DOWNLOAD

17 min read • Strategy

How to enable the company of tomorrow

Decoupling capabilities and leveraging the ecosystem

Businesses have traditionally organized themselves to ensure optimal effectiveness in each of their business functions. However, shorter product lifecycles, demand for customization, rising consumer expectations, and the growth of automation and data challenge this model. This article explains how success requires organizations to decouple capabilities from business functions, in order to deliver best-inclass performance and enable the company of tomorrow.

Based on demand from its 7,000+ shops in almost 100 countries, a prominent fast-fashion retailer ordered thousands of raincoats from its Asian suppliers. During the 11-hour flight that brought the coats to the logistics hub in Europe, they were reassigned to markets and shops based on actualized data that leveraged big data and AI, considering weather forecasts, exchange rates and other variables. In a hyper-efficient logistics center only a few kilometers from the airport, a logistics partner received the raincoat shipments and relabeled and folded them as needed for each market, shipping them for distribution to their final destinations in only a few hours.

In another example, a global smartphone provider considered it strategic to achieve and maintain a leading position in display technology and manufacturing. To ensure this, it supplied smartphone displays of its archrival in the market.

Inditex (Zara) and Samsung are both examples of how capabilities can be externalized or opened to the market. As data and technology are freely available and adopted by companies, collaboration with other companies to boost productivity and creativity for core and non-core capabilities can be achieved with less friction, transaction costs and risks than in the past. This is fundamentally changing how companies conceive, develop, produce, and deliver their products or integrate third-party products and services into their product build, operations, and offerings. Our analysis suggests that this externalization of capabilities – decoupling them from the company’s business functions and leveraging the ecosystem more profoundly – will transform companies, as well as the landscapes of many industries, in the next three to five years. In this article we examine what’s behind the trend and identify some imperatives for leaders to consider when transforming their own organizations.

Several trends are challenging the traditional way companies define themselves

Companies have traditionally organized themselves with the objective of ensuring optimal efficiency and effectiveness in each of their business functions (R&D, production, distribution and sales) to deliver defined products and services. However, three trends challenge this model:

- Products and services: shorter life cycles, a customization imperative

- Changing, more demanding customer expectations

- The rise of automation and a data-driven world

1. Products and services: Shorter life cycles, a customization imperative

With few exceptions, almost any product or service can now be replicated in months, rather than years. This makes it increasingly difficult to build sustainable competitive advantage on product features or qualities. Moreover, product customization is becoming a must in both B2B and B2C, not only around product features, but in all interactions. Blurring industry boundaries and the acceleration of time1 leave companies ever-shorter time frames to set up efficient and effective processes so they can monetize shortened product life cycles.

As a result, optimizing along the traditional value chain is not enough to ensure sustainable profitability. The ability to pivot rapidly and adjust to evolving ecosystems has become all but essential.

2. Changing, more demanding customer expectations

In today’s business environment, customers expect everything to be delivered immediately, wherever they happen to be. They value experiences (with focus on how their needs are met) above products. Loyalty is increasingly driven by digital perceptions and the emotions that brands create through the purposes and values they put forward – as well as how consistent their actions are with those values2.

As a result, customer experience and trust around expertise, quality and reputation become more relevant than the physical features of products and services. BMW’s memorable advertising campaign, “Do you enjoy driving?” captures the essence of this change.

Tailoring messages to customer expectations and needs is driving major change within marketing functions, forcing them to add new capabilities. Marketing has migrated from broadcasting to active listening and engaging in dialog with customers. The acquisition of Sapient (a technology integrator) by Publicis (an advertising agency) to create the “agency of the future” shows how players are responding in order to compete in this new ecosystem.

3. The rise of automation and a data-driven world

Customization would not be possible without data to understand and precisely forecast customer behavior, as well as automation to effectively deliver it. The amount of data that is being collected, processed and interpreted has exploded over the last decade3. Increasing automation will put data at the core of every business process.

The availability and affordability of standardized technology infrastructure (from players such as Amazon, Microsoft and Alibaba) mean companies don’t need to develop their own data-related capabilities. Inexpensive information processing lowers transaction costs and further facilitates decoupling of capabilities and business functions.

Extracting value from data (whether company generated or from open data sources, third parties or ecosystems) has therefore emerged as a new capability that pervades all business functions. Beyond well-known examples such as Google and Facebook, many traditional industrial companies such as Atlas Copco (which is leveraging data for its pressured air-as-a-service business) are building business models based on data.

Companies will increasingly define themselves in terms of their capabilities rather than their products

As a consequence of these trends, the companies of tomorrow are shifting from a set, linear position in a supply chain to one that dynamically adjusts within their ecosystem. They will focus more on how they conceive, develop, produce and take their products and services to market. This means decoupling business functions (aligned with what they do) from capabilities (how they do it) to deliver value. Companies will focus on what they can do best, operating in those areas at their optimal scale. They will leverage best-in-class ecosystem partners to boost their capabilities and externalize both key and non-critical ones. These innovative, adaptive companies will enjoy extra resilience in their operations and future prospects.

