Introduction

A misplaced consensus?

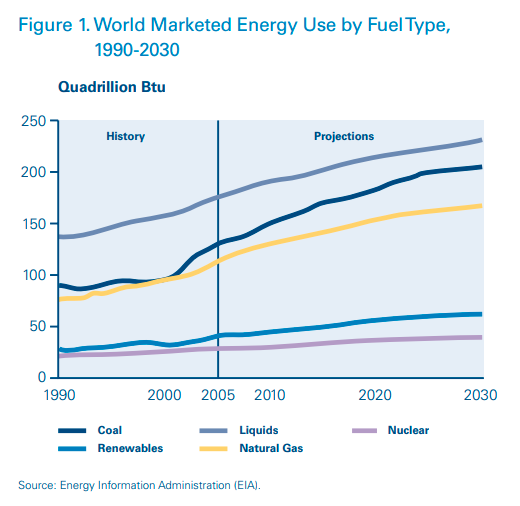

Across the energy industry, there appears to be a strong consensus that the economic crisis of 2008/9 will cause only a short-term slowdown in rising energy consumption and prices; and that after the storm has passed the world will resume its path of increasing energy use, with oil retaining its predominant position in the energy mix, and with prices resuming their inexorable climb to ever-higher levels. This consensus takes support, for example, from the recent International Energy Outlook issued (mid-2008) by the US Department of Energy’s Energy Information Administration, which projects total world consumption of marketed energy will increase by 50% between 2005 and 2030; similar data has been supplied by the Parisbased International Energy Agency (IEA), and other sources.

However, in November 2008 the IEA, in its annual World Energy Outlook, made a significant revision to its forecast of oil consumption. In its Reference Scenario, which amongst other things assumes no change in government policies, forecast oil demand in 2030 was 10 million barrels a day lower than in its previous analysis. Moreover, the IEA’s Executive Director, Nobuo Tanaka, essentially disowned this same Reference Scenario, asserting that: “Current trends in energy supply and consumption are patently unsustainable – environmentally, economically and socially.” To which he could have added “and geopolitically”

While there is no doubt that renewed growth in the world economy, whenever that kicks in, will generate an increasing need for energy, we believe that the consensus about oil’s continuing dominance may be misplaced. We can envisage an alternative future track, where oil loses its share in the energy mix more quickly than the consensus expects.

What is giving substance to this alternative scenario? The convergence of three powerful policy drivers; price volatility, security of supply, and climate change, the implications of which are explored in this paper. The mutually reinforcing impact of these three drivers, and their persuasiveness to those shaping the policy frameworks in all the major consuming markets of the world, including, very importantly, China, could, in our view, act as a catalyst for new policies that set us down the road to quite a different future. In this alternative future, the three converging drivers we have identified all point to the desirability of accelerating the transition to a new, post-hydrocarbons, energy era. And, perhaps counter-intuitively, it may be oil, given its particular demand characteristics, that is most at risk in this context.

Such an alternative scenario has, of course, profound implications for all businesses engaged in the energy industry, be they oil, gas, coal or power companies. This paper outlines those implications.

Unlock a Powerful Difference

RELATED INFORMATION

Arthur D. Little: New report explores "The beginning of the end for oil?"

A new report released today by management consultancy Arthur D. Little questions the energy sector’s consensus view that demand for oil will rise ever higher, driven in particular by consumption in…

Open banking: The beginning of a new era

Due to digital disruption, an important dichotomy erupts: banks have more interaction with customers than ever, but customers have many more choices to fulfill their financial needs. As customers…

Getting ready for the energy consumer of the future

The energy sector is undergoing radical transformation as formerly passive consumers take control over their energy consumption and procurement. Based on the five stages of this transformation, we…