DOWNLOAD

17 min read •

Strategy: How to cope with the uncertainties of tomorrow’s new world

Planning for the future has never been more difficult given the unstable and uncertain global environment that businesses face at both a macro and micro level. Based on insights from client conversations and internal experts, we outline the range of potential scenarios organizations could face, along with guidance and best practice on making strategic decisions in tomorrow’s new world.

When the dust of the COVID-19 crisis finally starts to settle, we will face a new environment that may vary dramatically from what we know today in terms of consumer behaviors, business models and the respective roles of the state and private sector. The longer and deeper the crisis, the more likely that profound changes will define tomorrow’s new world.

When the dust of the COVID-19 crisis finally starts to settle, we will face a new environment that may vary dramatically from what we know today in terms of consumer behaviors, business models and the respective roles of the state and private sector. The longer and deeper the crisis, the more likely that profound changes will define tomorrow’s new world.

Drawing on insights from our client network and internal experts, we have tried to map these changes and outline the range of very different future possible scenarios. In such an uncertain environment, strategic decision-making is challenging, so we have also provided guidance on how to approach this, based on well-established principles.

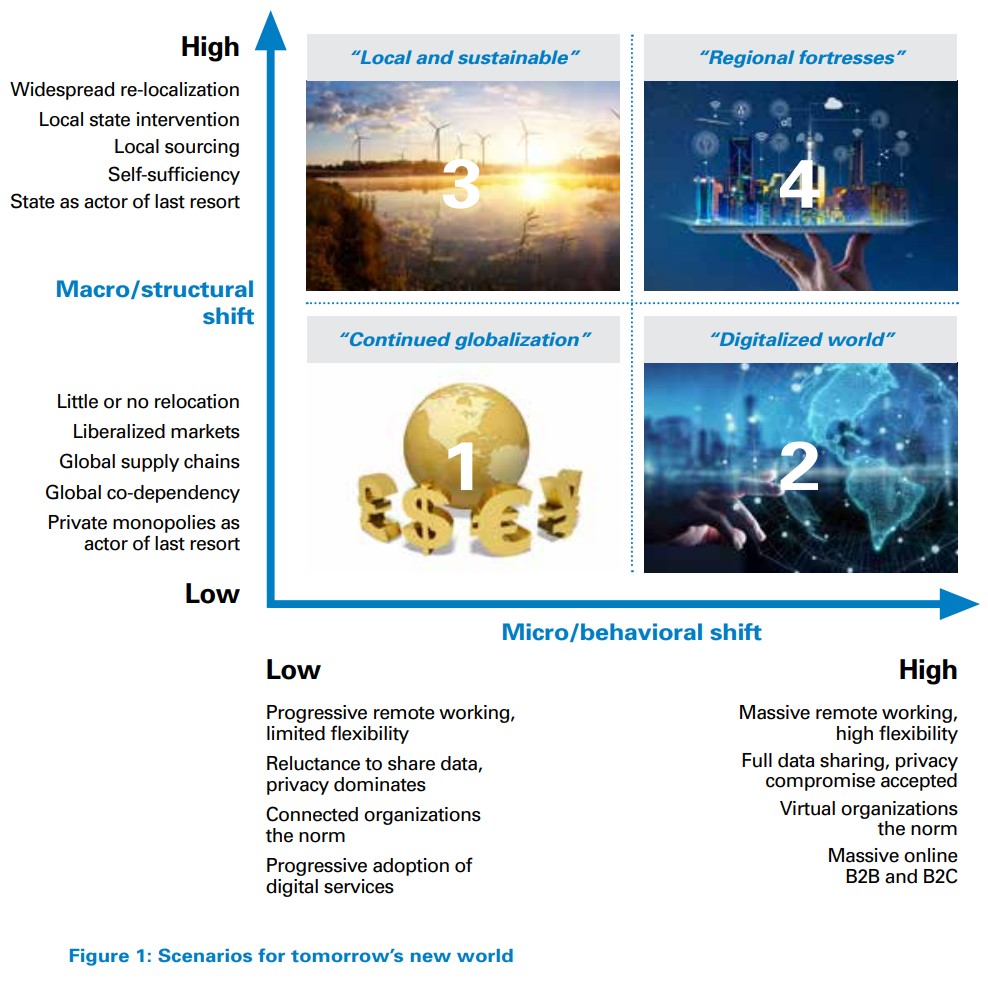

Thrown into a world of uncertainties

After the initial period of fast adaptation, companies across the globe are reflecting on what the new world might look like in the next few years. Tomorrow’s world will be shaped by both highly probable trends (such as greater working from home and more e-commerce) and other high-impact trends whose potential development is much more uncertain. A helpful way to consider these trends is to group them into two dimensions:

- Macro/structural level: Trends relating to economic structural and policy shifts, characterized especially by states and large companies wanting to reduce their global interdependency risks.

- Micro/behavioral level: Trends relating to sustained behavioral shifts among citizens as both consumers and workers, resulting initially from their experiences of lockdown and social distancing.

(1) Macro/structural level: Will we see a structural shift towards relocalization?