Decoupling capabilities from core business functions has a long history

Decoupling capabilities from business functions is nothing new in itself, and can be traced back to outsourcing of information technology-related processes from the late 1980s4. Efficient IT operations required skills, or capabilities at a scale, that non-specialized players could not achieve. Outsourcing contracts tended to be long-term commitments and covered a handful of functions. But despite all its limitations, outsourcing showed companies how they could decouple business functions from capabilities. It also created a new breed of companies that competed based on which could best provide some of these missing capabilities.

As outsourcing became an established practice and the reach of functions grew, operational reasons evolved to more strategic considerations. For example, hotel chains recognized that the capabilities required to manage real estate no longer provided any competitive advantage. Thus, they have freed financial resources by decoupling the ownership of “their” buildings, which are frequently sold to specialized asset management players. This allows the hotel chains to focus on aspects such as operations, brand and user experience (so-called “core competencies”). Decoupling also means companies can boost production by removing bottlenecks. Following this model, high-end fashion and luxury companies focus on brand management for their perfume product lines, leveraging product-design and manufacturing capabilities of third parties. Apple took advantage of the flexible capacity provided by contract manufacturers to meet the explosive demand prompted by the launch of the iPhone.

Sometimes, regulators have taken the lead. In many jurisdictions, energy utilities have been unbundled, which has separated their distribution activities from their retail activities, each requiring a different set of capabilities (optimizing asset utilization versus dealing with commodity price hedging and customer management).

An inflection point will cause costs and risks to drop drastically – as shown by early examples

However, whereas outsourcing and capability-based approaches have been around for decades, technology, connectivity, and the growing adoption of automation and AI are creating a new inflection point when the costs and risks of using complementary capabilities will be hugely reduced. The companies of tomorrow will therefore need to leverage new management approaches for optimal scale, cooperate with highly efficient and creative specialized ecosystem partners, or boost their internal capabilities. AI and advanced analytics will be critical.

Glimpses of these companies of tomorrow are already here, at different scales of adoption. A growing number of business decisions are aligned with this new logic. For example, Iberdrola, the number-one producer of wind power and one of the world’s biggest electricity utilities by market capitalization, has decoupled its renewables and networks arms so it can develop the first of these businesses on a global scale.

Some companies are already achieving extra sources of revenue by commercializing their in-house capabilities (“opening up the capability”). This helps gain scale and competitive advantage while minimizing the risk of failure. In addition to Amazon opening its information-processing and storage capabilities through Amazon Web Services, retail bank Banco Santander recently announced that it would open its payments platform to achieve the minimum scale required to compete.

The automotive sector provides a good example of extending collaboration from non-core to core capabilities. Here, the challenges around the transition from combustion engines to electric power trains and from ownership to access have forced traditional auto makers to reconsider their approaches. Demonstrating this, Daimler and BMW are pooling their noncore mobility services to create a new global player that will provide sustainable urban mobility for customers. They have also stated that they are sharing core engineering capabilities on driverless cars.

New entrants in every industry have taken full advantage of the opportunities provided by decoupling. Challenger banks, such as N26, focus on customer experience and rely on third parties for product development, regulatory compliance or IT platforms. Aryaka, a next-generation telecoms provider, concentrates on products and leverages connectivity and go-to-market channels from partners to reach its customers. Many small online retailers use Amazon’s platform to reach consumers.

Decoupling can also be used to build a new ecosystem. While Tesla’s initial insistence on being vertically integrated may seem to be in opposition to this trend, it actually recognizes that dominating certain capabilities is the way to build a position in a new industry. Panasonic building batteries in Tesla’s plant is another example of capabilities going beyond a firm’s walls. Tesla has opened its patents and published its roadmaps, demonstrating the importance of creating an ecosystem where your capability advantages can thrive.

Finally, in the telecoms industry, Telefonica is transforming itself from an integrated network and service operator to a capabilities- and platform-based business, splitting into a NetCo and an OpCo to take the best advantage of their respective capabilities. (See Box 1.)

Box 1 – Telefónica

Telefónica, a leading telecom service provider operating in 14 countries with more than 340 million customers, visualizes its operations in four layers or platforms, each offering welldefined capabilities:

- Platform 1 is the network infrastructure, with mobile and fixed network equipment, access and transport, and mobile spectrum. This layer is mapped into the countries where Telefónica operates.

- Platform 2 is the network services layer; it runs virtualized software systems, functions and databases that operate the company’s own and third-party network infrastructure equipment. This layer can be serviced by a single platform operating across different countries.

- Platform 3 is the applications layer, offering customers Telefónica and third-party services and applications (e.g., security, VOD from Movistar, and Netflix).

- Platform 4 is the data platform, providing information and intelligence from the massive amount of data generated in the networks.

Additionally, Telefónica announced a new organization in which two new B2B units would integrate a set of decoupled capabilities on a global scale – Telefónica Tech (focused on cybersecurity, the cloud, the Internet of Things and Big Data) and Telefónica Infra (with stakes in infrastructure vehicles serving Telefónica and third parties such as towers, greenfield fiber projects and data centers/edge networks). Telefónica Tech will leverage the muscle and local reach of the commercial teams in each country to sell its services, and through alliances, aims to export its capabilities to other countries where Telefónica is not present. Telefónica Infra’s ambition is to be one of the largest telecommunications infrastructure units in the world, exploiting the value of Telefónica’s and its partners’ portfolios of assets.

