17 min read • Financial services

Asset as a service

Transforming ownership and business models promises significant value

Executive Summary

Asset-as-a-service (AaaS) business models are increasingly being adopted across multiple industry sectors, driven by a growing demand from users of such assets as machinery and equipment. In the AaaS model, users no longer purchase assets; instead, they are billed for the actual benefit they receive. However, to introduce AaaS business models successfully, parties must meet several conditions.

AaaS models require the use of sensors to collect Internet of Things (IoT) and telemetry data, which is then shared and processed via networked systems, and provide a basis for calculating actual usage and current asset value. Automated billing, invoicing, and payment, as well as integration with existing enterprise resource planning systems, are important factors for scaling AaaS models.

AaaS delivers both benefits and implications for the existing business models of all parties involved. These parties include the equipment manufacturer, the user, and investors, such as financial institutions that traditionally provide loans or leasing models.

But a key question arises: which of the parties involved own the assets, receive cash flows from their use, and bear utilization risks? The answer will depend on each player’s ability to transform — along with their willingness to change their business models. The outcome is also closely linked to financing design, which can be structured differently depending on the business model, preferences, and type of asset. This Report describes various options and explains the benefits and risks for everyone involved.

1

Financing: Then & now

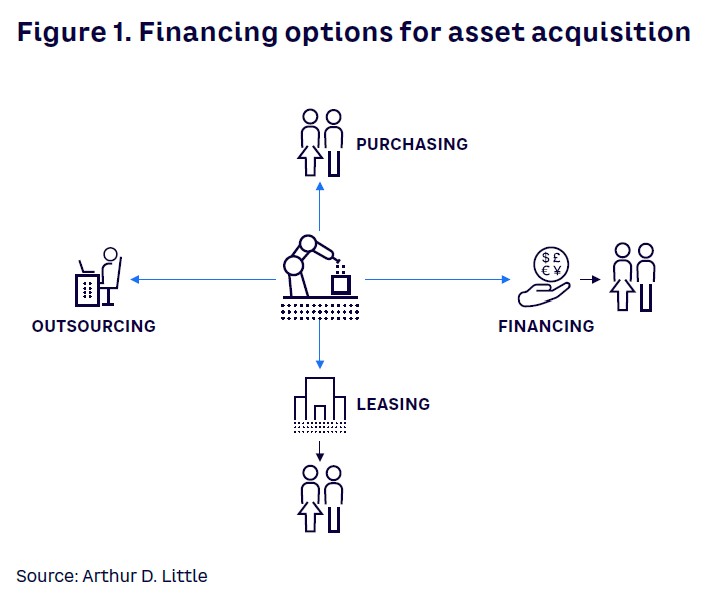

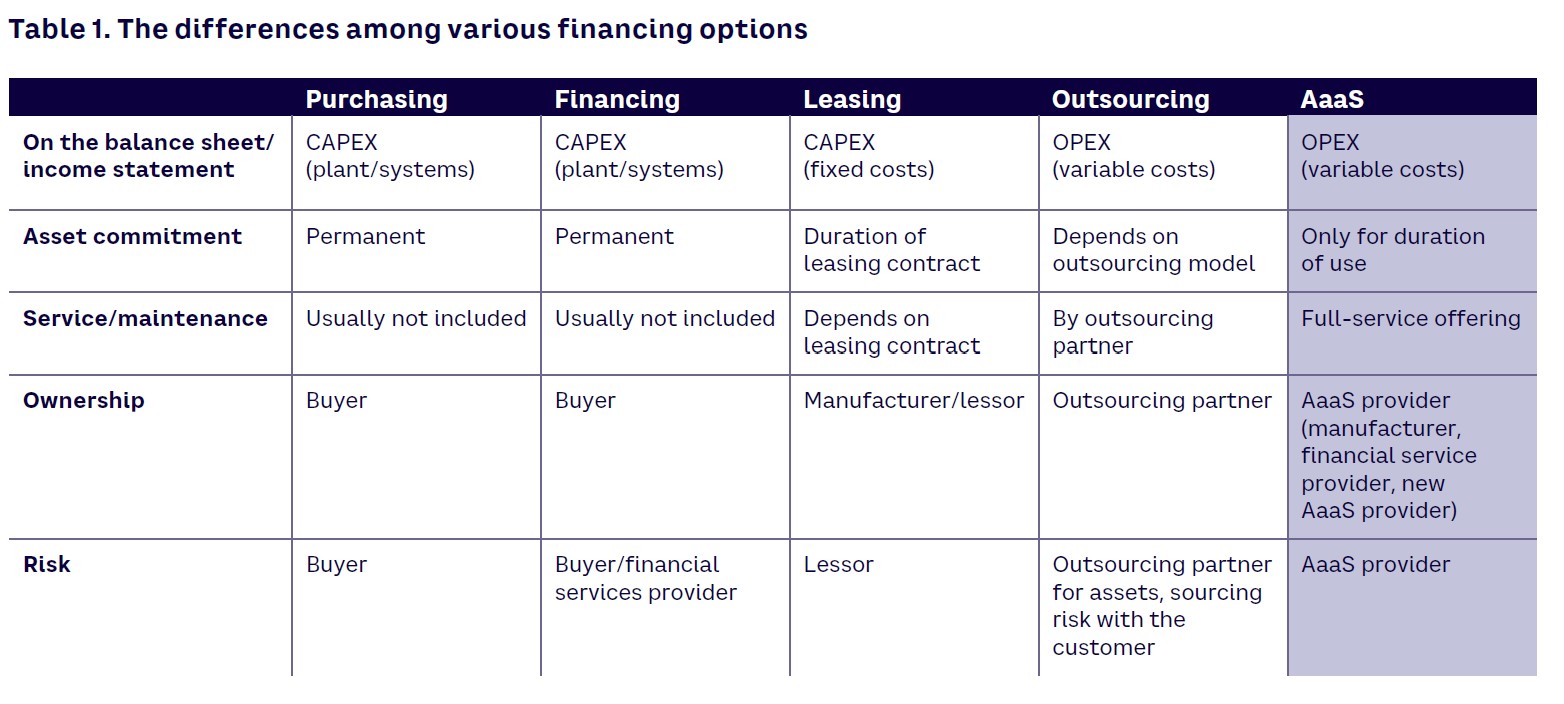

Until now, customers looking to finance an asset have traditionally had four options: purchasing, financing, leasing, or outsourcing (see Figure 1). These four options have major differences in how they are designed (see Table 1).

In the cases of purchasing and financing, the asset becomes part of a company’s assets. With financing, the company pays a fixed sum to a financial services provider over a set length of time. The other two variants (leasing and outsourcing) are more flexible and less capital-intensive. They differ primarily in the type and measurement of payment for the use of the asset.

Boosting sales through leasing dates back to the 19th century. Essentially, the leasing partner purchases the asset, with the end user company paying the partner at a fixed rate over a set term. In contrast to simply renting, the purchaser can then buy the item for a residual price at the end of the term.

The outsourcing of services, previously performed internally, has been taking place since the 1960s. Contracts specify the duration and subject matter of the external service provision, while the outsourcing partner retains ownership of the assets used within the contract.