As countries cautiously begin to lift restrictions on lockdown and movement across borders, governments are focusing intensively on measures to limit economic and social damage while continuing to control public-health risks. Governments in many countries have already taken a huge stake in business through direct funding of furloughed employees. In the turmoil of the coming economic recession they may need to increase their economic involvement substantially and apply new policies and regulations that will change the open, global free-trade market dynamic we know today. In parallel, large international companies will also be looking to increase organizational robustness, potentially through the relocalization of their operations, to hedge against future major disruptions:

Technological sovereignty: The COVID-19 crisis revealed to European and US citizens (and their governments) their high dependency on China and other Asian countries to supply protective equipment and pharmaceuticals. This is particularly true for strategic supplies such as masks and medicines – for example, according to the US Department of Commerce, 97 percent of all antibiotics in the US come from China. In response, many governments have committed themselves to greater control over the production and provision of these products. However, it is unclear to what extent these current intentions and commitments will be realized in practice and extended to other products and services:

- What will be the scope and extent of technological sovereignty shifts in terms of actual relocalization of production? What technologies and sectors will be covered, beyond the pharmaceutical and healthcare industries?

State intervention: Before the crisis, globalization was accelerating across most regions, with developed economies displacing manufacturing to low-cost countries. Faced with bankruptcies, galloping national debt and unheard-of levels of unemployment, governments are likely to be tempted towards protectionist measures that salvage returns on emergency loans and shore up local industries. Even before the crisis, there were incipient trade wars between the US and China, and governments in many countries have been increasingly voicing ambitions to take back control over the development of strategic economic sectors, for example, by promoting local/regional champions or through incentives to invest in local infrastructure:

- How far will governments keep their faith in global free markets to drive recovery, versus adopting ever-greater protectionist measures?

Environmental economics: The crisis hit at a time when climate-change concerns were rapidly moving up the policy agenda, and these concerns are here to stay. Governments in Europe, the US, and Japan have been used to transferring “dirty” industries to China and Asia, while imposing stricter environmental regulations on their own industries. This cost burden contributed to a lack of competitiveness in Europe and other western countries (e.g., producing one ton of hotrolled steel from a blast furnace is 13 percent more expensive when CO2 emissions are taxed at 30/ton). There has already been intensive lobbying to relax environmental norms. Given economic distress, European and western governments may be tempted to use regulation to favor growth and relocalization over environmental economics:

- How will the economic downturn affect policies? Will governments compromise on global environmental standards out of economic necessity, or will the reality of climate change force them instead to compromise on short-term economic well-being?

Operational robustness: The COVID-19 crisis highlighted the strong reliance of companies on long, complex global supply chains. Many companies whose logistical flows collapsed may consider refocusing, at least partially, on closer supply chains. Even before the lockdown, some European industrial companies (such as in the automotive sector) had concerns about global supply-chain vulnerabilities. However, operational relocation is costly and introduces new risks:

- Will companies only relocalize limited parts of their operations to hedge against future disruption, or will they aim to develop fully local supply chains as alternatives to current global ones?

(2) Micro/behavioral level: How disruptive and permanent will the behavioral shift be?

In the context of lockdowns and social distancing, our behaviors as consumers have already changed in ways that were previously unheard of. Companies have also already changed the way they do business so they can operate safely for employees and customers. The longer these measures last, the more likely the shift will become, at least in some respects, irreversible. We expect that the following aspects will be especially impactful for businesses:

Accelerated digitalization: The step-change in digital interactivity is the most obvious and direct behavioral change we have seen so far. Many services and utilities have switched from on-site to online access overnight: education, public administration, legal advice, consulting and even medical appointments. This growth in digital interactions would have been unimaginable only a few months ago, and represents a jump into the future of between two and 10+ years, according to different observers. The CEO of British Land, Chris Grigg, who manages one of Britain’s biggest retail and office landlords, says that as a result of the pandemic his company has significantly brought forward the time when it expects the share of online shopping in Britain to reach almost 40 percent – double its current level. Augmented realityand virtual reality-enabled (AR/VR) technologies are breaking through as online retailers and service professionals test new ways to provide their services. The longer restrictions last, the more sustained adoption is likely to be. However, people still have a strong basic need for physical contact:

- As lockdown measures are progressively relaxed, how much will people continue to accept and embrace digital channels, rather than meeting their needs for physical interaction?

Local and “slow” life: Most people are experiencing a new home-based life. Remote working, which was already growing steadily (close to 50 percent over the past five years in the US), has exploded. Some consumers have had to change their purchasing habits and buy local products as retail stores experienced shortages of imported goods. Online stores run by local farmers have seen a boom in business as short food supply chains proved more resilient than traditional ones. One of the few upsides of the pandemic has been that people have started to realize the benefits of the absence of traffic – substantially reduced pollution, lower noise levels and, for many, the absence of commuting. However, this has all happened in the context of a massive drop in economic activity, the pain of which has yet to be felt by most:

- To what extent will companies and citizens sustain the shift towards local living and working, and will environmental/wellbeing criteria become more significant in consumption and lifestyle choices?

Data privacy: Lockdown has translated into a brutal loss of freedom, which we have accepted to collectively protect our health. The imposition of intrusive tracking-and-tracing tools may be a necessary price to pay if people are to be free to move while the virus is still globally active. In parallel, the accelerated development of digital services will lead companies to look to access even more of our personal data, fueling a trend that was already prevalent. These factors are already the subject of significant debate:

- Will people ultimately accept less data privacy for public health and convenience/lifestyle reasons, or will new safeguards and restrictions need to be imposed by public authorities to reflect their concerns?