The successful companies of the future will be those that have mastered strategic capability management

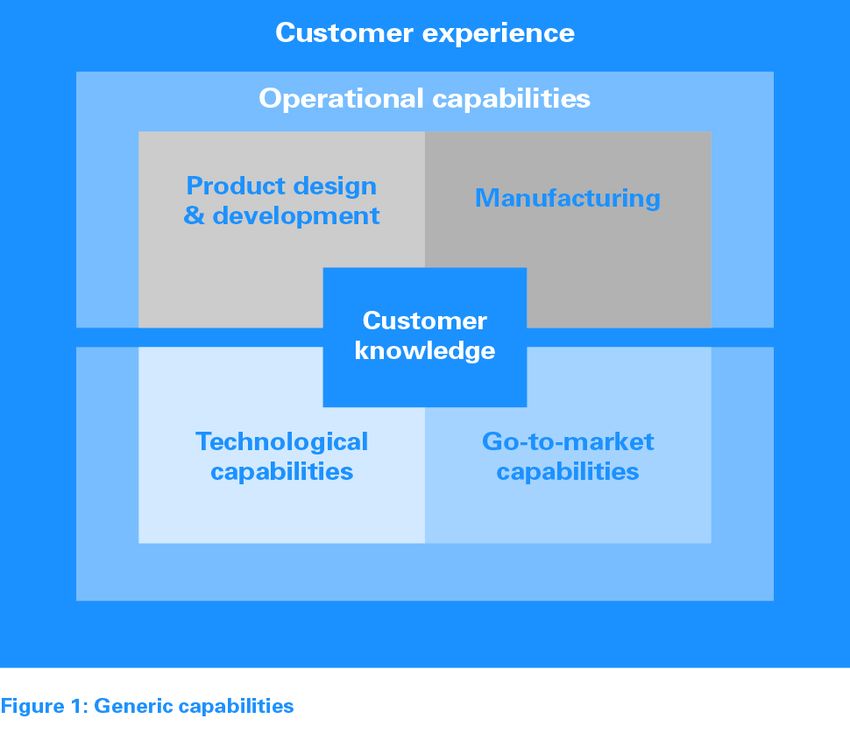

Decoupling capabilities means changing how companies structure and view themselves. Most companies need the generic capabilities shown in Figure 1.

It is striking that leading companies of today tend to focus on excelling in at least two of these generic capabilities: Apple in product design and customer experience; Amazon in operations, technological capabilities and customer experience; and Inditex in go-to-market and customer experience. Moving forward, the leading companies of tomorrow will all need to excel at least in customer experience, as well as have technology embedded in their DNA.

Looking at themselves in terms of capability “building blocks” allows companies to take a strategic view of where and how to optimize, as well as what part the external ecosystem can play. Companies can ensure they are the right size for each capability and possess the correct internal/external combination of technology, data, infrastructures, human expertise and facilities. This will be a competitive advantage because it will make them more efficient, creative, flexible and agile than integrated organizations.

We expect three different categories of capability-based players to arise:

- Orchestrators attract and align players on the demand side (consumers and business customers), the supply side, or both, at a scale that generates benefits for all. The capability-driven ecosystem model favors a few orchestrators dominating a space. Amazon has chosen to open its operational capabilities to third parties to become an orchestrator, with great success.

- Premium players can generate superior value by offering products, services and customer experience that match the material and emotional needs of carefully segmented consumer or business customer groups. Retailer Inditex, again with superb operational and customer experience capabilities, is a premium player in its ecosystem.

- Efficient players can now offload big parts of their organizational structures to focus on their cores. Efficiency is their main value driver, and the capabilitydriven approach can deliver substantial advantages versus the classical integrated model. Tata Consulting Services excels in operations and people management and competes as the leading commodity provider of IT outsourcing services.

Decoupling capabilities from business functions and working in ecosystems brings its own challenges. Choosing the differentiating capabilities and their target scale are difficult strategic decisions. Identifying the right partners and controlling the interfaces with them adds complexity. Moving from linear supplier-provider relationships to joint development and increased dependencies requires new management capabilities that go beyond the classic command-and-control model. Balancing creativity and efficiency becomes essential5.

However, we should expect technology to continue its rapid development and become even more pervasive. This will drive further decoupling of capabilities and functions because the cost to select and connect the required capabilities to perform any business function could be driven down to almost zero. Cheap access to data provides full visibility of end-to-end processes, which means the hidden costs of collaboration decrease and confidence increases. As automation progresses from the current wave of algorithms (in which simple tasks are automated) to autonomous machines (which solve problems and take decisions in real time), machines will engage in the majority of transactions. Building on the IT outsourcing analogy, the future could resemble the Lambda service from Amazon Web Services, in which each instruction demands computing resources, optimizing performance and eliminating all waste.

All of this means that for the company of the future, virtually all capabilities could be potentially decoupled, including such core capabilities as product development and go-to-market. Indeed, we see the ability to drive innovative approaches to capability management as a critical enabler.

The CEO agenda for the company of tomorrow

Getting the company ready to survive and succeed in “Tomorrowland”, only three to five years from now, is one of the biggest challenges for CEOs and their leadership teams. Although there is clearly no one-size-fits-all program, it is possible to identify some key imperatives. (See Figure 2.)

