14 min read • Financial services, Strategy, Operations management

Disruption — Can banks strike back?

“The universal banking model is inherently unstable and unworkable. No amount of restructuring, management change or regulation is ever likely to change that.”

So said John Reed, the former Chairman and CEO of Citigroup, as far back as 2015, at a time when global banks across the world were starting to pare back their international operations in response to increasing regulation. The decline of the traditional global bank has only accelerated since then. The newly emerged digital native and “neobank” competitors are now in favor. Their state-of-the-art digital technology, lower-cost structure, lower capital requirements, and greater flexibility in introducing products render them nimbler and more adaptable to changing consumer demands. Moreover, they are free from the high labor and capital costs of maintaining and upgrading obsolete technology. Because of all this, fintech firms command a much higher stock market price than banks, which is often not much less than that of many major technology firms.

To get a sense of the magnitude of the challenge banks face, we need look no further than Ant, the financial arm of Chinese marketplace Alibaba. Its technology can handle 120,000 transactions every second and reach a decision to grant a loan or not within just three minutes. This is the world’s purest example of digital finance’s tremendous potential, but the vivid signs of a banking revolution are everywhere – for instance, Europe’s three largest “neobanks”, Revolut, N26 and Monzo, have 23 million registered users between them, and that number continues to grow.

By contrast, the model of the traditional universal bank is dead, killed off by a changing marketplace and the emergence of a new breed of footloose financial players that command destructive technological power. Investors’ decisions speak louder than words. Price-to-book ratios for retail banks remain consistently below 1 in all major markets. Venture capital investment in fintech has grown at 20% per year from 2011 to 2021. The number of fintechs companies nearly doubled from around 12,000 in 2018 to almost 21,000 in 2020.

So is it really game over for established banks? Fortunately, not yet. Despite all the funding that has gone their way, there has been no sweeping market takeover by fintechs. Becoming a bank is extremely costly, and there is still a lot of customer stickiness to the brands that they know. Also, fintechs are swimming with a lot of other sharks. For example, the market for payment companies is seriously overcrowded, with many players starved of capital and staring down empty balance sheets. Recent market corrections in fintech valuations (Robinhood being a case in point) and turbulences in the decentralized finance landscape show how fintechs will need to work hard to stay ahead.

There is, therefore, still some time. However, banks are notoriously slow-moving organizations and have a track record of being poor at anticipating change and failing to adapt. Banks do have a future, but they must accept that it’s a different future. If bank leaders fail to make radical changes, they will perish. The time for those changes is now. Let’s consider what they need to do.