Investment and entrepreneurship: In recent years, fueled by low interest rates, creative financial engineering and leveraging have been the keystone to delivering shareholder value; this has been demonstrated by share buybacks, debtand equity-backed acquisitions, industry consolidations and huge valuations for loss-making unicorns with winner-takes-all business models. With massive financial support provided by governments to distressed sectors, citizens may require governments to limit the debt levels and dividend payments of companies supported by their taxpayer dollars. A severe economic downturn may lead to risk aversion in investment decisions, with investments concentrated in sectors labeled strategic by public authorities. On the other hand, investors and governments may also take the opportunity to invest in innovative breakthrough business models and technologies as society adapts to survive:

- To what extent will investors become more risk averse (by choice or regulation), rather than funding breakthroughs and fueling a new wave of entrepreneurial investment?

The combination of these two uncertainty dimensions (the degree of macro/structural and micro/behavioral changes), both of which will be impacted by the length and depth of the crisis, potentially produce very different market environments for businesses. We will explore these in the next section.

The new world – What are the scenarios?

We have illustrated the uncertain world of tomorrow with four scenarios, which represent different combinations of macro and micro shifts. These scenarios all require different strategic responses from businesses.

Scenario #1 – Continued globalization

In Scenario #1, rapid progress in eliminating the virus and a relatively fast economic recovery leads to a return to the key patterns of a globalized economy:

- The economic downturn and limited investment capacity increase the consolidation of economic power into the hands of a small number of giant corporations, including tech leaders such as Amazon, Netflix, Google, Baidu and others. These continue to pursue optimization and efficiency via global supply chains.

- High unemployment rates, low investment capacity and the high cost of debt to the rest of the economy hinders further acceleration of digitalization beyond pre-crisis levels.

- Investment in digital services continues along its previous path, but with a clear and more rigorous focus on short-term return on investment.

- Society’s reluctance to share personal data justifies stringent data-privacy norms, limiting the speed of further economic digitalization.

- Climate-change priorities are still high, but tempered by the need to alleviate short-term economic hardship.

Scenario #1 would not drastically change the key ingredients of the economy and markets, but would mean that private monopolies would act even more as the actor of last resort.

Scenario #2 – Digitalized world

In Scenario #2, a protracted recovery period or failure to find a full solution to the pandemic drives rapid acceleration of digitalization, leading to more permanent changes in the global economy:

- Massive adoption of digital services and other means of securing social distancing, including drastic robotification and remote/flexible working with virtual organizations, become the norm.

- Companies and supply chains are not just connected, but completely digitalized.

- Governments temper protectionist and interventionist policies to enable global free markets to help drive economic recovery, focusing instead on managing the collateral damage from the collapse of distressed legacy sectors.

- Privacy norms are sacrificed to the common interest and private data is made fully available to secure optimal efficiency and fluidity of B2C, B2B and B2G online services such as e-care, e-justice and advisory services.

- The remaining investment capacity of corporations and private-equity firms focuses on new breakthrough technologies and business models, driven by the necessity for radical change.

- Climate-change priorities drive fundamental transformation of the global economy towards sustainable technologies in areas such as energy, mobility and manufacturing.

Scenario #2 effectively continues the trend of the NYSE FANG+ Index, which has outperformed the market this year by up to 12 percent on average, compared to a double-digit drop for the S&P 500. As another example, digital-health funding has already grown by 50 percent in 2020 Q1 year on year, with $3.1B invested. In Scenario #2 the major global digital private players would further accelerate their strong growth.

Scenario #3 – Local and sustainable

In Scenario #3, the combination of a deep recession, high state protectionism, and a public preference for “slower life” causes a reaction against further globalization and drives a focus on developing sustainable local communities:

- Stronger state intervention incentivizes local sourcing and reduces dependency on the global economy.

- Climate change and corporate social responsibility issues are seen as higher priority than economic growth.

- Digitalization progresses, but at a similar rate to precrisis levels, with careful prioritization limited by available investment.

- Organizations and their customers are connected, but they do not become virtual – human contact is still the norm.

- Experiences during lockdown leave a legacy of public preference for localism and stronger awareness of the environmental and personal benefits of less travel, local consumption, less waste and self-sufficiency.

- Lack of investment capacity and economic hardship contribute to a focus on developing the local economy, specializing as required to be competitive for trade and gain access to vital or innovative imports.

- Data-privacy concerns remain strong, with employment as a key priority versus radical technology development.

As an example, some of the principles in Scenario #3 can be found today in Sweden, with its ReGen Villages. As another example, incentivization of local sourcing and reducing reliance on the global economy is already planned by the Bank of Japan.

Scenario #4 – Regional fortresses

In Scenario #4, a protracted recovery period or prolonged failure to find a full solution to the virus drives not only acceleration of digitalization, but also the formation of regional clusters driven by greater state intervention and protectionism as governments look to increase resilience to global shocks:

- Stronger protectionism and state intervention, with the state as the actor of last resort, securing strategic sectors and supporting industries, companies and the economy in fighting threats.

- As in Scenario #2, acceleration of digital and smart technology is a key lever to secure local or regional economic growth, self-sufficiency and local sourcing. Thanks to robotics, regions are able to reshore most of their activity and use digital channels and robots to make cities more efficient and productive.

- “Smartization” of public services is accelerated, including health and infrastructure, as well as robotization of services such as restaurants and stores.

- Privacy norms are sacrificed to the common interest, with private data made fully available to enable digital development.

- Investment, led by cities and regional clusters, focuses on new breakthrough technologies and business models, driven by the necessity for radical change and redeployment.

- Local technology-driven companies are the new champions of a self-sufficient, multi-local world, with the power of global corporations restricted through local regulations.

- Climate-change priorities are pursued through government support to national/regional technology investment and behavior-change efforts.