1. Continuously anticipate using the best tools and partners

Extrapolating from the past used to be a solid guide for the future. Today, companies need to learn how to continuously read the evolving dynamics of industries and ecosystems in a complex world of blurring industry boundaries. In natural ecosystems, species evolve and adapt, and the fittest thrive and survive. In business ecosystems, the clock is ticking orders of magnitude faster. In a hyper-competitive world, business ecosystems will favor three main drivers: disintermediation, collaboration, and the emergence of the best for each capability6.

Technologies that enable fluid collaboration will change at an accelerated speed, as will their adoption, occasionally jumping rather than following a smooth path as critical mass of adopters is reached. Being an early adopter or fast follower can provide a competitive advantage. However, in most instances being first is not necessary. When considering technology adoption, deciding when to follow will be as important as choosing when to lead in order to avoid wasting money and distracting the organization. Companies need to:

- Continuously read the context – through researching customer trends, technology maturity and adoption rates, as well as the economic, global trade and geopolitical environment. Thought leadership will be key.

- Decouple anticipation from any given business function so it can achieve a broad-enough context.

- Leverage automated tools, advanced analytics, human intelligence and ecosystem partners to anticipate, as well as create, a forward- and outside-looking attitude throughout the company culture. Most trends and disruptions becoming relevant on a five-year horizon are present now with innovators and early adopters. Connecting relevant dots from close and far references will be a critical skill.

2. Use an ecosystem lens to shape the required capabilities

The linear view of supply chains delivering products or services is not reflecting the multidimensional network realities of ecosystems, which are eroding and blurring industry borders and reshaping competitive landscapes. Companies must therefore now start building maps through this ecosystem lens:

- Map their organizational capabilities and then compare these to the ecosystems they are in. This will need to provide a fractal view of activities and assets of which end users and customers are at the center, how the status quo has changed, who is winning, and who is losing ground.

- Consider complementary providers and players connected with customers, either directly (B2C) or through other players (B2B2C or B2B). This will offer a new perspective of the world.

- Be flexible in adding, removing, scaling up and scaling down capabilities, as well as collaborating with ecosystem partners to boost efficiency and creativity. To decide which capabilities to own and which ones to source, companies should plan for at least two or three fractal levels below the main capability level. Dispose of assets and resources that do not provide differentiating or efficient capabilities, and source them from more efficient and creative ecosystem partners. Be willing to consider even the “sacred cows”.

- Data will be essential. Companies should be able to generate, process and share massive amounts of data securely and without friction. Only a few companies will replicate the provision of free services in exchange for data. Rather, winning companies will be able to run highly efficient operations, take better business decisions, and expand their businesses in new areas through their superior management of data.

3. Develop the ambidextrous organization and culture to perform in a “decoupled capabilities” ecosystem

People will still make the difference in the company of tomorrow. In the coming years, survival and success will rely on leveraging the talent and skills of human beings who can get the most out of technology. People and machines together will build high-value organizations to achieve excellence, not only in productivity and efficiency, but also in creativity, agility and collaboration.

It is important for companies to visualize this new world in simple terms. Imagine a company having 1,000 engineers in product development, working on 50 projects. It could open 30 of these projects to co-development with ecosystem partners, with 600 of its engineers collaborating with two or five times this number from specialized partners. This would allow the company to increase its product development capability by 60 percent, or up to 300 percent. It could also reduce headcount, freeing up expensive resources, while still accessing new projects with external resources. In any case, data, collaboration tools, an open culture, and agile and efficient project organizations will be necessary. Companies should:

- Mobilize and retrain their workforces at all levels of their organizations to shift to a new model in which teams running capabilities are highly accountable, with greater degrees of freedom to decide what to do in-house and what to leverage from selected partners.

- Through optimizing across internal and external capabilities, seek opportunities to run flatter, leaner and more projectdriven organizations.

- Redefine business processes for ecosystem operations, leveraging data centricity, automation, advanced analytics, and AI/ML.

As data becomes pervasive, real-time performance measurement and adjustments will become the new normal. The organization should adopt proven approaches to become “ambidextrous” – balancing efficiency with creativity through matching the right approaches to the different jobs to be done.

4. Review the future positioning and role of the company

The respective fates of Fujifilm and Kodak remind us that companies that fail to anticipate or change will be left behind or destroyed. Ecosystems require companies to be ready to evolve so they can adjust to opportunities and threats. Companies must decide where they want to play in three to five years, and how they will reach and defend the desired position in the ecosystems. The path to becoming an orchestrator or premium or commodity player will be greatly influenced by the purpose of the company. Companies should:

- Develop a clear and shared underlying sense of purpose (raison d’etre) to help guide positioning as the scope of products and services changes and evolves.

- Learn by doing and collaborating to help identify and reach preferred positions in the ecosystem. Move away from linear strategic thinking to a network, multidimensional model in which ecosystem players can be partners, competitors or both.

- Put suitable innovation structures in place to facilitate development and validation of major new strategic alternatives without their being stifled by corporate antibodies. These innovation structures will be integrated into the organization if and when needed7.