Priorities for legacy banks to strike back

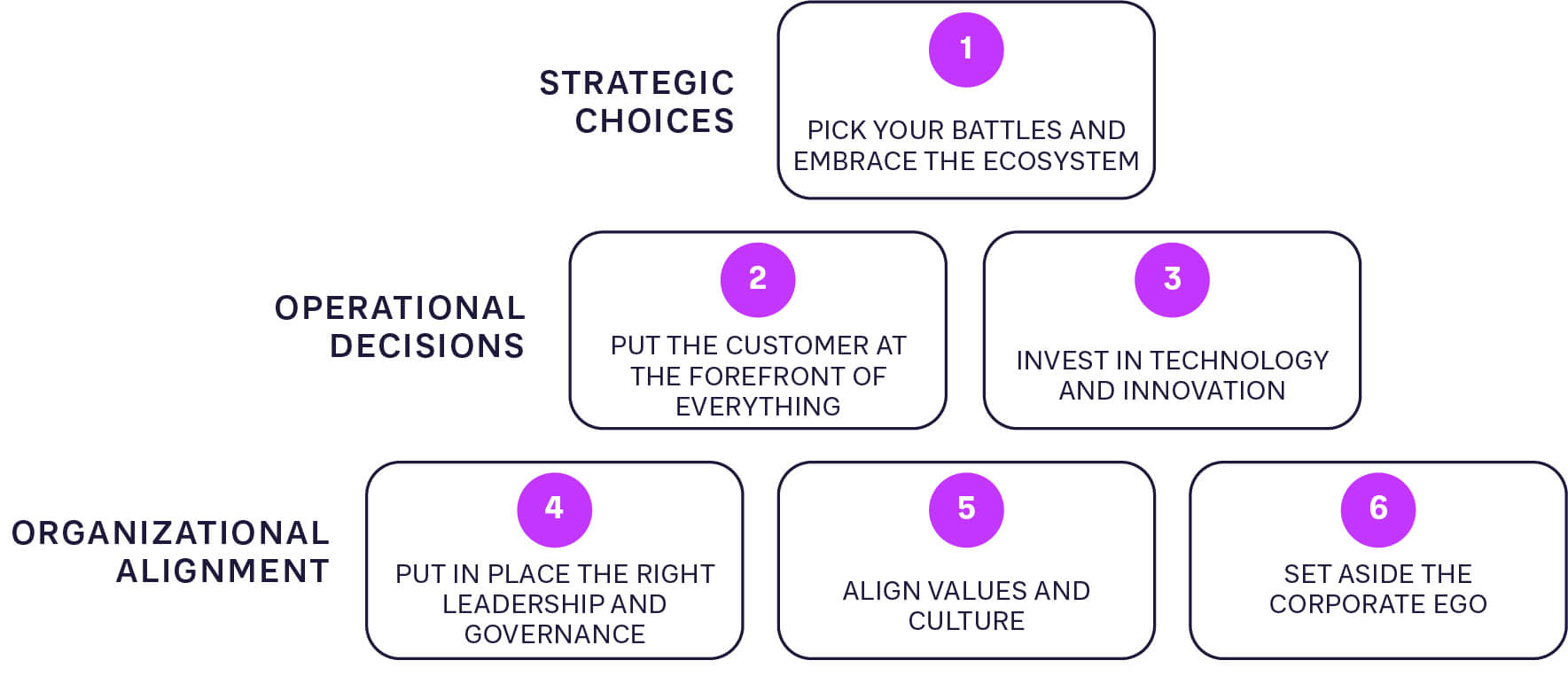

To effect radical change, legacy banks need to consider six priorities to transform themselves into the sort of innovative, agile and forward-looking institutions required for a successful future (Figure 1).

1. Pick your battles and embrace the ecosystem

The place to start is to recognize and acknowledge that things have changed, and it’s no longer possible to be all things to all people. A legacy bank hoping to compete against fintechs and non-banks can no longer afford to dilute its resources by pursuing a “here and there, hedging your bets” strategy. Putting your eggs in different baskets may work for an investor, but not a legacy bank.

This means banks will usually need to move the dial by a factor of 10 rather than just readjust it and work in the margins. The best way to approach this is to make sure they develop a clear picture of the future – the point of arrival of the industry in three to five years’ time – and decide what their role should be within that future. For example, the continuing rise of fintechs brings with it new ways of doing business, such as “triangular strategies” that allow them to leverage assets and channels banks don’t have, and embedded finance, which, given the rise of e-commerce across many markets and channels, offers the opportunity for exponential growth. For instance, in the US, the size of the embedded finance market is forecast to equal that of Big Tech - in other words, approximately half the value of today’s global banking market.

As the traditional value chain is dissolved by these disruptors, it is being replaced by a much wider financial ecosystem consisting of many niches, which is creating a world where, at least for now, capital-intensive models still co-exist alongside those that are capital-light. In this hybrid business environment, the old-school British banking model, which has for so long underpinned financial services, is looking increasingly irrelevant and creaky. If retail banks are to maintain any kind of position in the market, they will need to turn to a balance-sheet-light model that revolves around selling third-party products rather than recycling deposits into new loans. For that, they will need a very different set of capabilities.

What is happening here to banks is, of course, part of a much bigger and wider economic shift in the marketplace. As Anne Bennett, CEO of the National Australian Bank, says: “The largest movie house owns no cinemas, the world’s largest taxi company owns no taxis, and increasingly, large phone companies own no telco infrastructure. What, then, is the future asset for banks?” Her answer: “Experience.”