Although Singapore is not yet as sophisticated as we describe in this scenario, the early response of the city-state to COVID-19, mainly built on strong digital foundations, illustrates some of its features. Singapore has been recognized as very efficient in addressing the surveillance, prevention, diagnosis and treatment stages of the pandemic, as detailed by the United Nations Development Programme (UNDP). The government used contact-tracing technology, with geographic and demographic data shared with the population to encourage people to seek healthcare in case of virus exposure. A range of apps and platforms were used to provide detailed information and stay in touch with the population, while buildings were equipped with diagnostic technologies.

What does this mean for strategy?

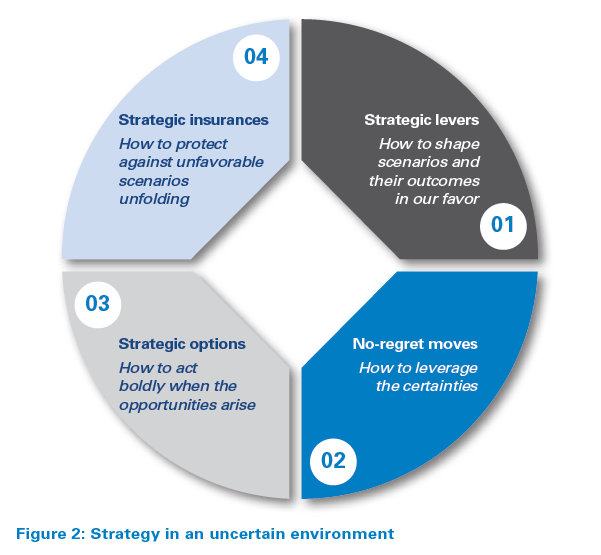

As the saying goes, “It is difficult to make predictions, especially about the future”. The range of potential scenarios shows that companies need to embed uncertainty into their strategic decision-making approaches. In working with hundreds of large companies over the last 20 years, we have found that there is a proven methodology for achieving this, which remains effective today.

As shown in Figure 2, the essence of this is to formulate four types of strategic moves, while realizing that in any scenarioplanning exercise, the actual outcome is more likely to be a combination of elements rather than conforming to a single stereotype:

1. Strategic levers – How to shape scenarios and their outcomes in our favor?

First, companies need to leverage the power they possess to influence and shape scenarios in ways that are favorable to them. For example:

- Companies active in the production of medical supplies (such as hydroalcoholic gel) have already engaged with public authorities on the conditions necessary to develop and maintain local/regional production.

- Digital actors are already promoting their solutions (such as e-health platforms, e-education, and individual track & trace) to public authorities and local ecosystems as ways to improve regions’ and cities’ resilience against pandemics. They are also negotiating the frameworks for changes to digital privacy regulation, thereby shaping the future towards a “Regional fortresses” scenario.

- Telecom network operators are positioning themselves as a “critical” sector (enablers of e-education, workfrom- home, robotization, etc.) to secure state subsidies or favorable regulations to accelerate the deployment of fiber-to-the-home and 5G, thereby promoting the “Digitalized world” and “Regional fortresses” scenarios.

2. No-regret moves – How to leverage the certainties?

However, while many uncertainties exist, some things will be fairly certain in all scenarios. For example, today it is almost guaranteed that there will be an increase in workplace virtualization, along with a significant global economic downturn. Any strategy will need to address these issues.

The need for organizations to balance agility and productivity will be critically important to respond rapidly to ongoing changes in a difficult economic climate.

In some cases, distressed competitors or suppliers represent a unique opportunity to acquire strategic competencies (patents, technologies, expertise) that will be key whatever scenario unfolds. Embedding uncertainty management into decision-making processes and governance is compulsory to navigate through the crisis, as well as more fundamentally to thrive in an increasingly volatile world.

3. Strategic options – How to act boldly when opportunities arise?

The aim here is to be ready to make bold moves as trigger points of favorable scenarios are reached. This involves identifying strategic moves with limited upfront investment but massive potential for rapid upscaling. By projecting the company into the most likely scenarios, clear strategic directions can be defined and the company’s future business and operating models shaped. This starts with monitoring promising business models and technologies that are emerging during the crisis, with a view to, for example, taking minority stakes or initially entering partnerships. For example:

- Retail and B2B companies might develop proofs of concept for online personalized AR-/VR-enabled sales and distribution to meet new physical-distancing needs.

- Services companies (e.g., lawyers, notaries, consultants, insurance agents, health professionals) might invest in technical platforms and pilot teams to switch to online provision of (most of) their services, as soon as the first trigger points of the “Digitalized world” or “Regional fortresses” scenarios occur.

- If either the “Local and sustainable” or “Regional fortresses” scenarios begin to unfold, food retailers could prepare their own local-sourcing ecosystems and smart-city suppliers could prepare to double down on their growth investments.

4. Strategic insurance – How to protect against unfavorable scenarios unfolding?

Finally, one of the aspects often poorly addressed in strategic planning is strategic “insurance”. Against an uncertain and unwanted outcome, you insure yourself. Targeted actions can be taken to mitigate the negative impact of unwanted scenarios. For example:

- Companies with globalized production chains could launch robotization pilots to mitigate labor-cost increases due to forced re-localization to higher labor-cost markets.

- Companies could develop plans and establish preliminary contacts/proofs of concept for multisupplier and multi-geographical set-up of their sourcing strategies to pre-empt any losses of competitiveness in case of the “Local and sustainable” or “Regional fortresses” scenarios.