The future belongs to AaaS

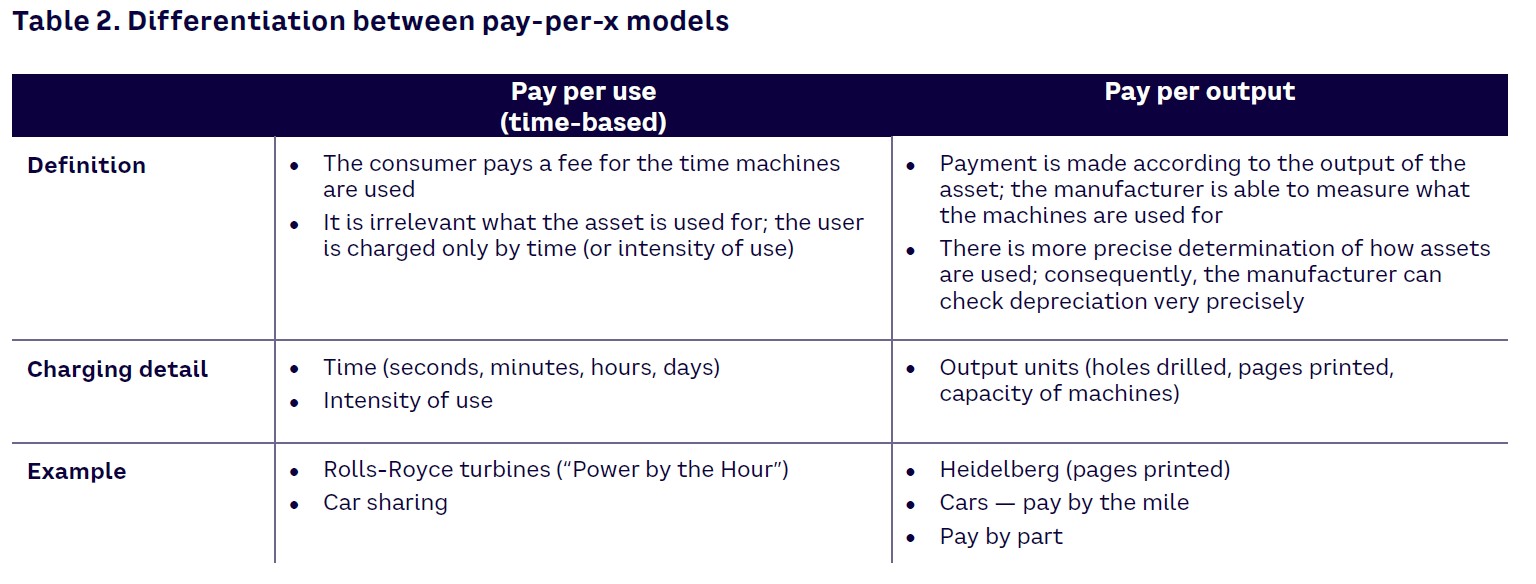

In AaaS business models, the traditional division of roles among manufacturers, buyers, and financial service providers is newly defined. With AaaS, assets are no longer purchased, financed, or leased by the user; instead, they are purchased on a pay-per-use or pay-per-output basis, where users pay only for actual use (see Table 2). These new business models transfer the familiar concepts of other “as-a-service” models, which are already common for software solutions, to tangible assets such as machinery and equipment.

In AaaS models, billing is based on usage rather than at a flat rate. This means that customers/users have much greater flexibility in how they use assets. For example, they can just use them for a short time (e.g., project-based) and then relinquish the asset once it is no longer needed. This generates new opportunities for investors — both on the debt and equity side — by creating new asset classes. These are attractive options, especially given the current limited investment opportunities and liquidity in the market.

The value trend and thus the current fair value of a machine must show a clear correlation to operating hours, capacity utilization, or the number of units produced.

AaaS business models offer advantages for users and also transfer the risk of asset ownership to AaaS providers. These adjustments also enable new business models for asset manufacturers and financial service providers. For manufacturers, the AaaS business model opens up new revenue streams, some of which promise higher margins than with traditional sales or rental businesses.

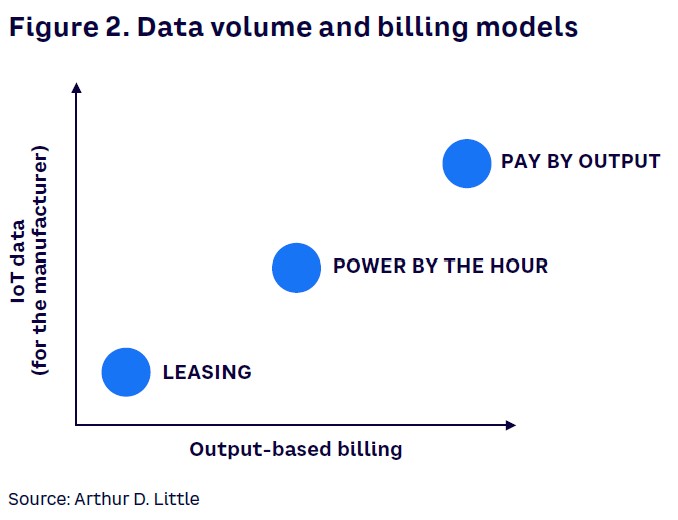

AaaS models are already being used in certain industries, particularly in mechanical and plant engineering. For example, Rolls-Royce is considered one of the first engineering companies to offer pay-per-use models with its “Power by the Hour” performance-based contracts for its jet engines. Other examples of companies integrating IoT technology with pay-per-use models include machinery and equipment manufacturers DMG Mori and Trumpf.

However, beyond these examples, AaaS business models are not yet established across all industries, with wider usage limited by factors such as a lack of process-integration options. However, ongoing digitalization and further development of IoT technologies are now driving greater adoption of AaaS business models, which will further accelerate the trend toward pay-per-use services (see Figure 2).

IoT enables precise measurement, more accurate billing

At its heart, AaaS is primarily enabled by the digitalization of systems driven by Industry 4.0. Increased digitalization means that the measurement data recorded in each machine can be sent to the manufacturer or owner of the machines through networked systems, where it can then be processed and evaluated. This provides a complete record of how often and to what extent the respective machine was used, giving the manufacturer complete transparency.

Another advantage enabled by system digitalization is the capability for a manufacturer to maintain machines remotely and, using predictive maintenance, to understand precisely when servicing is required through sensors attached to the machine that measure activity and the levels of wear on specific parts. As a result, machines have a much longer service life and productivity increases due to fewer unplanned breakdowns.

Additionally, the manufacturer can use these sensors to measure temperature, humidity, or geolocation to know exactly where the machine is situated and the environment in which it is being used. By contrast, in traditional leasing models, the manufacturer does not have this data and must use a “grey box model” (essentially a data-based simulation) to analyze how durable the machines are and when parts need to be replaced.

This data also facilitates future strategic planning. Through analysis with artificial intelligence (AI) algorithms, the manufacturer can determine how demand for specific machines will develop and thus anticipate future trends.