Insight for the executive

Companies of tomorrow will have leadership teams with shared visions. They will be comfortable adopting and leveraging technology and have the right attitudes to deal with uncertainty, as well as the ability to evolve to incorporate data-driven decisions.

CEOs transforming their companies by decoupling capabilities from business functions should receive understanding and support from shareholders and private investors if the equity story is properly assessed and executed. Private investment (activist) funds have also spotted the opportunities around disruption of value chains. They seek companies whose capabilities, as well as the ecosystems that they develop or play in, are worth more than their existing products and services – and target them accordingly.

For each industrial revolution to happen, many changes need to occur at different levels. Today, technologies and business paradigms are ready; professionals, managers and consumers are educated; infrastructures have been deployed; and institutional enablers such as investors and regulators are starting to accommodate change. CEOs therefore need to set the agenda or be left behind.

17 min read • Strategy

How to enable the company of tomorrow

Decoupling capabilities and leveraging the ecosystem

Businesses have traditionally organized themselves to ensure optimal effectiveness in each of their business functions. However, shorter product lifecycles, demand for customization, rising consumer expectations, and the growth of automation and data challenge this model. This article explains how success requires organizations to decouple capabilities from business functions, in order to deliver best-inclass performance and enable the company of tomorrow.

Based on demand from its 7,000+ shops in almost 100 countries, a prominent fast-fashion retailer ordered thousands of raincoats from its Asian suppliers. During the 11-hour flight that brought the coats to the logistics hub in Europe, they were reassigned to markets and shops based on actualized data that leveraged big data and AI, considering weather forecasts, exchange rates and other variables. In a hyper-efficient logistics center only a few kilometers from the airport, a logistics partner received the raincoat shipments and relabeled and folded them as needed for each market, shipping them for distribution to their final destinations in only a few hours.

In another example, a global smartphone provider considered it strategic to achieve and maintain a leading position in display technology and manufacturing. To ensure this, it supplied smartphone displays of its archrival in the market.

Inditex (Zara) and Samsung are both examples of how capabilities can be externalized or opened to the market. As data and technology are freely available and adopted by companies, collaboration with other companies to boost productivity and creativity for core and non-core capabilities can be achieved with less friction, transaction costs and risks than in the past. This is fundamentally changing how companies conceive, develop, produce, and deliver their products or integrate third-party products and services into their product build, operations, and offerings. Our analysis suggests that this externalization of capabilities – decoupling them from the company’s business functions and leveraging the ecosystem more profoundly – will transform companies, as well as the landscapes of many industries, in the next three to five years. In this article we examine what’s behind the trend and identify some imperatives for leaders to consider when transforming their own organizations.

Several trends are challenging the traditional way companies define themselves

Companies have traditionally organized themselves with the objective of ensuring optimal efficiency and effectiveness in each of their business functions (R&D, production, distribution and sales) to deliver defined products and services. However, three trends challenge this model:

- Products and services: shorter life cycles, a customization imperative

- Changing, more demanding customer expectations

- The rise of automation and a data-driven world

1. Products and services: Shorter life cycles, a customization imperative

With few exceptions, almost any product or service can now be replicated in months, rather than years. This makes it increasingly difficult to build sustainable competitive advantage on product features or qualities. Moreover, product customization is becoming a must in both B2B and B2C, not only around product features, but in all interactions. Blurring industry boundaries and the acceleration of time1 leave companies ever-shorter time frames to set up efficient and effective processes so they can monetize shortened product life cycles.

As a result, optimizing along the traditional value chain is not enough to ensure sustainable profitability. The ability to pivot rapidly and adjust to evolving ecosystems has become all but essential.

2. Changing, more demanding customer expectations

In today’s business environment, customers expect everything to be delivered immediately, wherever they happen to be. They value experiences (with focus on how their needs are met) above products. Loyalty is increasingly driven by digital perceptions and the emotions that brands create through the purposes and values they put forward – as well as how consistent their actions are with those values2.

As a result, customer experience and trust around expertise, quality and reputation become more relevant than the physical features of products and services. BMW’s memorable advertising campaign, “Do you enjoy driving?” captures the essence of this change.

Tailoring messages to customer expectations and needs is driving major change within marketing functions, forcing them to add new capabilities. Marketing has migrated from broadcasting to active listening and engaging in dialog with customers. The acquisition of Sapient (a technology integrator) by Publicis (an advertising agency) to create the “agency of the future” shows how players are responding in order to compete in this new ecosystem.

3. The rise of automation and a data-driven world

Customization would not be possible without data to understand and precisely forecast customer behavior, as well as automation to effectively deliver it. The amount of data that is being collected, processed and interpreted has exploded over the last decade3. Increasing automation will put data at the core of every business process.

The availability and affordability of standardized technology infrastructure (from players such as Amazon, Microsoft and Alibaba) mean companies don’t need to develop their own data-related capabilities. Inexpensive information processing lowers transaction costs and further facilitates decoupling of capabilities and business functions.

Extracting value from data (whether company generated or from open data sources, third parties or ecosystems) has therefore emerged as a new capability that pervades all business functions. Beyond well-known examples such as Google and Facebook, many traditional industrial companies such as Atlas Copco (which is leveraging data for its pressured air-as-a-service business) are building business models based on data.