- Businesses could also secure potential access to contracts and/or markets for which public authorities might impose pre-qualification requirements (e.g., localization and security of data storage, minimal production/delivery capacity within the region, backup facilities, formal safety and risk management certifications). Again, the aim is to invest a little upfront to ensure that the company is able to protect itself, rather than deploying costly full-scale back-up plans.

The above approach allows companies to embrace the complexity related to uncertainties, providing clear decision frameworks and linking decision points to events that will trigger the (progressive) unfolding of one or more scenarios. In periods of high uncertainty such as the current crisis, the best-prepared first movers can build substantial competitive advantage, either through minimizing exposure to losses or by capturing the lion’s share of new opportunities.

Insight for the executive

The crisis we are facing is certainly deeper than most of us have seen in our lifetimes. However, despite the hardship and tragedy, there will ultimately be new opportunities, as well as challenges. To prepare for these, leaders need to maintain a broad perspective:

- Look beyond the short-term crisis and start preparing for the new world as structural and behavioral changes begin to significantly reshape the business environment.

- Do not only focus on the most obvious trends, but also assess the major areas of uncertainty and their implications.

- Use the full breadth of strategic plays. Most executives tend to focus on developing strategic options, but they overlook the three other strategic plays: shaping the scenarios, making swift no-regret moves and, especially, developing strategic insurance to mitigate unwanted scenarios.

- Do not try to over-simplify complexity related to uncertainties, but instead embrace it and embed uncertainty management into decision-making:

- Develop capabilities for scenario development and monitoring of trigger events.

- Adjust strategic and operational planning and related governance mechanisms.

- Shape the culture of the organization to help employees deal with uncertainty.

- Strengthen the “ambidextrous” capability of the organization to encourage creativity and responsiveness to change, as well as efficiency and productivity.

- Adapt partner and ecosystem management in terms of both communication around uncertainties and redeployment of capabilities.

- Leverage the potential of digital technologies to improve intelligence and increase agility and responsiveness.

The future is full of complexity and uncertainty. Companies need to embrace this and – underpinned by a clear vision and set of values – be prepared to make radical changes to their products, services and processes as they go forward.

17 min read •

Strategy: How to cope with the uncertainties of tomorrow’s new world

Planning for the future has never been more difficult given the unstable and uncertain global environment that businesses face at both a macro and micro level. Based on insights from client conversations and internal experts, we outline the range of potential scenarios organizations could face, along with guidance and best practice on making strategic decisions in tomorrow’s new world.

When the dust of the COVID-19 crisis finally starts to settle, we will face a new environment that may vary dramatically from what we know today in terms of consumer behaviors, business models and the respective roles of the state and private sector. The longer and deeper the crisis, the more likely that profound changes will define tomorrow’s new world.

Drawing on insights from our client network and internal experts, we have tried to map these changes and outline the range of very different future possible scenarios. In such an uncertain environment, strategic decision-making is challenging, so we have also provided guidance on how to approach this, based on well-established principles.

Thrown into a world of uncertainties

After the initial period of fast adaptation, companies across the globe are reflecting on what the new world might look like in the next few years. Tomorrow’s world will be shaped by both highly probable trends (such as greater working from home and more e-commerce) and other high-impact trends whose potential development is much more uncertain. A helpful way to consider these trends is to group them into two dimensions:

- Macro/structural level: Trends relating to economic structural and policy shifts, characterized especially by states and large companies wanting to reduce their global interdependency risks.

- Micro/behavioral level: Trends relating to sustained behavioral shifts among citizens as both consumers and workers, resulting initially from their experiences of lockdown and social distancing.

(1) Macro/structural level: Will we see a structural shift towards relocalization?

As countries cautiously begin to lift restrictions on lockdown and movement across borders, governments are focusing intensively on measures to limit economic and social damage while continuing to control public-health risks. Governments in many countries have already taken a huge stake in business through direct funding of furloughed employees. In the turmoil of the coming economic recession they may need to increase their economic involvement substantially and apply new policies and regulations that will change the open, global free-trade market dynamic we know today. In parallel, large international companies will also be looking to increase organizational robustness, potentially through the relocalization of their operations, to hedge against future major disruptions:

Technological sovereignty: The COVID-19 crisis revealed to European and US citizens (and their governments) their high dependency on China and other Asian countries to supply protective equipment and pharmaceuticals. This is particularly true for strategic supplies such as masks and medicines – for example, according to the US Department of Commerce, 97 percent of all antibiotics in the US come from China. In response, many governments have committed themselves to greater control over the production and provision of these products. However, it is unclear to what extent these current intentions and commitments will be realized in practice and extended to other products and services:

- What will be the scope and extent of technological sovereignty shifts in terms of actual relocalization of production? What technologies and sectors will be covered, beyond the pharmaceutical and healthcare industries?

State intervention: Before the crisis, globalization was accelerating across most regions, with developed economies displacing manufacturing to low-cost countries. Faced with bankruptcies, galloping national debt and unheard-of levels of unemployment, governments are likely to be tempted towards protectionist measures that salvage returns on emergency loans and shore up local industries. Even before the crisis, there were incipient trade wars between the US and China, and governments in many countries have been increasingly voicing ambitions to take back control over the development of strategic economic sectors, for example, by promoting local/regional champions or through incentives to invest in local infrastructure:

- How far will governments keep their faith in global free markets to drive recovery, versus adopting ever-greater protectionist measures?