2

AaaS: The technology perspective

IoT, telemetry data: pivotal for new business models

According to Statista, since 2016, the number of IoT sensors has quadrupled from around 5 billion to about 20 billion devices. Estimates suggest that this development will result in a total of 80 zettabytes of data by 2025. The challenge is that this data is currently only used for data analysis and efficiency purposes, especially in the shift to Industry 4.0, rather than for new business models. As a result, companies continue to improve their (business) processes, but do not rethink them — a key for true transformation. Consequently, a lot of potential is lost, especially in terms of increased customer benefits and added value.

As described in Chapter 1, customers want new services and products — but often do not know exactly what it is they want. When it comes to customers operating in “asset-heavy” markets (i.e., the classic target markets of many small and medium-sized enterprises), customers tend to look for greater financial flexibility through new forms of financing and rental models. The transformation from CAPEX to OPEX is evolving toward customers only wanting to pay for the actual, documented use of assets (whether machines or vehicles) instead of paying a generic rental or lease price. Enabling this capability requires access to IoT sensor data to monitor and understand machine usage. Sensors in IoT devices already collect comprehensive data sets across different asset usage categories. To enable complete analysis and transformation of this IoT data into financial data, the first step is to make it available.

Taking the example of a commercial vehicle such as a tractor, an IoT sensor under the driver’s seat would use telemetry to send information to the manufacturer’s cloud infrastructure. In this case, the sensor data is automatically secured against external access (by meeting ISO standard 26262, “Road vehicles — Functional safety”), ensuring that usage information cannot be manipulated. As soon as the IoT data is available in the manufacturer’s cloud data lake, business/billing logic must be created and applied. This includes, among other areas, metrics for billing processes. Through a micro service architecture in the selected cloud environment, various scalable billing and business logic can be developed. For example, Austrian agricultural machinery manufacture Lindner Traktoren bills based on operating hours. However, it also defines a set engine speed as a threshold value. Above this threshold, the operating cost rate increases; under it, the rate decreases.

Other billing and business logic can also be created to cover the use of attached implements, mileage billing, or tiered pricing. The most important factor when defining activity accounting and pricing is to identify the critical cost drivers for asset wear and tear. By evaluating this data, the asset’s use also becomes transparent, enabling complete asset lifecycle management. In addition to performance-relevant data, environmental data such as CO2 emissions can also be measured. This helps in showing the environmental, social, and governance (ESG) impacts of the asset.

Upon implementing the business and billing logic, the asset data must be integrated into the existing system landscape; for example, the system must create legally compliant invoices and send them to the customer. Furthermore, usage data must also be recorded in the manufacturer’s enterprise resource planning (ERP) system and be available as a data record. While this sounds simple in theory, defining and implementing billing logic directly in an ERP system is difficult in practice, because systems must be individually adapted, resulting in lengthy, costly projects rather than flexible and fast integrations. Therefore, it is best to first implement usage-based billing outside the ERP system, and then integrate data into the system later.

Once the invoice has been created and processed via relevant systems and processes, the next step is integration into payment transactions. In the European B2B environment, corporate customer accounts are accessed via the European Banking Internet Communication Standard (EBICS). However, this standard contains shortcomings, especially around the fully automatic processing and programming capability of payments. In some cases, this means that invoices still must be transferred manually.

Consequently, several associations are working on solutions that support the request-to-pay (R2P) process. However, R2P is only likely to be implemented and made available when ISO 20022 standard is updated to include its format specification in November 2022. To ensure companies can offer further comprehensive solutions, Germany’s Deutsche Kreditwirtschaft (DK) is currently working on a solution for programmatic payments that enables the full digitalization of the payment process. (Note: DK’s initiative should not be confused with the European Central Bank’s approach to a Central Bank Digital Currency [CBDC]. Because of legal and societal requirements, a digital Euro must meet different goals and requirements, such as multichannel availability and offline payment capabilities. At the commercial bank level, requirements then focus on programming capabilities.)

Once a payment process is finalized, the transformation of IoT sensor data into financial data is complete. As this transformation is performed per asset, it provides a corresponding profitability analysis for each asset. Analysis of IoT data shows the asset’s specific usage, incurred costs (primarily through depreciation), as well as generated cash flows. As a result, a P&L statement can be prepared for each asset. In the context of financing, this provides a far better basis for assessing risk. When looking at the entire asset portfolio (e.g., vehicle fleet) with such precise information, overall data collection enables conclusions about profitability to increase in accuracy.

3

AaaS: The financial perspective

Transforming the business model

The impacts of AaaS are wide-ranging and will drive comprehensive change across multiple industries. In addition to changing usage patterns and ownership, AaaS will likely transform existing business models as well. Unprecedented visibility into the condition, claim, and use of assets provides both an overview of the current value of an asset and the revenue it generates — the basis for ROI calculations. The physical asset thus fulfills the basic requirement of becoming an investment object itself. Therefore, the impact is not limited to the industry itself; it also changes requirements for financing solutions.

For manufacturers, AaaS offers the opportunity to expand their own business models, ultimately transforming them toward the direction of servitization. While manufacturers usually generate revenues primarily by selling the assets they produce, such as machinery and equipment, the newly created opportunities allow them to make asset capacities available to users on a permanent or even short-term basis. To satisfy changing user needs, the manufacturer then offers a complete package that is billed via a usage-based rate. In addition to the use of the asset, the offering can include maintenance and repair as well as additional services like insurance. These additional services can be monetized to a greater extent and cover a longer period of time. The resulting long-term, stronger user commitment to the manufacturer delivers an increase in customer lifetime value. Instead of just one-off revenue from the sale of an asset, companies receive a monthly recurring revenue.

Value proposition of AaaS

Manufacturer/asset owner

For the manufacturer, the expansion — or, rather, conversion — of its business model delivers a range of advantages. For example, the manufacturer can target new customer groups that were previously unreachable effectively due to capital restrictions or investment hurdles. Moreover, additional revenues can be generated through services and add-ons. The basic concept of the AaaS business model transfers the utilization risk from the customer, who is only billed for service used, to the manufacturer or owner of the asset. In the case of low utilization rates, the owner generates lower revenues. In the case of high utilization, the owner receives correspondingly higher payments from the user.

This utilization risk can be priced by the owner through higher usage fees and at least partially reduced through such mechanisms as the agreement of a basic fee. Automating back-office processes, such as billing and invoicing, is both vital for manufacturers looking to scale AaaS business models and an essential part of the value proposition as it optimizes cost structure. The availability of usage data enables unprecedented transparency into the payment flows generated as well as the condition and complete lifecycle of the asset. The manufacturer can thus manage service and maintenance in a targeted manner; utilize access to a daily, updated assessment of an asset’s value; and gain valuable insights into how an asset is being used and the requirements that it has to meet — all of which can feed into new product design. AaaS business models also enable optimization of the asset’s properties by adapting production processes. The manufacturer, as the owner of the asset, is also incentivized to produce assets with high value and resilience that can generate revenue over the longest possible periods of time, even under heavy use. Ultimately, AaaS business models promise to make resource use more efficient, as well as contribute significantly to the adoption of the circular economy and even sustainability across industry.