Of course, the arrival point for every bank is different, but there should be a common factor between all – that this should be far away from where the bank is now. If it is not, the senior leadership team has not been thinking big enough. Without a clear strategy to follow, it is no exaggeration to say a bank could be heading for bankruptcy. And leaders need to be clear that this is much more than digitalization – digital is neither a strategy nor a business model in itself, but, rather, a means to enhance and implement a business model. In practice, banks will need to shed long-established activities, re-evaluate the levels of risk they are willing to accept, restructure systems and processes, and invest without quibble in the new technology that is needed.

2. Put the customer at the forefront of everything

For the future, the customer should be everything. This means any digital transformation must be firmly and fundamentally anchored in the customer value it provides. Traditionally, banks have often focused on demographics and purchase histories to decide on customer priorities, but this will no longer be adequate to move towards the much higher level of customer focus needed in the new environment.

Instead, banks need to employ technology to acquire a much greater understanding of those they do business with, and then use this to personalize every interaction with them. For example, state-of-the-art “chatbots” and other computer-supported conversation tools are now a bare minimum. Data analytics and the use of AI to recognize each customer and then accurately predict the purpose of their conversations is of even more value. Becoming a seamless problem solver, offering “one-call resolution” to save customers time and effort, will go a long way towards winning their hearts and minds. Regaining customers’ trust is essential to make the wheel turn in the traditional banks’ favor.

Given that open banking means disruptive third parties can now access customer data held with another financial institution, banks have no choice but to focus on becoming high-level, data-first organizations themselves, so they can monetize their wealth of customer knowledge. Again, this comes down to investing in the right technology and top-notch analysis. This creates opportunities, but generally only for early movers, as they are the ones that tend to capture the market and hold onto their customers. Life is then harder for those that come afterwards.

3. Invest in technology and innovation

Technology is the key enabler – from increasing productivity and cutting costs to reaching previously inaccessible market segments and enriching the customer experience. Unfortunately, technological obsolescence is rife in today’s banking environment. Those not paying attention to approaching end-of-life hardware and software situations will find themselves in front of a funding abyss as they scramble to replace their old IT infrastructure with something more fit for purpose. The effective adoption and use of next-generation technology is the road to greater customer engagement, faster product development, better operational management, and improved compliance, efficiency, and growth. It will also enrich the customer experience through stellar, hyper-personalized service.

Shifting to new technology will obviously necessitate the writing off of old systems and software, but this is a price that must be accepted. Fortunately, the cost of IT continues to fall and the adoption of cloud-based services can dramatically cut infrastructure costs. Banks must also become technology agnostic by using architectures for front-, middle- and back-office processes that allow for easy integration with third-party solutions and facilitate migration away from legacy IT solutions.

The pace of technological change in the financial sector is rapid, with breakthrough technologies regularly appearing. This means banks need to become proactive in innovation management, continually identifying emerging technologies and then using them to lever advantage. Becoming a truly innovative organization calls for new capabilities and ways of working, including becoming agile in the same way as the best non-bank fintechs. This means creating quickly, running parallel improvement sprints, seeking fast feedback, doubling down on winners, and killing losers. It also means being prepared to embrace working with new ecosystem partners in different ways. For example, some financial institutions have been successful in incubating and scaling up new businesses externally through partners without compromising the wider organization, such as Openbank by Banco Santander. (Refer to ADL’s Breakthrough Incubator model[1] for more on how this works.) A credible innovation strategy ensures that the products and services of tomorrow can be rapidly delivered.

Orange Bank is another example of what is possible. Orange Bank is able to bring out six to eight product innovations in a month, which is double what a legacy institution could deliver in a year, through taking a strategic approach to innovation and adopting modern innovation practices.

4. Put in place the right leadership and governance

Having the right person in charge is key to a legacy bank’s survival and future success. Needed above all is a leader who understands how to be ambidextrous – able to deliver significant growth and productivity improvements in the short term, while simultaneously redesigning a bank’s business model and moving it to the new point of arrival in the future. In most cases this means more emphasis on “Exploring” – innovating for the future – to better balance “Exploiting”, which has typically been the main focus for legacy banks.

This is quite different from being merely “forward-looking”, which involves doing little more than identifying a few industry trends and sketching out some possible options in response. The truly ambidextrous CEO must also be adept at peering through the blizzard of largely irrelevant information, slicing into the complexity of others’ opinions, and be willing to back their decisions even when they are based on incomplete information. Some good examples of banks that have risen to the challenge in this way are BBVA, JP Morgan and Goldman Sachs.