Environmental economics: The crisis hit at a time when climate-change concerns were rapidly moving up the policy agenda, and these concerns are here to stay. Governments in Europe, the US, and Japan have been used to transferring “dirty” industries to China and Asia, while imposing stricter environmental regulations on their own industries. This cost burden contributed to a lack of competitiveness in Europe and other western countries (e.g., producing one ton of hotrolled steel from a blast furnace is 13 percent more expensive when CO2 emissions are taxed at 30/ton). There has already been intensive lobbying to relax environmental norms. Given economic distress, European and western governments may be tempted to use regulation to favor growth and relocalization over environmental economics:

- How will the economic downturn affect policies? Will governments compromise on global environmental standards out of economic necessity, or will the reality of climate change force them instead to compromise on short-term economic well-being?

Operational robustness: The COVID-19 crisis highlighted the strong reliance of companies on long, complex global supply chains. Many companies whose logistical flows collapsed may consider refocusing, at least partially, on closer supply chains. Even before the lockdown, some European industrial companies (such as in the automotive sector) had concerns about global supply-chain vulnerabilities. However, operational relocation is costly and introduces new risks:

- Will companies only relocalize limited parts of their operations to hedge against future disruption, or will they aim to develop fully local supply chains as alternatives to current global ones?

(2) Micro/behavioral level: How disruptive and permanent will the behavioral shift be?

In the context of lockdowns and social distancing, our behaviors as consumers have already changed in ways that were previously unheard of. Companies have also already changed the way they do business so they can operate safely for employees and customers. The longer these measures last, the more likely the shift will become, at least in some respects, irreversible. We expect that the following aspects will be especially impactful for businesses:

Accelerated digitalization: The step-change in digital interactivity is the most obvious and direct behavioral change we have seen so far. Many services and utilities have switched from on-site to online access overnight: education, public administration, legal advice, consulting and even medical appointments. This growth in digital interactions would have been unimaginable only a few months ago, and represents a jump into the future of between two and 10+ years, according to different observers. The CEO of British Land, Chris Grigg, who manages one of Britain’s biggest retail and office landlords, says that as a result of the pandemic his company has significantly brought forward the time when it expects the share of online shopping in Britain to reach almost 40 percent – double its current level. Augmented realityand virtual reality-enabled (AR/VR) technologies are breaking through as online retailers and service professionals test new ways to provide their services. The longer restrictions last, the more sustained adoption is likely to be. However, people still have a strong basic need for physical contact:

- As lockdown measures are progressively relaxed, how much will people continue to accept and embrace digital channels, rather than meeting their needs for physical interaction?

Local and “slow” life: Most people are experiencing a new home-based life. Remote working, which was already growing steadily (close to 50 percent over the past five years in the US), has exploded. Some consumers have had to change their purchasing habits and buy local products as retail stores experienced shortages of imported goods. Online stores run by local farmers have seen a boom in business as short food supply chains proved more resilient than traditional ones. One of the few upsides of the pandemic has been that people have started to realize the benefits of the absence of traffic – substantially reduced pollution, lower noise levels and, for many, the absence of commuting. However, this has all happened in the context of a massive drop in economic activity, the pain of which has yet to be felt by most:

- To what extent will companies and citizens sustain the shift towards local living and working, and will environmental/wellbeing criteria become more significant in consumption and lifestyle choices?

Data privacy: Lockdown has translated into a brutal loss of freedom, which we have accepted to collectively protect our health. The imposition of intrusive tracking-and-tracing tools may be a necessary price to pay if people are to be free to move while the virus is still globally active. In parallel, the accelerated development of digital services will lead companies to look to access even more of our personal data, fueling a trend that was already prevalent. These factors are already the subject of significant debate:

- Will people ultimately accept less data privacy for public health and convenience/lifestyle reasons, or will new safeguards and restrictions need to be imposed by public authorities to reflect their concerns?

Investment and entrepreneurship: In recent years, fueled by low interest rates, creative financial engineering and leveraging have been the keystone to delivering shareholder value; this has been demonstrated by share buybacks, debtand equity-backed acquisitions, industry consolidations and huge valuations for loss-making unicorns with winner-takes-all business models. With massive financial support provided by governments to distressed sectors, citizens may require governments to limit the debt levels and dividend payments of companies supported by their taxpayer dollars. A severe economic downturn may lead to risk aversion in investment decisions, with investments concentrated in sectors labeled strategic by public authorities. On the other hand, investors and governments may also take the opportunity to invest in innovative breakthrough business models and technologies as society adapts to survive:

- To what extent will investors become more risk averse (by choice or regulation), rather than funding breakthroughs and fueling a new wave of entrepreneurial investment?

The combination of these two uncertainty dimensions (the degree of macro/structural and micro/behavioral changes), both of which will be impacted by the length and depth of the crisis, potentially produce very different market environments for businesses. We will explore these in the next section.

The new world – What are the scenarios?

We have illustrated the uncertain world of tomorrow with four scenarios, which represent different combinations of macro and micro shifts. These scenarios all require different strategic responses from businesses.

Scenario #1 – Continued globalization

In Scenario #1, rapid progress in eliminating the virus and a relatively fast economic recovery leads to a return to the key patterns of a globalized economy:

- The economic downturn and limited investment capacity increase the consolidation of economic power into the hands of a small number of giant corporations, including tech leaders such as Amazon, Netflix, Google, Baidu and others. These continue to pursue optimization and efficiency via global supply chains.

- High unemployment rates, low investment capacity and the high cost of debt to the rest of the economy hinders further acceleration of digitalization beyond pre-crisis levels.

- Investment in digital services continues along its previous path, but with a clear and more rigorous focus on short-term return on investment.

