DOWNLOAD

DATE

Contact

Predictive analytics provides the necessary tools to Indian life insurance companies to improve customer retention, optimize business processes and improve profitability.

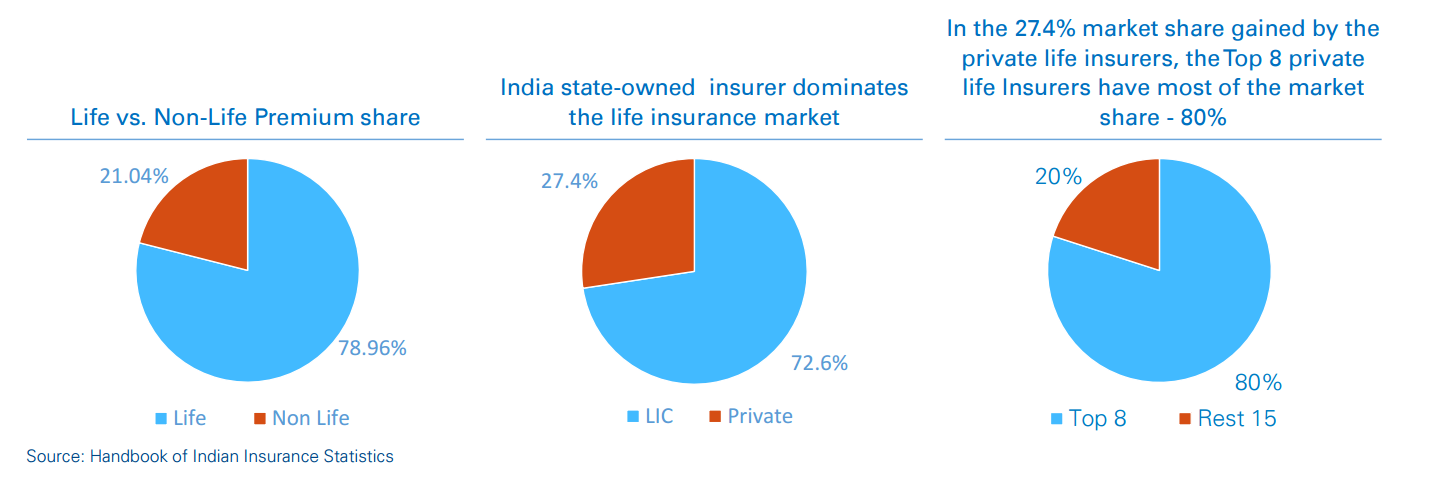

In India, there are 24 life insurance companies. Life Insurance Corporation of India (LIC), a Government of India-owned corporation, has close to 72.6% of all total life premiums and dominates the life insurance market. Out of 23 private life insurers, 15 have less than 1% of the overall life insurance market.

A few of the smaller, private life insurers are trying to find niches markets , cost efficiencies and trying to expand the market. However, most of them have low market share, persistency ratios and high operating expenses. Thus, many smaller life insurers face a survival risk in the Indian life insurance market.

Smaller, private life insurers have a survival risk in the Indian life insurance market. They have low market share, persistency ratios and high operating expenses.

Figure 1 : The key problems plaguing the life insurance companies in India are as follows:

Persistency ratio is defined as the percentage of all existing policies that are renewed by the insurer annually. Policy premiums in India are due monthly, quarterly and yearly. However, due to the factors mentioned earlier, persistency ratios (PR) are low in India.

PR in India is categorized as follows – 13th Month PR (end of 1st year), 25th Month PR (end of 2nd year), 37th Month PR (end of 3rd year), 49th Month PR (end of 4th year) and 61st Month PR (end of 5th year). So, 13th Month PR for the overall industry is 61%, so it means that after 1 year post sale, only 61 out of 100 policies were renewed. Persistency ratio for the overall life insurance industry for the 61st month PR is 28%. This means more than two-thirds of all life insurance policies are not renewed after five years. (See the table below.)

This deeply hurts life insurance companies as they generally struggle to make money in the first five years of the life insurance policy. Customers are also at a disadvantage, as they lose a large proportion of the premiums paid if they don’t renew in the first one to three years.

Life insurers in India are trying to tackle the PR problem by using similar means. The most common approach is to build specialized teams that call policy holders whose policies are up for renewal two to three months before their renewal dates.

The intention is to improve contractibility by systemic calling. However, without an integrated approach (data analysis, analytics, CRM platform, service improvements and process realignment), these efforts are likely to plateau around the industry average, which, in the first case, is not very high.

Unlock a Powerful Difference

RELATED INFORMATION

Arthur D. Little expands Healthcare & Life Sciences Practice in Germany and Switzerland with leading biotech expertise

Dr. Franziska Thomas appointed as Associate Director to lead the way for innovative technology in the pharmaceutical and biotech sectors Global Management Consultancy Arthur D. Little (ADL), today…

Tesla insurance

Tesla Insurance, the automaker’s insurance division, aims to capture a large share of motor insurance among Tesla owners by providing enhanced customer experience compared to traditional motor …

Arthur D. Little appoints Dr. Patrick Linnenbank as Partner in Healthcare & Life Sciences practice

Patrick started his career as a medical doctor, with a focus on Emergency Medicine & Forensics. Following the completion of an MBA, he moved into the consulting industry and in 1999 joined Bain…