Closely linked to this is the subject of governance. The board appoints the CEO, but do the board members have the right skills, capabilities and foresight to understand the radical nature of the transformation needed? Will they tend to prefer an experienced “status quo CEO” to one who is truly ambidextrous? Therefore, it may be necessary to refresh the board by bringing in a more diverse mix of open-minded individuals representing a range of gender, race and experience profiles. This should include a strong awareness of such things as artificial intelligence, machine learning, robotic process automation and augmented reality.

5. Align values and culture

Bankers often tend to feel uncomfortable when pursuing anything that does not have hard financial edges. However, competing effectively with fintechs and meeting the changing needs of customers mean it is now essential for legacy banks to address issues around organizational personality and culture.

In this, the leader’s perceived values, attitudes and behaviors are key. A forward-looking ambidextrous leader can convince the organization that the old days of banking are gone, and that a different way of thinking is needed. This message needs to be pushed into every corner. Unfortunately, many bank executives do not yet understand the impact of something like digitization and how it impacts every aspect of the business, from core functions to organizational structure and culture.

A good example of this is RBS, which, despite the institution’s massive resources, was incapable of creating a successful digital bank because it was hamstrung by old ways of thinking that were a mismatch with the new model. This can be contrasted with the likes of N26 and Tandem, which achieved great things with very limited resources because they had an aligned mind-set focused on speed and meeting their customers’ needs in the best way possible. In addition, customer needs are changing. For example, just over half of Generation Z (those born between 1995 and 2010) say they trust their primary financial institution – a bank – most with their money.

Today, culture is often cited as the single best predictor of employee satisfaction, more so than compensation or work-life balance. However, the cultural values and day-to-day behaviors of banks are often out of sync with the types of individuals they need to recruit and retain, most significantly in terms of failure to be seen to respect employees adequately. Younger people in particular have different, and often stronger, beliefs and expectations regarding an organization’s values and culture. For example, the need to truly embrace environmental, social, and corporate governance (ESG), which reflects a firm’s collective consciousness beyond the purely commercial, is now a key priority for growing numbers of employees, consumers and investors.

6. Set aside the corporate ego

One of the challenges for all but the largest legacy banks is setting aside their corporate ego and realizing they can no longer go it alone. For those banks to deliver exceptional value to their customers – as they must – they have to be willing to work in partnership with fintechs, which have the digital knowledge and experience they need to access to make up for gaps in their offering.

Banks must be prepared to become part of a much wider ecosystem that is geared towards serving the broader needs of the customer. By doing so, they will be able to turn defense into attack and better protect their position. In such an environment, it isn’t generally possible for a financial brand to stand out as it did before. However, banks can, to some extent, mitigate this loss of visibility by ensuring they play a proactive role in shaping any platform they are part of. This means managing the process of developing the partner ecosystem strategically and purposefully, rather than, as is often the case, in a piecemeal and uncoordinated way.

There are some good examples of this in action. Santander, for instance, has launched “Trade Hub”, a proprietary platform that encompasses non-financial services. For many financial institutions, this coming together with third parties to provide sector-specific solutions will be the only way to secure a long-term future.

