DOWNLOAD

DATE

MEET THE AUTHORS

Contact

Retail shops, food & beverage outlets and car parks are perceived as integral parts of an airport. These so-called “non-aero revenues” have long been a reliable and profitable source of income for airports. However, in recent years, airports’ vital income source has been under attack. Now, due to the COVID-19 crisis, airport terminals around the world are deserted. Is COVID-19 the last bullet that will break airports’ fortress? We propose not, if airports embrace current challenges and pivot their mind-set to a data-driven, collaborative approach while differentiating their commercial offerings.

Non-aero revenues are under attack

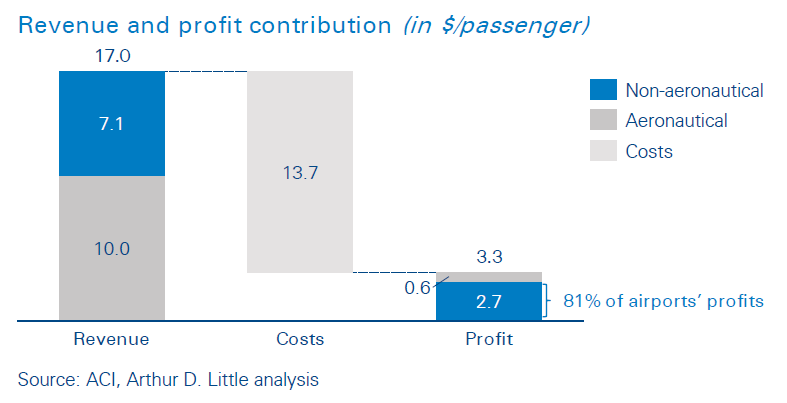

Non-aero revenues are airports’ backbone. With ongoing pressure from airlines on aeronautical fees, non-aero revenues are more and more in focus. On a global scale, costs to serve passengers exceed fees airports receive from airlines. Even though non-aero only makes up 40 percent of airports’ revenues, it accounts for 80 percent of their profits.

Unfortunately for airports, airlines, retailers and new players are all targeting the airports’ bonanza. Global airport retail declined by 3 percent annually between 2013 and 2017. European airports have seen a drop of 7.5 percent in the same time frame. The COVID-19 pandemic has brought the aviation industry to a standstill. Travel will commence again, but long-term effects will remain visible.