Companies will increasingly define themselves in terms of their capabilities rather than their products

As a consequence of these trends, the companies of tomorrow are shifting from a set, linear position in a supply chain to one that dynamically adjusts within their ecosystem. They will focus more on how they conceive, develop, produce and take their products and services to market. This means decoupling business functions (aligned with what they do) from capabilities (how they do it) to deliver value. Companies will focus on what they can do best, operating in those areas at their optimal scale. They will leverage best-in-class ecosystem partners to boost their capabilities and externalize both key and non-critical ones. These innovative, adaptive companies will enjoy extra resilience in their operations and future prospects.

Decoupling capabilities from core business functions has a long history

Decoupling capabilities from business functions is nothing new in itself, and can be traced back to outsourcing of information technology-related processes from the late 1980s4. Efficient IT operations required skills, or capabilities at a scale, that non-specialized players could not achieve. Outsourcing contracts tended to be long-term commitments and covered a handful of functions. But despite all its limitations, outsourcing showed companies how they could decouple business functions from capabilities. It also created a new breed of companies that competed based on which could best provide some of these missing capabilities.

As outsourcing became an established practice and the reach of functions grew, operational reasons evolved to more strategic considerations. For example, hotel chains recognized that the capabilities required to manage real estate no longer provided any competitive advantage. Thus, they have freed financial resources by decoupling the ownership of “their” buildings, which are frequently sold to specialized asset management players. This allows the hotel chains to focus on aspects such as operations, brand and user experience (so-called “core competencies”). Decoupling also means companies can boost production by removing bottlenecks. Following this model, high-end fashion and luxury companies focus on brand management for their perfume product lines, leveraging product-design and manufacturing capabilities of third parties. Apple took advantage of the flexible capacity provided by contract manufacturers to meet the explosive demand prompted by the launch of the iPhone.

Sometimes, regulators have taken the lead. In many jurisdictions, energy utilities have been unbundled, which has separated their distribution activities from their retail activities, each requiring a different set of capabilities (optimizing asset utilization versus dealing with commodity price hedging and customer management).

An inflection point will cause costs and risks to drop drastically – as shown by early examples

However, whereas outsourcing and capability-based approaches have been around for decades, technology, connectivity, and the growing adoption of automation and AI are creating a new inflection point when the costs and risks of using complementary capabilities will be hugely reduced. The companies of tomorrow will therefore need to leverage new management approaches for optimal scale, cooperate with highly efficient and creative specialized ecosystem partners, or boost their internal capabilities. AI and advanced analytics will be critical.

Glimpses of these companies of tomorrow are already here, at different scales of adoption. A growing number of business decisions are aligned with this new logic. For example, Iberdrola, the number-one producer of wind power and one of the world’s biggest electricity utilities by market capitalization, has decoupled its renewables and networks arms so it can develop the first of these businesses on a global scale.

Some companies are already achieving extra sources of revenue by commercializing their in-house capabilities (“opening up the capability”). This helps gain scale and competitive advantage while minimizing the risk of failure. In addition to Amazon opening its information-processing and storage capabilities through Amazon Web Services, retail bank Banco Santander recently announced that it would open its payments platform to achieve the minimum scale required to compete.

The automotive sector provides a good example of extending collaboration from non-core to core capabilities. Here, the challenges around the transition from combustion engines to electric power trains and from ownership to access have forced traditional auto makers to reconsider their approaches. Demonstrating this, Daimler and BMW are pooling their noncore mobility services to create a new global player that will provide sustainable urban mobility for customers. They have also stated that they are sharing core engineering capabilities on driverless cars.

New entrants in every industry have taken full advantage of the opportunities provided by decoupling. Challenger banks, such as N26, focus on customer experience and rely on third parties for product development, regulatory compliance or IT platforms. Aryaka, a next-generation telecoms provider, concentrates on products and leverages connectivity and go-to-market channels from partners to reach its customers. Many small online retailers use Amazon’s platform to reach consumers.

Decoupling can also be used to build a new ecosystem. While Tesla’s initial insistence on being vertically integrated may seem to be in opposition to this trend, it actually recognizes that dominating certain capabilities is the way to build a position in a new industry. Panasonic building batteries in Tesla’s plant is another example of capabilities going beyond a firm’s walls. Tesla has opened its patents and published its roadmaps, demonstrating the importance of creating an ecosystem where your capability advantages can thrive.

Finally, in the telecoms industry, Telefonica is transforming itself from an integrated network and service operator to a capabilities- and platform-based business, splitting into a NetCo and an OpCo to take the best advantage of their respective capabilities. (See Box 1.)

Box 1 – Telefónica

Telefónica, a leading telecom service provider operating in 14 countries with more than 340 million customers, visualizes its operations in four layers or platforms, each offering welldefined capabilities:

- Platform 1 is the network infrastructure, with mobile and fixed network equipment, access and transport, and mobile spectrum. This layer is mapped into the countries where Telefónica operates.

- Platform 2 is the network services layer; it runs virtualized software systems, functions and databases that operate the company’s own and third-party network infrastructure equipment. This layer can be serviced by a single platform operating across different countries.

- Platform 3 is the applications layer, offering customers Telefónica and third-party services and applications (e.g., security, VOD from Movistar, and Netflix).