User/customer

AaaS delivers an equally large number of benefits for the asset user. Through the servitization business model, the manufacturer takes over complete responsibility for asset operation. By making the manufacturer responsible for maintenance — and by ensuring that any downtime does not impact the customer due to the benefit of usage-based billing — everyone’s interests are aligned, helping to enable a smoother operating relationship. Asset productivity is increased, while at the same time the user can concentrate fully on the core business. Since the user pays solely for the use of the asset or its output, and these costs are covered by the revenue generated from the goods the asset produces, payment flows are all in parallel. The asset manufacturer/owner assumes the utilization risk from the asset user.

Even if, in most cases, the cost per unit produced is likely to be slightly higher at average or increased utilization levels, the user still benefits. AaaS acts as an insurance policy in cases where assets are underutilized, helping ensure that the user’s cost structure is more flexible and preserving liquidity if sales or orders drop. Increased transparency about asset utilization and accrued costs enables better calculations of the profitability of product offerings and business focus. Moreover, resources are used more efficiently, contributing to a more sustainable overall business. Additionally, the shift from CAPEX to OPEX is a significant benefit for the user. Compared to a loan-financed acquisition of the asset, the user also profits from a lighter balance sheet, since the asset manufacturer continues to own the asset.

Options for refinancing the asset

As explained above, with AaaS, the asset user benefits from a lighter balance sheet. By contrast, an AaaS business model significantly extends the balance sheet of the asset’s manufacturer. On a small scale, this may still be acceptable, and sometimes even desirable. However, if the business model is to be scalable, the manufacturer must ensure that assets are not capitalized on its balance sheet.

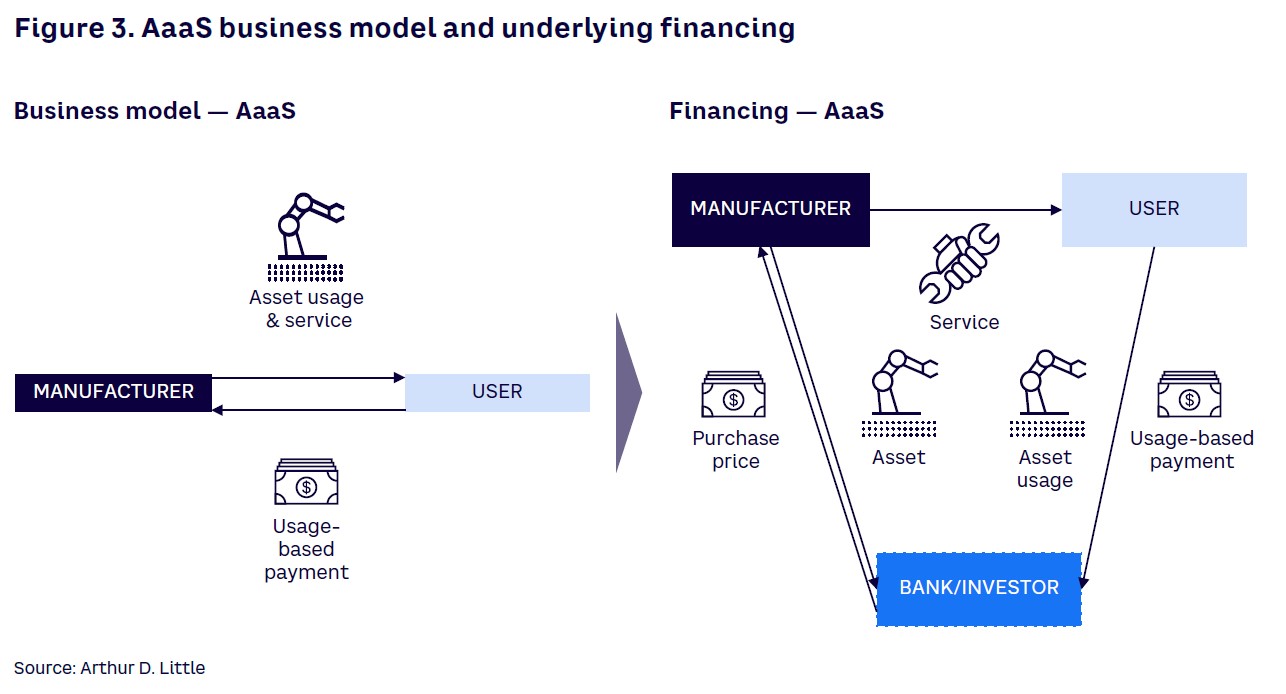

To ensure this, it is crucial to differentiate between the two types of AaaS model — business model and financing — depending on ownership of the asset (see Figure 3).

In the case of the business model AaaS, the manufacturer keeps the asset on its balance sheet but also benefits from the entire cash flows it generates, while taking on the utilization risk. However, if the cash flows generated by an asset become measurable, the physical asset can be turned into an investment object with a calculable return. That leads to the second model, which is characterized by the involvement of an investor. Investors such as banks, faced with dwindling returns in the market, can tap into such new asset classes, provided they are competent at assessing the risk. By allowing an outside investor to become the owner of the asset, the manufacturer can remove the asset from its own balance sheet. Three options for refinancing are outlined below:

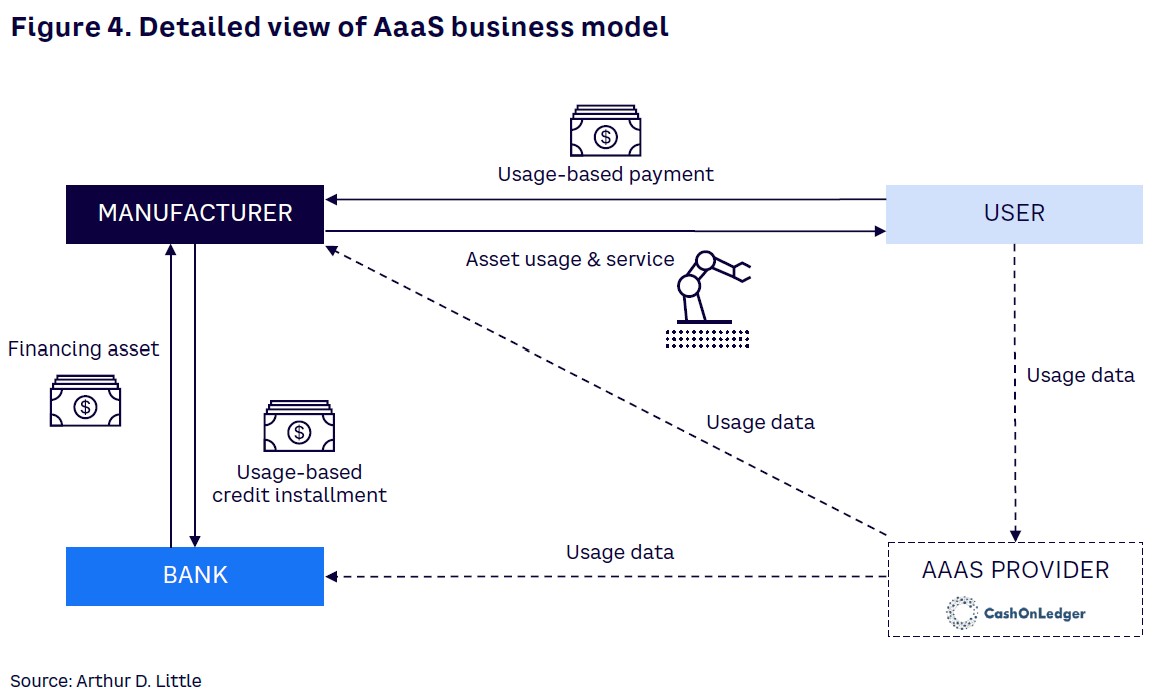

- Financing for the manufacturer. If the asset manufacturer wants to collect full cash flows from the asset and is simply looking for a way to refinance it, it normally takes out a loan. The manufacturer remains the owner of the asset and makes it available to the user, receiving a usage-based payment in return. If the bank is interested in (partially) assuming the utilization risk, its financing/interest rate can be structured depending on the utilization of the asset (see Figure 4). To ensure that this model is effective, it is vital that all parties have full visibility into the asset’s IoT data.