Changing preferences and lack of differentiation

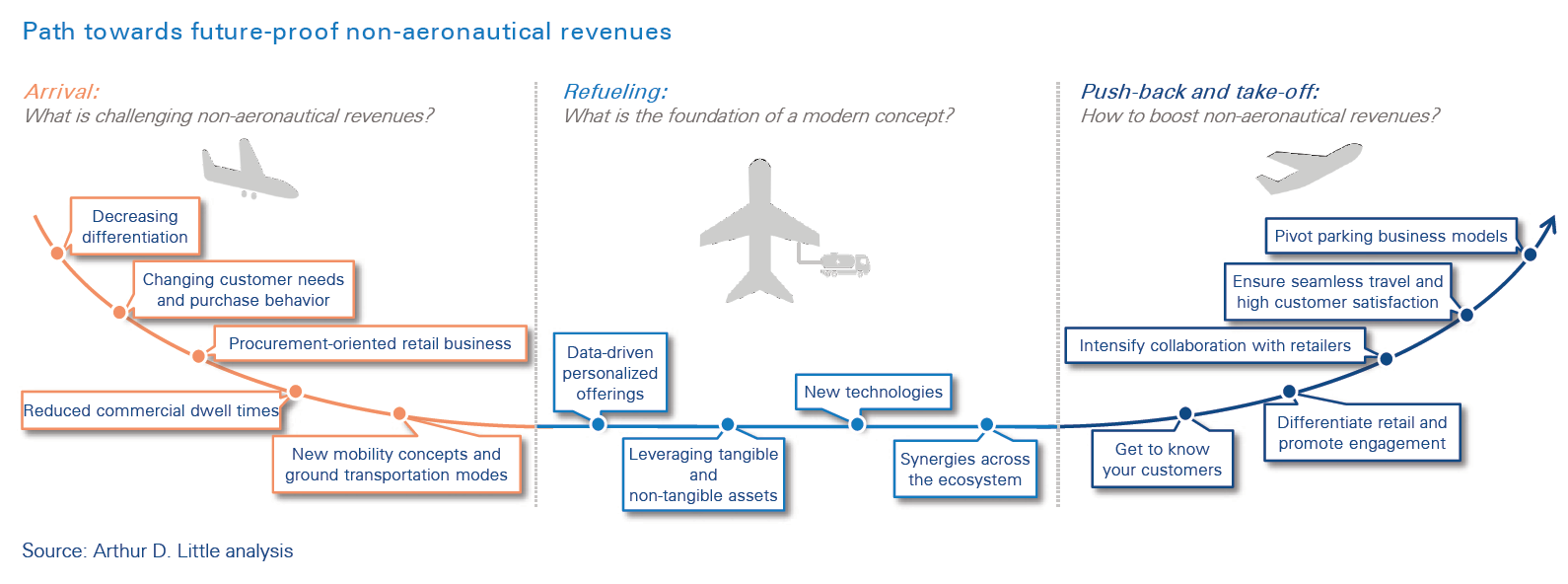

Although all large airports rely on non-aero revenues, large regional differences can be observed. Parking revenues are particularly strong in North America, where cars are still the dominating ground transportation mode. In Asia and the Middle East, retail is the largest segment, driven by strong cultural desires to shop while traveling. In Europe, the picture is more varied and heavily depends on airlines’ business models. Our analysis has revealed five main trends that exemplify the threats to airports’ non-aero business:

1. Decreasing differentiation

The term “duty-free” has long enticed customers to spend at airports. Travelers sweeping through stores and finding unbeatable deals is a rare sight today. The rising numbers of price-conscious travelers, price comparison apps and large e-commerce players have all contributed to the erosion of the perceived price advantage of travel retail. Low prices and exclusive products were once key success drivers. Today, the absence thereof is a key barrier preventing travelers from making retail purchases.

2. Changing customer needs and purchase behavior

Travel retail has historically meant selling luxury products to affluent travelers. Today, passengers expect a radically different shopping experience. They value local products, an extensive selection, the ability to customize and try out products and a seamless digital journey. Convenience and fun are key demands – and most travel retailers have not been able to deliver these. Affluent Asian travelers have slowly replaced less engaged Western luxury consumers in recent years. This has been a positive trend for airport retail, given the significantly larger average basket size of Asian travelers. However, COVID-19 has caused this customer segment to vanish – and it remains to be seen when travelers from Asia will conquer airports in the Western Hemisphere again.

3. Procurement-oriented retail business

Travel retailers are often driven by a strong desire to negotiate low concessions and minimum annual guarantees (MAGs) with airports. In many instances, they lack understanding of customer preferences and the ability to boost sales efficiency. Many industries have mastered the concept of flexible pricing and yield management. Airports, on the other hand, have pushed to increase concessions, leaving retailers with little flexibility to invest in new shopping concepts.

4. Reduced commercial dwell times

Statistics show that spend and commercial dwell time are correlated – spend increases by 2.5 percent for every minute travelers linger longer in retail areas. Passengers’ dwell time has decreased by five minutes. Manual processes that lead to long queues take away valuable shopping time.

5. New mobility concepts and ground transportation modes

Parking fees typically account for around 25 percent of airports’ non-aero revenues. EBIT margins are often as high as 50-70 percent – which makes this the strongest value of all non-aero segments. However, car-sharing and ride-hailing companies such as Uber and Lyft are not a rare sight at airports anymore. Oftentimes, airports have introduced pick-up and drop-off zones for ride-hailing businesses, but otherwise not found answers to the challenges of new ground transportation concepts. In addition, autonomous driving, once it is available, will radically change how people travel to and from airports.

The foundation of a future-proof offering

With a refreshed mind-set, airports can revitalize their non-aero business. A modern offering rests on four pillars:

1. Data-driven personalized offerings

Airports and retailers need to increase their efforts to access data – for example, by developing 5G campus networks – to embrace customers’ preferences and provide a unique and personalized experience along the customer journey. Airside operations benefit, too. For example, location data and improved passenger knowledge help to optimize gate allocation.

2. Leveraging tangible and non-tangible assets

Airports and travel retailers cannot and should not copy large online retailers. Instead, they need to better exploit their key strengths: access to customers with idle time, strong fulfillment capabilities, and the ability to create memorable experiences.

3. New technologies

Airport processes are often labor-intensive and seldom enjoyable. Airports need to use technologies such as biometrics to change this. Retailers need to become more customer oriented. They need to directly target passengers with personalized offers using push notifications.

4. Synergies across the ecosystem

Airlines, airports, retailers and ground handlers all interact with passengers along the travel journey. Despite this, most initiatives to satisfy passengers remain isolated. Intensified collaboration would help deliver a complete and compelling passenger experience.

Five steps to boost non-aero revenues

Our work in this field has shown that airport executives need to take five steps to be ready for the future of non-aero revenues:

1. Get to know your customers

Every point of the customer journey is a monetization opportunity. Yet, players typically only focus on a small section of the customer journey and are missing key ingredients to provide a seamless experience. Unlike airports and retailers, airlines are the main point of contact for passengers and have an incomparable amount of passenger data and customer knowledge. Consequently, ground experiences at many airports do not reflect customers’ preferences. Airports and retailers possess fulfillment capabilities that airlines lack. By collaborating, airlines, airports and retailers can create synergies.