- Society’s reluctance to share personal data justifies stringent data-privacy norms, limiting the speed of further economic digitalization.

- Climate-change priorities are still high, but tempered by the need to alleviate short-term economic hardship.

Scenario #1 would not drastically change the key ingredients of the economy and markets, but would mean that private monopolies would act even more as the actor of last resort.

Scenario #2 – Digitalized world

In Scenario #2, a protracted recovery period or failure to find a full solution to the pandemic drives rapid acceleration of digitalization, leading to more permanent changes in the global economy:

- Massive adoption of digital services and other means of securing social distancing, including drastic robotification and remote/flexible working with virtual organizations, become the norm.

- Companies and supply chains are not just connected, but completely digitalized.

- Governments temper protectionist and interventionist policies to enable global free markets to help drive economic recovery, focusing instead on managing the collateral damage from the collapse of distressed legacy sectors.

- Privacy norms are sacrificed to the common interest and private data is made fully available to secure optimal efficiency and fluidity of B2C, B2B and B2G online services such as e-care, e-justice and advisory services.

- The remaining investment capacity of corporations and private-equity firms focuses on new breakthrough technologies and business models, driven by the necessity for radical change.

- Climate-change priorities drive fundamental transformation of the global economy towards sustainable technologies in areas such as energy, mobility and manufacturing.

Scenario #2 effectively continues the trend of the NYSE FANG+ Index, which has outperformed the market this year by up to 12 percent on average, compared to a double-digit drop for the S&P 500. As another example, digital-health funding has already grown by 50 percent in 2020 Q1 year on year, with $3.1B invested. In Scenario #2 the major global digital private players would further accelerate their strong growth.

Scenario #3 – Local and sustainable

In Scenario #3, the combination of a deep recession, high state protectionism, and a public preference for “slower life” causes a reaction against further globalization and drives a focus on developing sustainable local communities:

- Stronger state intervention incentivizes local sourcing and reduces dependency on the global economy.

- Climate change and corporate social responsibility issues are seen as higher priority than economic growth.

- Digitalization progresses, but at a similar rate to precrisis levels, with careful prioritization limited by available investment.

- Organizations and their customers are connected, but they do not become virtual – human contact is still the norm.

- Experiences during lockdown leave a legacy of public preference for localism and stronger awareness of the environmental and personal benefits of less travel, local consumption, less waste and self-sufficiency.

- Lack of investment capacity and economic hardship contribute to a focus on developing the local economy, specializing as required to be competitive for trade and gain access to vital or innovative imports.

- Data-privacy concerns remain strong, with employment as a key priority versus radical technology development.

As an example, some of the principles in Scenario #3 can be found today in Sweden, with its ReGen Villages. As another example, incentivization of local sourcing and reducing reliance on the global economy is already planned by the Bank of Japan.

Scenario #4 – Regional fortresses

In Scenario #4, a protracted recovery period or prolonged failure to find a full solution to the virus drives not only acceleration of digitalization, but also the formation of regional clusters driven by greater state intervention and protectionism as governments look to increase resilience to global shocks:

- Stronger protectionism and state intervention, with the state as the actor of last resort, securing strategic sectors and supporting industries, companies and the economy in fighting threats.

- As in Scenario #2, acceleration of digital and smart technology is a key lever to secure local or regional economic growth, self-sufficiency and local sourcing. Thanks to robotics, regions are able to reshore most of their activity and use digital channels and robots to make cities more efficient and productive.

- “Smartization” of public services is accelerated, including health and infrastructure, as well as robotization of services such as restaurants and stores.

- Privacy norms are sacrificed to the common interest, with private data made fully available to enable digital development.

- Investment, led by cities and regional clusters, focuses on new breakthrough technologies and business models, driven by the necessity for radical change and redeployment.

- Local technology-driven companies are the new champions of a self-sufficient, multi-local world, with the power of global corporations restricted through local regulations.

- Climate-change priorities are pursued through government support to national/regional technology investment and behavior-change efforts.

Although Singapore is not yet as sophisticated as we describe in this scenario, the early response of the city-state to COVID-19, mainly built on strong digital foundations, illustrates some of its features. Singapore has been recognized as very efficient in addressing the surveillance, prevention, diagnosis and treatment stages of the pandemic, as detailed by the United Nations Development Programme (UNDP). The government used contact-tracing technology, with geographic and demographic data shared with the population to encourage people to seek healthcare in case of virus exposure. A range of apps and platforms were used to provide detailed information and stay in touch with the population, while buildings were equipped with diagnostic technologies.

What does this mean for strategy?

As the saying goes, “It is difficult to make predictions, especially about the future”. The range of potential scenarios shows that companies need to embed uncertainty into their strategic decision-making approaches. In working with hundreds of large companies over the last 20 years, we have found that there is a proven methodology for achieving this, which remains effective today.

As shown in Figure 2, the essence of this is to formulate four types of strategic moves, while realizing that in any scenarioplanning exercise, the actual outcome is more likely to be a combination of elements rather than conforming to a single stereotype:

1. Strategic levers – How to shape scenarios and their outcomes in our favor?

First, companies need to leverage the power they possess to influence and shape scenarios in ways that are favorable to them. For example:

- Companies active in the production of medical supplies (such as hydroalcoholic gel) have already engaged with public authorities on the conditions necessary to develop and maintain local/regional production.

- Digital actors are already promoting their solutions (such as e-health platforms, e-education, and individual track & trace) to public authorities and local ecosystems as ways to improve regions’ and cities’ resilience against pandemics. They are also negotiating the frameworks for changes to digital privacy regulation, thereby shaping the future towards a “Regional fortresses” scenario.