- Pay-per-use credit for the customer. If the asset user is interested in usage-based billing but the manufacturer is not willing to take the assets onto its own balance sheet, assets can be covered by pay-per-use financing (see Figure 5), with various offers covering this area already available (including those from Germany’s Commerzbank). In the case of pay-per-use financing for the customer, the manufacturer sells the asset to the user. The user then takes out financing from the bank at an interest rate based on the use of the asset. Making the rate flexible essentially creates an AaaS business model.

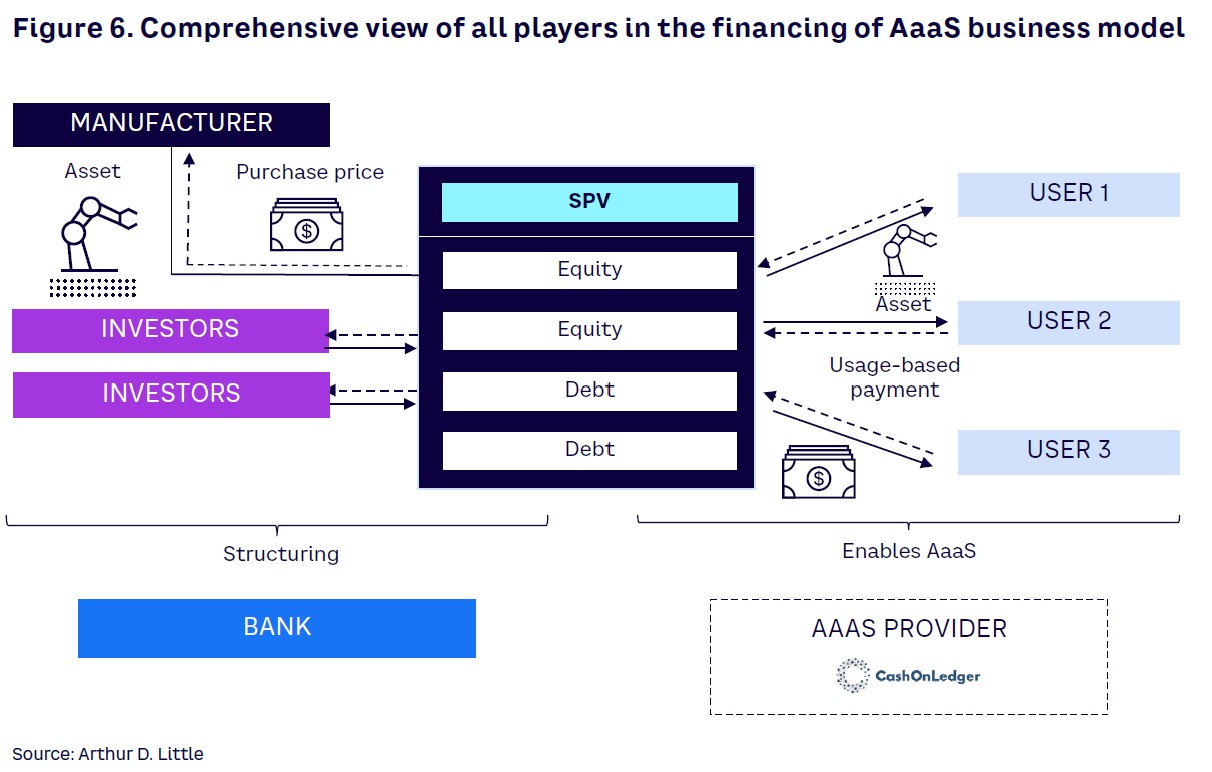

To implement flexible financing successfully, the financing bank needs access to IoT data generated by the asset, as well as the skills to analyze the data, in order to complete a full risk assessment that determines the pricing as well as the fluctuation margins of the interest rate. The added value is obvious: the manufacturer can satisfy customer needs and de facto offer a simple form of usage-based billing. The user’s financing rate is based on actual usage, but the asset remains on the user’s balance sheet. The bank can expand its business model toward AaaS, meet changing customer needs, and potentially generate higher returns by assuming part of the utilization risk. - Financing by means of a special-purpose vehicle (SPV). The most sensible approach to financing AaaS is a solution that does not burden the balance sheet of either the manufacturer or the user. The SPV is a structure that offers a solution that is in many ways similar to the approaches of original equipment manufacturers (OEMs) in the automotive and mechanical engineering sectors that have their own captive finance companies for sales financing. In this model, the manufacturer sells the asset to the SPV, receiving payment of the purchase price. The SPV becomes the owner of the asset, offers it to the user, and in return receives use-dependent cash flows (see Figure 6).

The manufacturer continues to provide maintenance and repair. To ensure that the manufacturer participates at least partially in ongoing cash flow and that interests are aligned with regard to the value of the asset, it can make sense for the manufacturer to hold an equity share in the SPV. This is also advantageous in that the manufacturer has the greatest asset expertise and is responsible for distributing and servicing contracts.

At the same time, financing through an SPV opens up the investment in the asset to a large number of investors, allowing them to participate in the cash flow that the asset generates. The central prerequisite for success is transparency of the asset’s IoT data. In principle, refinancing of the SPV is also conceivable via debt instruments. Assets can be tokenized, offering a range of opportunities when it comes to how the SPV is structured. In this case, a digital twin is created based on the IoT data and, if the asset is tokenized using distributed ledger technology, it becomes accessible to a broader spectrum of investors. In this context, tokenization is a way to make an asset liquid and investable, through debt financing or equity-like ownership of the assets. The Liechtenstein Token Act currently provides a good regulatory framework for combining multiple assets into one SPV in which investors can invest via shares or debt.

Conclusion

With the increasing availability of IoT data and changing user needs, AaaS business models are becoming increasingly important. At the same time, the increased interaction of individual market participants in the AaaS environment and the corresponding changes in these business models bring greater complexity that must be managed.

In addition to technical requirements, such as the availability of IoT data at the asset level, the willingness to change one’s own business model is essential. For example, manufacturers must look at transforming their sales teams and implementing new service models if they are to successfully implement AaaS business models. Moreover, to scale this approach, manufacturers must focus on both the automation of processes (e.g., billing) and the refinancing of assets to grow AaaS revenues and reduce risk.