- Platform 4 is the data platform, providing information and intelligence from the massive amount of data generated in the networks.

Additionally, Telefónica announced a new organization in which two new B2B units would integrate a set of decoupled capabilities on a global scale – Telefónica Tech (focused on cybersecurity, the cloud, the Internet of Things and Big Data) and Telefónica Infra (with stakes in infrastructure vehicles serving Telefónica and third parties such as towers, greenfield fiber projects and data centers/edge networks). Telefónica Tech will leverage the muscle and local reach of the commercial teams in each country to sell its services, and through alliances, aims to export its capabilities to other countries where Telefónica is not present. Telefónica Infra’s ambition is to be one of the largest telecommunications infrastructure units in the world, exploiting the value of Telefónica’s and its partners’ portfolios of assets.

The successful companies of the future will be those that have mastered strategic capability management

Decoupling capabilities means changing how companies structure and view themselves. Most companies need the generic capabilities shown in Figure 1.

It is striking that leading companies of today tend to focus on excelling in at least two of these generic capabilities: Apple in product design and customer experience; Amazon in operations, technological capabilities and customer experience; and Inditex in go-to-market and customer experience. Moving forward, the leading companies of tomorrow will all need to excel at least in customer experience, as well as have technology embedded in their DNA.

Looking at themselves in terms of capability “building blocks” allows companies to take a strategic view of where and how to optimize, as well as what part the external ecosystem can play. Companies can ensure they are the right size for each capability and possess the correct internal/external combination of technology, data, infrastructures, human expertise and facilities. This will be a competitive advantage because it will make them more efficient, creative, flexible and agile than integrated organizations.

We expect three different categories of capability-based players to arise:

- Orchestrators attract and align players on the demand side (consumers and business customers), the supply side, or both, at a scale that generates benefits for all. The capability-driven ecosystem model favors a few orchestrators dominating a space. Amazon has chosen to open its operational capabilities to third parties to become an orchestrator, with great success.

- Premium players can generate superior value by offering products, services and customer experience that match the material and emotional needs of carefully segmented consumer or business customer groups. Retailer Inditex, again with superb operational and customer experience capabilities, is a premium player in its ecosystem.

- Efficient players can now offload big parts of their organizational structures to focus on their cores. Efficiency is their main value driver, and the capabilitydriven approach can deliver substantial advantages versus the classical integrated model. Tata Consulting Services excels in operations and people management and competes as the leading commodity provider of IT outsourcing services.

Decoupling capabilities from business functions and working in ecosystems brings its own challenges. Choosing the differentiating capabilities and their target scale are difficult strategic decisions. Identifying the right partners and controlling the interfaces with them adds complexity. Moving from linear supplier-provider relationships to joint development and increased dependencies requires new management capabilities that go beyond the classic command-and-control model. Balancing creativity and efficiency becomes essential5.

However, we should expect technology to continue its rapid development and become even more pervasive. This will drive further decoupling of capabilities and functions because the cost to select and connect the required capabilities to perform any business function could be driven down to almost zero. Cheap access to data provides full visibility of end-to-end processes, which means the hidden costs of collaboration decrease and confidence increases. As automation progresses from the current wave of algorithms (in which simple tasks are automated) to autonomous machines (which solve problems and take decisions in real time), machines will engage in the majority of transactions. Building on the IT outsourcing analogy, the future could resemble the Lambda service from Amazon Web Services, in which each instruction demands computing resources, optimizing performance and eliminating all waste.

All of this means that for the company of the future, virtually all capabilities could be potentially decoupled, including such core capabilities as product development and go-to-market. Indeed, we see the ability to drive innovative approaches to capability management as a critical enabler.

The CEO agenda for the company of tomorrow

Getting the company ready to survive and succeed in “Tomorrowland”, only three to five years from now, is one of the biggest challenges for CEOs and their leadership teams. Although there is clearly no one-size-fits-all program, it is possible to identify some key imperatives. (See Figure 2.)

1. Continuously anticipate using the best tools and partners

Extrapolating from the past used to be a solid guide for the future. Today, companies need to learn how to continuously read the evolving dynamics of industries and ecosystems in a complex world of blurring industry boundaries. In natural ecosystems, species evolve and adapt, and the fittest thrive and survive. In business ecosystems, the clock is ticking orders of magnitude faster. In a hyper-competitive world, business ecosystems will favor three main drivers: disintermediation, collaboration, and the emergence of the best for each capability6.

Technologies that enable fluid collaboration will change at an accelerated speed, as will their adoption, occasionally jumping rather than following a smooth path as critical mass of adopters is reached. Being an early adopter or fast follower can provide a competitive advantage. However, in most instances being first is not necessary. When considering technology adoption, deciding when to follow will be as important as choosing when to lead in order to avoid wasting money and distracting the organization. Companies need to:

- Continuously read the context – through researching customer trends, technology maturity and adoption rates, as well as the economic, global trade and geopolitical environment. Thought leadership will be key.

- Decouple anticipation from any given business function so it can achieve a broad-enough context.

- Leverage automated tools, advanced analytics, human intelligence and ecosystem partners to anticipate, as well as create, a forward- and outside-looking attitude throughout the company culture. Most trends and disruptions becoming relevant on a five-year horizon are present now with innovators and early adopters. Connecting relevant dots from close and far references will be a critical skill.

