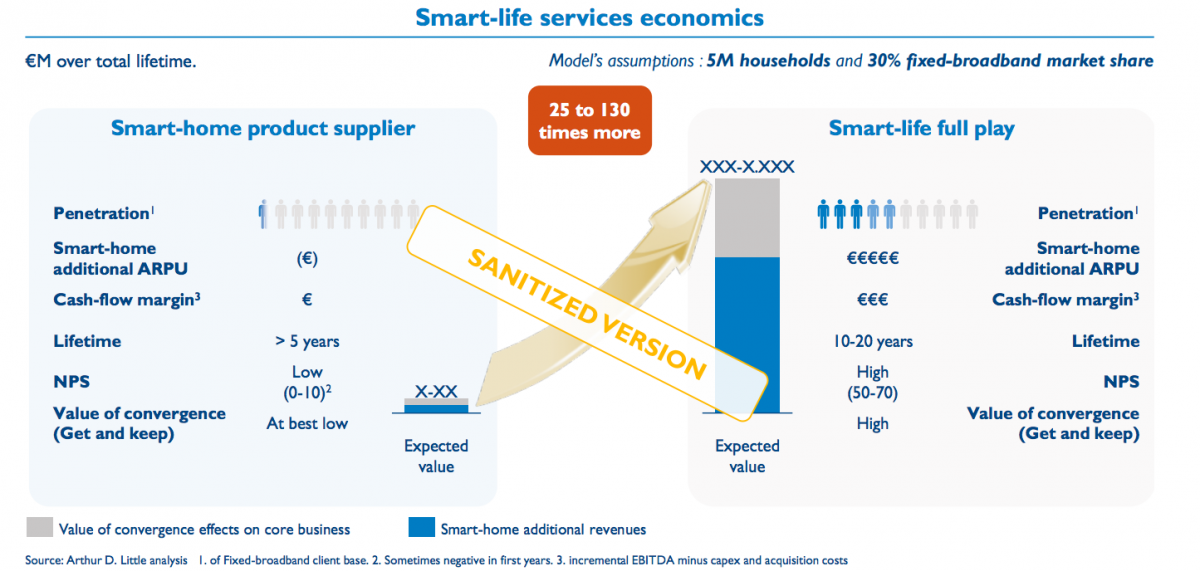

The most tangible value creation is driven by the revenues and profitability of end-to-end smart-life services.

Portfolio components such as home security and automation, energy control and home-assistance services are able to claim ARPU levels ranging from €20 to €80 per month. Empirical experiences show that telecom operators can easily generate incremental revenues at around 20% EBITDA via a partnership model3 . With no need to cut prices of home-services already provided to the market, profitability is maintained (or even increased), facilitating the development of a wide portfolio of partnerships.

Indirect value creation comes from a substantial increase of net promoter scores (NPSs) and retention. Smart-life full-play services benefit from considerable NPSs ranging from 50 to 70, whereas telecom services typically score between -20 and 30. Furthermore, this high end-user satisfaction is linked to a longterm home refurbishment cycle (10 to 20 years) securing very low churn levels.

A last source of value creation comes from the increasing reliance on core telecom services, which drives substantial opportunities for cross-selling and up-tiering, with limited acquisition costs (i.e. captive base). The stickiness of smartlife services tends to further reduce churn on core telecom services.

In all, the smart-life service provider offers the highest organic growth opportunity in the B2C market. No other current opportunities are as sizable. Smart-life services could generate 25 to 130 times more value than the current device-driven smallplay offerings (Figure above).

Telecom operators are ideally positioned to play this enabler role

Benefiting from dual legitimacy, telecom operators are uniquely positioned to capture this growth potential.

Telecom operators are recognized as central players in ensuring the connectivity and management of all connected devices in the customer’s home LAN. In many markets, most telecom operators have reputations as trusted companies providing fair conditions and service quality. This high level of trust is essential, as the smart-life service provider is expected to be active in the heart of the client’s home. Besides, with the emergence of a plethora of connected devices with low customer support available, customers are likely to turn to the telco’s call center when facing problems anyhow.

On the ecosystem side, telecom operators benefit from strong legitimacy as well: selling products to households, providing relevant care and managing the billing relationship are in their DNA. On top of that, their strong local presence positions them ideally to take the lead and set up the local ecosystem and partnership management.

Enabling smart-life services is also a strategic survival move for operators: it prevents other actors (GAFAM5 , utility and postal companies, etc.) from getting too close to their connectivity services, which could lead operators into the “dumb pipe”, corner or even bring these other players into the resale of fixed and mobile network services.

Partnerships will be key to succeed

To optimize return on investments, reduce product development risks and improve the credibility of the solution for the customer, telecom operators will need to develop the right partnership strategies. Their aim should not be to replace consumer electronics companies or home-service providers, but rather to enable home services via partnerships.

Multiple home-assistance service providers exist today, operating strong networks of home-repair professionals and sub-contractors in many domains: plumbing, heating, electrical related, electronics, etc. Examples of home-service aggregators include HomeServe, Dixons and Multiasistencia. The latter, the Spanish leader in management and repair of claims for insurance and utility companies, leverages its large network of sub-contractors to resolve end users’ insurance claims. Also noteworthy, from car to home again, the last months have seen the development of a plethora of Uber-like and collaborative economy apps for those home-services, which will probably soon land with a set of new home-service leaders.

Partnerships with home-service aggregators are not complex to set up. Similar to telecom operators, home-service aggregators have a local dimension. Some have built strong brand images, which, combined with telcos, can strengthen the credibility of the offering to clients.

Besides, telecom operators should consider partnering with consumer electronics manufacturers to design and build platforms able to connect and manage all the smart devices in a household. Nokia, for instance, announced the release by end of 2016 of its smart-home solution oriented for telecom operators, including a hub, gateway, and mobile application. With such equipment partnerships, telecom operators can move out of the device-based and small-play considerations and focus on valueadded services with higher margins.

In all, with proper strategies and investments, the right level of executive commitment and ongoing support, the smart-life service provider has considerable value-creation potential. It is time to dare.

Insight for executives

- Small-play smart-home initiatives based on devices sales, self-installation and self-action mostly failed at generating value.

- Becoming an end-to-end service provider, leveraging smart devices to provide a quick, no-burden reaction to everyday problems in the home, is desirable to high-value customers.

- End-to-end smart-life services could generate considerable margin growth to operators, 25 to 150 times higher than small-play initiatives.

- Some telecom operators have started moving, while GAFAM and other players (utilities, postal actors, homeservice aggregators) are looking to position themselves.

- Telecom operators are uniquely positioned to take the smartlife enabler role, benefiting from their client and ecosystem legitimacy. It is time to dare!

- To ensure fast go-to-market and reduce commercial and investment risks, operators should develop their partnership strategies with both home-service aggregators and consumer-electronics manufacturers that provide smarthome gateways

Unlock a Powerful Difference

RELATED INFORMATION

Smart Home: Bridging the Islands

The world's largest internet players, such as Microsoft, Google, Apple and Amazon, are also investing significantly in Smart Home - but have they really cracked customer requirements? Arthur D.…

Catching the Smart Home Opportunity

In this report, Arthur D. Little reviews the key trends driving the potential for Smart Home solutions, presents an overview of four main segments and provides recommendations for telecom operators…

Low carbon London

A Victorian terraced home with a twist, No.1 Lower Carbon Drive, opened to the public today to provide Londoners with examples of ways in which they can alter their homes and domestic lifestyles to…