AaaS models bring the promise of significant value for users, manufacturers, and investors and have the potential to substantially influence value creation across multiple industries.

DOWNLOAD THE FULL REPORT

17 min read • Financial services

Asset as a service

Transforming ownership and business models promises significant value

DATE

Executive Summary

Asset-as-a-service (AaaS) business models are increasingly being adopted across multiple industry sectors, driven by a growing demand from users of such assets as machinery and equipment. In the AaaS model, users no longer purchase assets; instead, they are billed for the actual benefit they receive. However, to introduce AaaS business models successfully, parties must meet several conditions.

AaaS models require the use of sensors to collect Internet of Things (IoT) and telemetry data, which is then shared and processed via networked systems, and provide a basis for calculating actual usage and current asset value. Automated billing, invoicing, and payment, as well as integration with existing enterprise resource planning systems, are important factors for scaling AaaS models.

AaaS delivers both benefits and implications for the existing business models of all parties involved. These parties include the equipment manufacturer, the user, and investors, such as financial institutions that traditionally provide loans or leasing models.

But a key question arises: which of the parties involved own the assets, receive cash flows from their use, and bear utilization risks? The answer will depend on each player’s ability to transform — along with their willingness to change their business models. The outcome is also closely linked to financing design, which can be structured differently depending on the business model, preferences, and type of asset. This Report describes various options and explains the benefits and risks for everyone involved.

1

Financing: Then & now

Until now, customers looking to finance an asset have traditionally had four options: purchasing, financing, leasing, or outsourcing (see Figure 1). These four options have major differences in how they are designed (see Table 1).

In the cases of purchasing and financing, the asset becomes part of a company’s assets. With financing, the company pays a fixed sum to a financial services provider over a set length of time. The other two variants (leasing and outsourcing) are more flexible and less capital-intensive. They differ primarily in the type and measurement of payment for the use of the asset.

Boosting sales through leasing dates back to the 19th century. Essentially, the leasing partner purchases the asset, with the end user company paying the partner at a fixed rate over a set term. In contrast to simply renting, the purchaser can then buy the item for a residual price at the end of the term.

The outsourcing of services, previously performed internally, has been taking place since the 1960s. Contracts specify the duration and subject matter of the external service provision, while the outsourcing partner retains ownership of the assets used within the contract.

The future belongs to AaaS

In AaaS business models, the traditional division of roles among manufacturers, buyers, and financial service providers is newly defined. With AaaS, assets are no longer purchased, financed, or leased by the user; instead, they are purchased on a pay-per-use or pay-per-output basis, where users pay only for actual use (see Table 2). These new business models transfer the familiar concepts of other “as-a-service” models, which are already common for software solutions, to tangible assets such as machinery and equipment.

In AaaS models, billing is based on usage rather than at a flat rate. This means that customers/users have much greater flexibility in how they use assets. For example, they can just use them for a short time (e.g., project-based) and then relinquish the asset once it is no longer needed. This generates new opportunities for investors — both on the debt and equity side — by creating new asset classes. These are attractive options, especially given the current limited investment opportunities and liquidity in the market.

The value trend and thus the current fair value of a machine must show a clear correlation to operating hours, capacity utilization, or the number of units produced.

AaaS business models offer advantages for users and also transfer the risk of asset ownership to AaaS providers. These adjustments also enable new business models for asset manufacturers and financial service providers. For manufacturers, the AaaS business model opens up new revenue streams, some of which promise higher margins than with traditional sales or rental businesses.

AaaS models are already being used in certain industries, particularly in mechanical and plant engineering. For example, Rolls-Royce is considered one of the first engineering companies to offer pay-per-use models with its “Power by the Hour” performance-based contracts for its jet engines. Other examples of companies integrating IoT technology with pay-per-use models include machinery and equipment manufacturers DMG Mori and Trumpf.

However, beyond these examples, AaaS business models are not yet established across all industries, with wider usage limited by factors such as a lack of process-integration options. However, ongoing digitalization and further development of IoT technologies are now driving greater adoption of AaaS business models, which will further accelerate the trend toward pay-per-use services (see Figure 2).

IoT enables precise measurement, more accurate billing

At its heart, AaaS is primarily enabled by the digitalization of systems driven by Industry 4.0. Increased digitalization means that the measurement data recorded in each machine can be sent to the manufacturer or owner of the machines through networked systems, where it can then be processed and evaluated. This provides a complete record of how often and to what extent the respective machine was used, giving the manufacturer complete transparency.

Another advantage enabled by system digitalization is the capability for a manufacturer to maintain machines remotely and, using predictive maintenance, to understand precisely when servicing is required through sensors attached to the machine that measure activity and the levels of wear on specific parts. As a result, machines have a much longer service life and productivity increases due to fewer unplanned breakdowns.

Additionally, the manufacturer can use these sensors to measure temperature, humidity, or geolocation to know exactly where the machine is situated and the environment in which it is being used. By contrast, in traditional leasing models, the manufacturer does not have this data and must use a “grey box model” (essentially a data-based simulation) to analyze how durable the machines are and when parts need to be replaced.

This data also facilitates future strategic planning. Through analysis with artificial intelligence (AI) algorithms, the manufacturer can determine how demand for specific machines will develop and thus anticipate future trends.

2

AaaS: The technology perspective

IoT, telemetry data: pivotal for new business models

According to Statista, since 2016, the number of IoT sensors has quadrupled from around 5 billion to about 20 billion devices. Estimates suggest that this development will result in a total of 80 zettabytes of data by 2025. The challenge is that this data is currently only used for data analysis and efficiency purposes, especially in the shift to Industry 4.0, rather than for new business models. As a result, companies continue to improve their (business) processes, but do not rethink them — a key for true transformation. Consequently, a lot of potential is lost, especially in terms of increased customer benefits and added value.

As described in Chapter 1, customers want new services and products — but often do not know exactly what it is they want. When it comes to customers operating in “asset-heavy” markets (i.e., the classic target markets of many small and medium-sized enterprises), customers tend to look for greater financial flexibility through new forms of financing and rental models. The transformation from CAPEX to OPEX is evolving toward customers only wanting to pay for the actual, documented use of assets (whether machines or vehicles) instead of paying a generic rental or lease price. Enabling this capability requires access to IoT sensor data to monitor and understand machine usage. Sensors in IoT devices already collect comprehensive data sets across different asset usage categories. To enable complete analysis and transformation of this IoT data into financial data, the first step is to make it available.

Taking the example of a commercial vehicle such as a tractor, an IoT sensor under the driver’s seat would use telemetry to send information to the manufacturer’s cloud infrastructure. In this case, the sensor data is automatically secured against external access (by meeting ISO standard 26262, “Road vehicles — Functional safety”), ensuring that usage information cannot be manipulated. As soon as the IoT data is available in the manufacturer’s cloud data lake, business/billing logic must be created and applied. This includes, among other areas, metrics for billing processes. Through a micro service architecture in the selected cloud environment, various scalable billing and business logic can be developed. For example, Austrian agricultural machinery manufacture Lindner Traktoren bills based on operating hours. However, it also defines a set engine speed as a threshold value. Above this threshold, the operating cost rate increases; under it, the rate decreases.