2. Use an ecosystem lens to shape the required capabilities

The linear view of supply chains delivering products or services is not reflecting the multidimensional network realities of ecosystems, which are eroding and blurring industry borders and reshaping competitive landscapes. Companies must therefore now start building maps through this ecosystem lens:

- Map their organizational capabilities and then compare these to the ecosystems they are in. This will need to provide a fractal view of activities and assets of which end users and customers are at the center, how the status quo has changed, who is winning, and who is losing ground.

- Consider complementary providers and players connected with customers, either directly (B2C) or through other players (B2B2C or B2B). This will offer a new perspective of the world.

- Be flexible in adding, removing, scaling up and scaling down capabilities, as well as collaborating with ecosystem partners to boost efficiency and creativity. To decide which capabilities to own and which ones to source, companies should plan for at least two or three fractal levels below the main capability level. Dispose of assets and resources that do not provide differentiating or efficient capabilities, and source them from more efficient and creative ecosystem partners. Be willing to consider even the “sacred cows”.

- Data will be essential. Companies should be able to generate, process and share massive amounts of data securely and without friction. Only a few companies will replicate the provision of free services in exchange for data. Rather, winning companies will be able to run highly efficient operations, take better business decisions, and expand their businesses in new areas through their superior management of data.

3. Develop the ambidextrous organization and culture to perform in a “decoupled capabilities” ecosystem

People will still make the difference in the company of tomorrow. In the coming years, survival and success will rely on leveraging the talent and skills of human beings who can get the most out of technology. People and machines together will build high-value organizations to achieve excellence, not only in productivity and efficiency, but also in creativity, agility and collaboration.

It is important for companies to visualize this new world in simple terms. Imagine a company having 1,000 engineers in product development, working on 50 projects. It could open 30 of these projects to co-development with ecosystem partners, with 600 of its engineers collaborating with two or five times this number from specialized partners. This would allow the company to increase its product development capability by 60 percent, or up to 300 percent. It could also reduce headcount, freeing up expensive resources, while still accessing new projects with external resources. In any case, data, collaboration tools, an open culture, and agile and efficient project organizations will be necessary. Companies should:

- Mobilize and retrain their workforces at all levels of their organizations to shift to a new model in which teams running capabilities are highly accountable, with greater degrees of freedom to decide what to do in-house and what to leverage from selected partners.

- Through optimizing across internal and external capabilities, seek opportunities to run flatter, leaner and more projectdriven organizations.

- Redefine business processes for ecosystem operations, leveraging data centricity, automation, advanced analytics, and AI/ML.

As data becomes pervasive, real-time performance measurement and adjustments will become the new normal. The organization should adopt proven approaches to become “ambidextrous” – balancing efficiency with creativity through matching the right approaches to the different jobs to be done.

4. Review the future positioning and role of the company

The respective fates of Fujifilm and Kodak remind us that companies that fail to anticipate or change will be left behind or destroyed. Ecosystems require companies to be ready to evolve so they can adjust to opportunities and threats. Companies must decide where they want to play in three to five years, and how they will reach and defend the desired position in the ecosystems. The path to becoming an orchestrator or premium or commodity player will be greatly influenced by the purpose of the company. Companies should:

- Develop a clear and shared underlying sense of purpose (raison d’etre) to help guide positioning as the scope of products and services changes and evolves.

- Learn by doing and collaborating to help identify and reach preferred positions in the ecosystem. Move away from linear strategic thinking to a network, multidimensional model in which ecosystem players can be partners, competitors or both.

- Put suitable innovation structures in place to facilitate development and validation of major new strategic alternatives without their being stifled by corporate antibodies. These innovation structures will be integrated into the organization if and when needed7.

Insight for the executive

Companies of tomorrow will have leadership teams with shared visions. They will be comfortable adopting and leveraging technology and have the right attitudes to deal with uncertainty, as well as the ability to evolve to incorporate data-driven decisions.

CEOs transforming their companies by decoupling capabilities from business functions should receive understanding and support from shareholders and private investors if the equity story is properly assessed and executed. Private investment (activist) funds have also spotted the opportunities around disruption of value chains. They seek companies whose capabilities, as well as the ecosystems that they develop or play in, are worth more than their existing products and services – and target them accordingly.

For each industrial revolution to happen, many changes need to occur at different levels. Today, technologies and business paradigms are ready; professionals, managers and consumers are educated; infrastructures have been deployed; and institutional enablers such as investors and regulators are starting to accommodate change. CEOs therefore need to set the agenda or be left behind.

RELATED INFORMATION

The Company of Tomorrow

The COVID-19 crisis hit the world as this edition of Prism was in preparation. Needless to say, the outlook for business, at least in the short term, has changed radically in just a few weeks.…

BUILDING THE BATTERY ECOSYSTEM OF TOMORROW

Combining technology, scale-up capabilities, and capital to power change Realizing the strategic importance of batteries, Western governments are aiming to build their own ecosystems, competing (and…

Ten management priorities for today and tomorrow

Now that the dust of the global financial crisis has begun to settle, many business leaders are wondering what their next steps should be in the lingering atmosphere of uncertainty. With the heavy…