Airlines may not be willing to share valuable passenger data however, leading airports often collect data themselves. For example, Singapore Changi and London Heathrow have introduced loyalty and e-commerce programs.

2. Differentiate and promote engagement

In many ways, e-commerce platforms have made airport retail look outdated. Retailers need to radically shift their focus from procuring contracts to providing great shopping experiences. To fend off attacks from e-commerce, they must innovate and exploit their advantage of physically interacting with passengers.

COVID-19 & non-aero revenues – The way forward

The global COVID-19 pandemic has caused a standstill in the aviation industry. The recovery phase will be difficult. To revitalize their non-aero business, airports need to prepare for the ramp-up phase and embrace four key trends:

1. Increased dwell times

Airports need additional hygiene measures. Passengers will plan for more time at airports – more than needed. We predict that dwell times will increase.

2. Limited capacity

Social distancing will limit the capacity of stores. Airports need to introduce order & collect options to prepare for changing shopping behavior.

3. Uncertain travel behavior

Post-COVID-19 ramp-up scenarios are uncertain. Affluent Asian travelers are cautious about traveling internationally. Changing travel patterns require airports to flexibilize and adapt their non-aero offerings.

4. New collaboration models

Retailers are not able to pay high concessions in turbulent times with uncertain demand. Airports and retailers must align incentives and develop new, resilient and cooperative collaboration models.

Liquor and confectionery will be replaced by showrooms and flagship stores. Retail needs to be entertaining and surprising. “Magic mirrors” and other virtual technologies allow passengers to experience and personalize products. As airlines unbundle and reduce their service offerings, retail opportunities emerge. Snacks and meals sold at vending machines and lounge access can be offered by airport operators instead. In cooperation with grocery stores, airports could even cover daily grocery needs for pick-up at arrival. There are many variables to master from a greater variety of choices, including low-carb and vegan options and modern sitting concepts, to optimized ordering, collection and gate-delivery concepts.

With intriguing offers using localized products that reflect the spirit of the region airports could give passengers the feeling of visiting a special place rather than somewhere boring and monotonous. Even with travel currently low, we believe airports can seize the opportunity of empty terminals and start key redevelopment projects now.

3. Intensify collaboration with retailers

Airports’ retail revenues largely depend on retailers’ sales. In many cases, collaboration between airports and retailers remains superficial as airports impose large concessions on retailers. However, COVID-19 will change how people travel in the future. Asian travelers will be cautious about traveling to epicenters of the pandemic. Retailers at large Western hubs will lose many of their most valuable customers and will be unable to pay high concessions or MAGs to airports.

Instead, airport operators, retailers and even airlines need to jointly develop and market offerings that fulfill passengers’ needs. Airports must provide the physical space, while retailers and brands create unique retail experiences and airlines provide valuable customer data to enable targeted promotions. Collaboration models between landlords and retailers is the foundation. Groupe ADP, a French premier airport operator, has managed to double spending per passenger at Paris Charles de Gaulle airport after establishing retail JVs. By pooling customer knowledge and aligning interests, airports can increase the value of their partnerships, unleash greater benefits for all parties, and make travel retail more sustainable and resilient in turbulent times.

4. Ensure seamless travel and high customer satisfaction

Connecting commercial and operational data is key for a seamless journey. In Helsinki, the introduction of a sensorbased queue management has led to an increase in non-aero revenues by 12.3 percent. In addition, customer satisfaction heavily influences spending. Satisfied customers tend to spend 7-12 percent more money. Hence, delays and cancellations not only cause customer dissatisfaction, but also negatively affect non-aero sales.

5. Pivot parking business models

Parking revenues can no longer be sustained with the classic “pay-to-stay” model. Airports need to anticipate the effects of autonomous driving and ride-hailing and consider these in infrastructure projects.

Airports need to go beyond creating pick-up and drop-off areas. They need to partner with ride-hailing companies and consider toll models to monetize curbside access. More and more airports are introducing ground transportation fees today – often with lower fees for zero-emission vehicles.

In addition, off-site valet and peer-to-peer car-sharing are two promising concepts in their infancy. Even though valet is not a new concept, Amsterdam Schiphol has revitalized it by parking cars at cheaper, off-site locations. Peer-to-peer car-sharing services such as Turo allow passengers to rent out their cars while away – departing passengers earn money with little effort, while arriving passengers enjoy access to affordable cars.

Conclusion

Non-aero revenues, essential for airports to sustain their business, have been under attack. Now, COVID-19 has halted travel almost completely. However, we argue that it merely underlines that change in the non-aero business is overdue. While the recovery from the pandemic demands strong efforts, it is a chance for airports to transform their approach to non-aero revenues.

Unlock a Powerful Difference

RELATED INFORMATION

Traveller 2020 - Change of Mind

Travellers' structure is changing, as are their requirements and buying behaviour. In this abstract, Arthur D. Little analyzes the "change of mind" of the traveller in 2020 compared to today’s…