Other billing and business logic can also be created to cover the use of attached implements, mileage billing, or tiered pricing. The most important factor when defining activity accounting and pricing is to identify the critical cost drivers for asset wear and tear. By evaluating this data, the asset’s use also becomes transparent, enabling complete asset lifecycle management. In addition to performance-relevant data, environmental data such as CO2 emissions can also be measured. This helps in showing the environmental, social, and governance (ESG) impacts of the asset.

Upon implementing the business and billing logic, the asset data must be integrated into the existing system landscape; for example, the system must create legally compliant invoices and send them to the customer. Furthermore, usage data must also be recorded in the manufacturer’s enterprise resource planning (ERP) system and be available as a data record. While this sounds simple in theory, defining and implementing billing logic directly in an ERP system is difficult in practice, because systems must be individually adapted, resulting in lengthy, costly projects rather than flexible and fast integrations. Therefore, it is best to first implement usage-based billing outside the ERP system, and then integrate data into the system later.

Once the invoice has been created and processed via relevant systems and processes, the next step is integration into payment transactions. In the European B2B environment, corporate customer accounts are accessed via the European Banking Internet Communication Standard (EBICS). However, this standard contains shortcomings, especially around the fully automatic processing and programming capability of payments. In some cases, this means that invoices still must be transferred manually.

Consequently, several associations are working on solutions that support the request-to-pay (R2P) process. However, R2P is only likely to be implemented and made available when ISO 20022 standard is updated to include its format specification in November 2022. To ensure companies can offer further comprehensive solutions, Germany’s Deutsche Kreditwirtschaft (DK) is currently working on a solution for programmatic payments that enables the full digitalization of the payment process. (Note: DK’s initiative should not be confused with the European Central Bank’s approach to a Central Bank Digital Currency [CBDC]. Because of legal and societal requirements, a digital Euro must meet different goals and requirements, such as multichannel availability and offline payment capabilities. At the commercial bank level, requirements then focus on programming capabilities.)

Once a payment process is finalized, the transformation of IoT sensor data into financial data is complete. As this transformation is performed per asset, it provides a corresponding profitability analysis for each asset. Analysis of IoT data shows the asset’s specific usage, incurred costs (primarily through depreciation), as well as generated cash flows. As a result, a P&L statement can be prepared for each asset. In the context of financing, this provides a far better basis for assessing risk. When looking at the entire asset portfolio (e.g., vehicle fleet) with such precise information, overall data collection enables conclusions about profitability to increase in accuracy.

3

AaaS: The financial perspective

Transforming the business model

The impacts of AaaS are wide-ranging and will drive comprehensive change across multiple industries. In addition to changing usage patterns and ownership, AaaS will likely transform existing business models as well. Unprecedented visibility into the condition, claim, and use of assets provides both an overview of the current value of an asset and the revenue it generates — the basis for ROI calculations. The physical asset thus fulfills the basic requirement of becoming an investment object itself. Therefore, the impact is not limited to the industry itself; it also changes requirements for financing solutions.

For manufacturers, AaaS offers the opportunity to expand their own business models, ultimately transforming them toward the direction of servitization. While manufacturers usually generate revenues primarily by selling the assets they produce, such as machinery and equipment, the newly created opportunities allow them to make asset capacities available to users on a permanent or even short-term basis. To satisfy changing user needs, the manufacturer then offers a complete package that is billed via a usage-based rate. In addition to the use of the asset, the offering can include maintenance and repair as well as additional services like insurance. These additional services can be monetized to a greater extent and cover a longer period of time. The resulting long-term, stronger user commitment to the manufacturer delivers an increase in customer lifetime value. Instead of just one-off revenue from the sale of an asset, companies receive a monthly recurring revenue.

Value proposition of AaaS

Manufacturer/asset owner

For the manufacturer, the expansion — or, rather, conversion — of its business model delivers a range of advantages. For example, the manufacturer can target new customer groups that were previously unreachable effectively due to capital restrictions or investment hurdles. Moreover, additional revenues can be generated through services and add-ons. The basic concept of the AaaS business model transfers the utilization risk from the customer, who is only billed for service used, to the manufacturer or owner of the asset. In the case of low utilization rates, the owner generates lower revenues. In the case of high utilization, the owner receives correspondingly higher payments from the user.

This utilization risk can be priced by the owner through higher usage fees and at least partially reduced through such mechanisms as the agreement of a basic fee. Automating back-office processes, such as billing and invoicing, is both vital for manufacturers looking to scale AaaS business models and an essential part of the value proposition as it optimizes cost structure. The availability of usage data enables unprecedented transparency into the payment flows generated as well as the condition and complete lifecycle of the asset. The manufacturer can thus manage service and maintenance in a targeted manner; utilize access to a daily, updated assessment of an asset’s value; and gain valuable insights into how an asset is being used and the requirements that it has to meet — all of which can feed into new product design. AaaS business models also enable optimization of the asset’s properties by adapting production processes. The manufacturer, as the owner of the asset, is also incentivized to produce assets with high value and resilience that can generate revenue over the longest possible periods of time, even under heavy use. Ultimately, AaaS business models promise to make resource use more efficient, as well as contribute significantly to the adoption of the circular economy and even sustainability across industry.

User/customer

AaaS delivers an equally large number of benefits for the asset user. Through the servitization business model, the manufacturer takes over complete responsibility for asset operation. By making the manufacturer responsible for maintenance — and by ensuring that any downtime does not impact the customer due to the benefit of usage-based billing — everyone’s interests are aligned, helping to enable a smoother operating relationship. Asset productivity is increased, while at the same time the user can concentrate fully on the core business. Since the user pays solely for the use of the asset or its output, and these costs are covered by the revenue generated from the goods the asset produces, payment flows are all in parallel. The asset manufacturer/owner assumes the utilization risk from the asset user.

Even if, in most cases, the cost per unit produced is likely to be slightly higher at average or increased utilization levels, the user still benefits. AaaS acts as an insurance policy in cases where assets are underutilized, helping ensure that the user’s cost structure is more flexible and preserving liquidity if sales or orders drop. Increased transparency about asset utilization and accrued costs enables better calculations of the profitability of product offerings and business focus. Moreover, resources are used more efficiently, contributing to a more sustainable overall business. Additionally, the shift from CAPEX to OPEX is a significant benefit for the user. Compared to a loan-financed acquisition of the asset, the user also profits from a lighter balance sheet, since the asset manufacturer continues to own the asset.

Options for refinancing the asset

As explained above, with AaaS, the asset user benefits from a lighter balance sheet. By contrast, an AaaS business model significantly extends the balance sheet of the asset’s manufacturer. On a small scale, this may still be acceptable, and sometimes even desirable. However, if the business model is to be scalable, the manufacturer must ensure that assets are not capitalized on its balance sheet.

To ensure this, it is crucial to differentiate between the two types of AaaS model — business model and financing — depending on ownership of the asset (see Figure 3).