- Telecom network operators are positioning themselves as a “critical” sector (enablers of e-education, workfrom- home, robotization, etc.) to secure state subsidies or favorable regulations to accelerate the deployment of fiber-to-the-home and 5G, thereby promoting the “Digitalized world” and “Regional fortresses” scenarios.

2. No-regret moves – How to leverage the certainties?

However, while many uncertainties exist, some things will be fairly certain in all scenarios. For example, today it is almost guaranteed that there will be an increase in workplace virtualization, along with a significant global economic downturn. Any strategy will need to address these issues.

The need for organizations to balance agility and productivity will be critically important to respond rapidly to ongoing changes in a difficult economic climate.

In some cases, distressed competitors or suppliers represent a unique opportunity to acquire strategic competencies (patents, technologies, expertise) that will be key whatever scenario unfolds. Embedding uncertainty management into decision-making processes and governance is compulsory to navigate through the crisis, as well as more fundamentally to thrive in an increasingly volatile world.

3. Strategic options – How to act boldly when opportunities arise?

The aim here is to be ready to make bold moves as trigger points of favorable scenarios are reached. This involves identifying strategic moves with limited upfront investment but massive potential for rapid upscaling. By projecting the company into the most likely scenarios, clear strategic directions can be defined and the company’s future business and operating models shaped. This starts with monitoring promising business models and technologies that are emerging during the crisis, with a view to, for example, taking minority stakes or initially entering partnerships. For example:

- Retail and B2B companies might develop proofs of concept for online personalized AR-/VR-enabled sales and distribution to meet new physical-distancing needs.

- Services companies (e.g., lawyers, notaries, consultants, insurance agents, health professionals) might invest in technical platforms and pilot teams to switch to online provision of (most of) their services, as soon as the first trigger points of the “Digitalized world” or “Regional fortresses” scenarios occur.

- If either the “Local and sustainable” or “Regional fortresses” scenarios begin to unfold, food retailers could prepare their own local-sourcing ecosystems and smart-city suppliers could prepare to double down on their growth investments.

4. Strategic insurance – How to protect against unfavorable scenarios unfolding?

Finally, one of the aspects often poorly addressed in strategic planning is strategic “insurance”. Against an uncertain and unwanted outcome, you insure yourself. Targeted actions can be taken to mitigate the negative impact of unwanted scenarios. For example:

- Companies with globalized production chains could launch robotization pilots to mitigate labor-cost increases due to forced re-localization to higher labor-cost markets.

- Companies could develop plans and establish preliminary contacts/proofs of concept for multisupplier and multi-geographical set-up of their sourcing strategies to pre-empt any losses of competitiveness in case of the “Local and sustainable” or “Regional fortresses” scenarios.

- Businesses could also secure potential access to contracts and/or markets for which public authorities might impose pre-qualification requirements (e.g., localization and security of data storage, minimal production/delivery capacity within the region, backup facilities, formal safety and risk management certifications). Again, the aim is to invest a little upfront to ensure that the company is able to protect itself, rather than deploying costly full-scale back-up plans.

The above approach allows companies to embrace the complexity related to uncertainties, providing clear decision frameworks and linking decision points to events that will trigger the (progressive) unfolding of one or more scenarios. In periods of high uncertainty such as the current crisis, the best-prepared first movers can build substantial competitive advantage, either through minimizing exposure to losses or by capturing the lion’s share of new opportunities.

Insight for the executive

The crisis we are facing is certainly deeper than most of us have seen in our lifetimes. However, despite the hardship and tragedy, there will ultimately be new opportunities, as well as challenges. To prepare for these, leaders need to maintain a broad perspective:

- Look beyond the short-term crisis and start preparing for the new world as structural and behavioral changes begin to significantly reshape the business environment.

- Do not only focus on the most obvious trends, but also assess the major areas of uncertainty and their implications.

- Use the full breadth of strategic plays. Most executives tend to focus on developing strategic options, but they overlook the three other strategic plays: shaping the scenarios, making swift no-regret moves and, especially, developing strategic insurance to mitigate unwanted scenarios.

- Do not try to over-simplify complexity related to uncertainties, but instead embrace it and embed uncertainty management into decision-making:

- Develop capabilities for scenario development and monitoring of trigger events.

- Adjust strategic and operational planning and related governance mechanisms.

- Shape the culture of the organization to help employees deal with uncertainty.

- Strengthen the “ambidextrous” capability of the organization to encourage creativity and responsiveness to change, as well as efficiency and productivity.

- Adapt partner and ecosystem management in terms of both communication around uncertainties and redeployment of capabilities.

- Leverage the potential of digital technologies to improve intelligence and increase agility and responsiveness.

The future is full of complexity and uncertainty. Companies need to embrace this and – underpinned by a clear vision and set of values – be prepared to make radical changes to their products, services and processes as they go forward.

RELATED INFORMATION

Tomorrow’s life sciences

Arthur D. Little and the UITP identify 25 imperatives to enable cities to cope with future mobility challenges

Global consultancy Arthur D. Little, together with its partner the UITP – The International Association of Public Transport – identifies three strategic directions and 25 imperatives for cities to…

Future of Urban Mobility ranking shows most cities are still badly equipped for tomorrow’s mobility challenges and identifies strategic recommendations

The new version of the ‘Future of Urban Mobility’ study includes an update of Arthur D. Little’s Urban Mobility Index, assessing the world’s cities in terms of mobility maturity and performance and…