In the case of the business model AaaS, the manufacturer keeps the asset on its balance sheet but also benefits from the entire cash flows it generates, while taking on the utilization risk. However, if the cash flows generated by an asset become measurable, the physical asset can be turned into an investment object with a calculable return. That leads to the second model, which is characterized by the involvement of an investor. Investors such as banks, faced with dwindling returns in the market, can tap into such new asset classes, provided they are competent at assessing the risk. By allowing an outside investor to become the owner of the asset, the manufacturer can remove the asset from its own balance sheet. Three options for refinancing are outlined below:

- Financing for the manufacturer. If the asset manufacturer wants to collect full cash flows from the asset and is simply looking for a way to refinance it, it normally takes out a loan. The manufacturer remains the owner of the asset and makes it available to the user, receiving a usage-based payment in return. If the bank is interested in (partially) assuming the utilization risk, its financing/interest rate can be structured depending on the utilization of the asset (see Figure 4). To ensure that this model is effective, it is vital that all parties have full visibility into the asset’s IoT data.

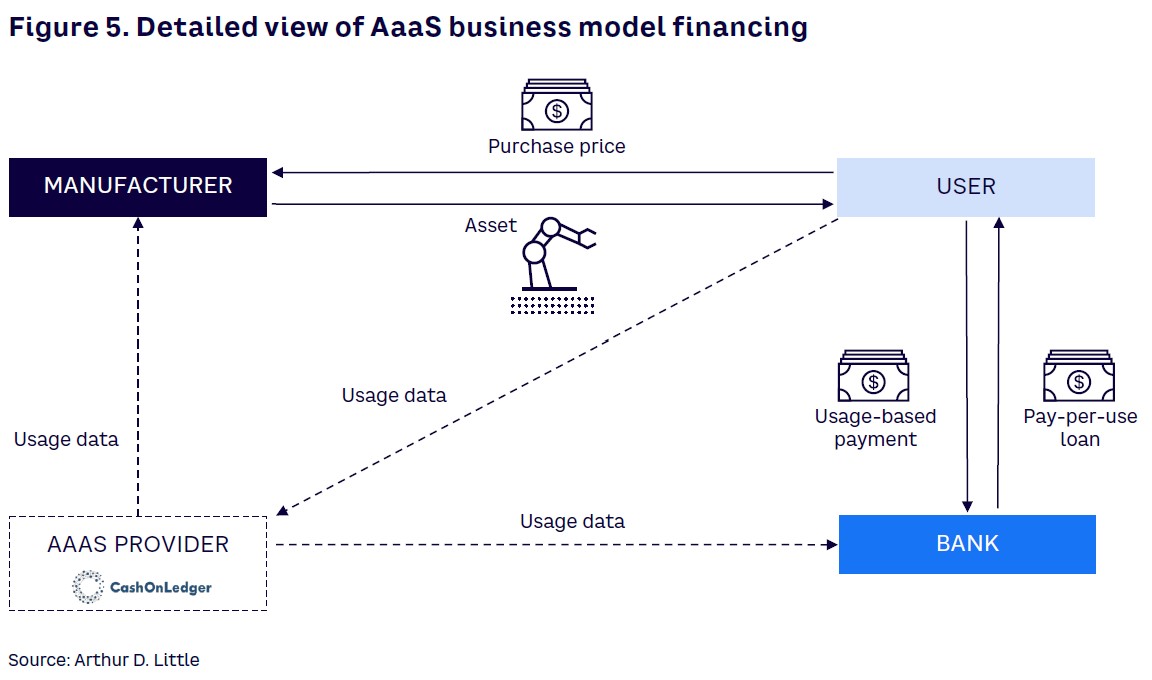

- Pay-per-use credit for the customer. If the asset user is interested in usage-based billing but the manufacturer is not willing to take the assets onto its own balance sheet, assets can be covered by pay-per-use financing (see Figure 5), with various offers covering this area already available (including those from Germany’s Commerzbank). In the case of pay-per-use financing for the customer, the manufacturer sells the asset to the user. The user then takes out financing from the bank at an interest rate based on the use of the asset. Making the rate flexible essentially creates an AaaS business model.

To implement flexible financing successfully, the financing bank needs access to IoT data generated by the asset, as well as the skills to analyze the data, in order to complete a full risk assessment that determines the pricing as well as the fluctuation margins of the interest rate. The added value is obvious: the manufacturer can satisfy customer needs and de facto offer a simple form of usage-based billing. The user’s financing rate is based on actual usage, but the asset remains on the user’s balance sheet. The bank can expand its business model toward AaaS, meet changing customer needs, and potentially generate higher returns by assuming part of the utilization risk. - Financing by means of a special-purpose vehicle (SPV). The most sensible approach to financing AaaS is a solution that does not burden the balance sheet of either the manufacturer or the user. The SPV is a structure that offers a solution that is in many ways similar to the approaches of original equipment manufacturers (OEMs) in the automotive and mechanical engineering sectors that have their own captive finance companies for sales financing. In this model, the manufacturer sells the asset to the SPV, receiving payment of the purchase price. The SPV becomes the owner of the asset, offers it to the user, and in return receives use-dependent cash flows (see Figure 6).

The manufacturer continues to provide maintenance and repair. To ensure that the manufacturer participates at least partially in ongoing cash flow and that interests are aligned with regard to the value of the asset, it can make sense for the manufacturer to hold an equity share in the SPV. This is also advantageous in that the manufacturer has the greatest asset expertise and is responsible for distributing and servicing contracts.

At the same time, financing through an SPV opens up the investment in the asset to a large number of investors, allowing them to participate in the cash flow that the asset generates. The central prerequisite for success is transparency of the asset’s IoT data. In principle, refinancing of the SPV is also conceivable via debt instruments. Assets can be tokenized, offering a range of opportunities when it comes to how the SPV is structured. In this case, a digital twin is created based on the IoT data and, if the asset is tokenized using distributed ledger technology, it becomes accessible to a broader spectrum of investors. In this context, tokenization is a way to make an asset liquid and investable, through debt financing or equity-like ownership of the assets. The Liechtenstein Token Act currently provides a good regulatory framework for combining multiple assets into one SPV in which investors can invest via shares or debt.

Conclusion

With the increasing availability of IoT data and changing user needs, AaaS business models are becoming increasingly important. At the same time, the increased interaction of individual market participants in the AaaS environment and the corresponding changes in these business models bring greater complexity that must be managed.

In addition to technical requirements, such as the availability of IoT data at the asset level, the willingness to change one’s own business model is essential. For example, manufacturers must look at transforming their sales teams and implementing new service models if they are to successfully implement AaaS business models. Moreover, to scale this approach, manufacturers must focus on both the automation of processes (e.g., billing) and the refinancing of assets to grow AaaS revenues and reduce risk.

AaaS models bring the promise of significant value for users, manufacturers, and investors and have the potential to substantially influence value creation across multiple industries.

DOWNLOAD THE FULL REPORT

RELATED INFORMATION

Strategic Options in the Fleet Service Market

Arthur D. Little recently completed a comprehensive survey of all the major players in the fleet service sector in the top five European automotive fleet markets. To model the market, determine the…