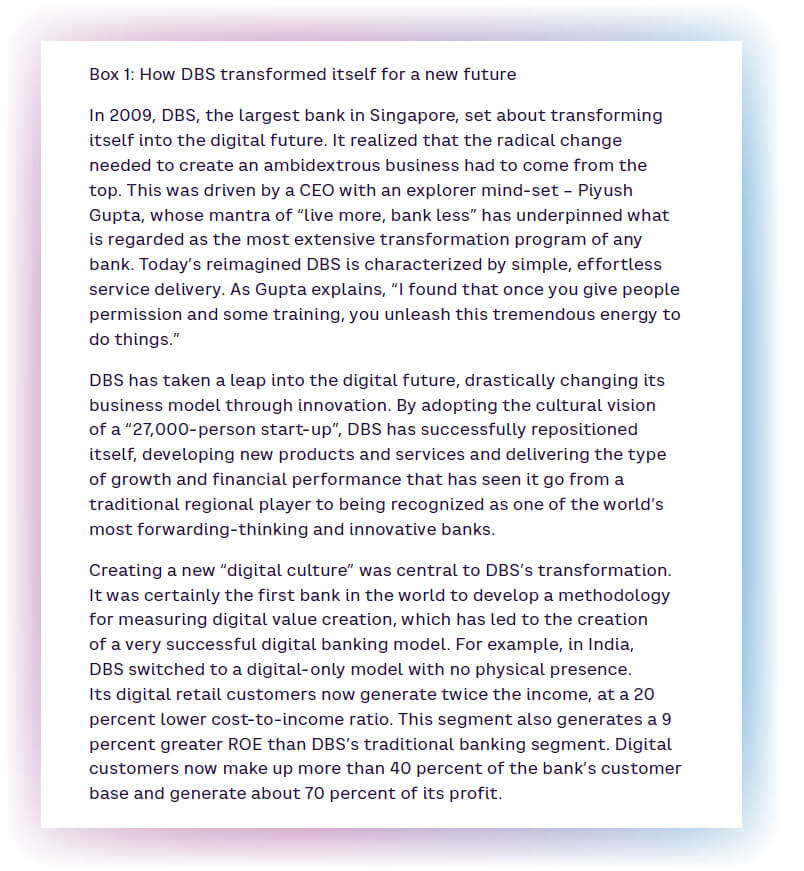

Despite the challenges of transforming a legacy bank, it can certainly be done. DBS, Singapore’s largest bank, is a great example of these six priorities in practice. (See Box 1.)

Insights for the Executive - How to start making the change

How do banks go about making the sort of radical transformation outlined above and become truly ambidextrous? The starting point is to make sure there is a shared sense of urgency and courage to embrace radical, disruptive change across the board and the executive. If you don’t think you need to shift, everything else is irrelevant. As Winston Churchill famously said, “Those that fail to learn from history are doomed to repeat it.”

A useful early step is to perform an honest stock-take of the bank’s current position. An initial “pulse check” can give banks an idea of their current capabilities. They can then follow this up with a benchmark survey to see how those capabilities stack up against those of other banks. After this “ambidexterity audit”, banks will have a much better idea of how to achieve a better balance between explore and exploit.

The most important early priority of all is to make sure that the bank has the right person to lead it to the ambidextrous future. This appointment needs to be an inspirational and entrepreneurial leader who understands the need for transformation and is willing to take risks and think differently – rather than merely maintaining the status quo.

Of course, it is all too easy to oversimplify the situation, and every institution will face differing circumstances and constraints. Deciding the strategy is one thing, but implementation is another entirely.

Nevertheless, timid board members who hide behind the excuse that transformation initiatives will disturb business as usual miss the point. In a brave new world of neobanks and digital fintechs, disrupting business as usual is precisely what needs to be done. If they feel they cannot, or prefer not to, participate in this, they should make room for organizations that are willing to do what is necessary.

As we have said, establishing the bank’s point of arrival in the future is vital. But this doesn’t mean trying to plan every step along the way. We can be fairly sure that Jeff Bezos, when he began Amazon in his garage, had no idea where his company would be in 25 years, or the degree of disruption it would cause. Once banks have reinvented themselves, they need to do it again and again, through a constant cycle of deconstruction and reconfiguration, similar to the Buddhist notion of an endless cycle of rebirth. In the end, the winners will be the banks that can overcome the inertia that legacy institutions have traditionally been incapable of surmounting and transform themselves for good.

Note

[1] “The Breakthrough Incubator: A proven approach | Arthur D. Little (adlittle.com)

14 min read • Financial services, Strategy, Operations management

Disruption — Can banks strike back?

“The universal banking model is inherently unstable and unworkable. No amount of restructuring, management change or regulation is ever likely to change that.”

DATE

So said John Reed, the former Chairman and CEO of Citigroup, as far back as 2015, at a time when global banks across the world were starting to pare back their international operations in response to increasing regulation. The decline of the traditional global bank has only accelerated since then. The newly emerged digital native and “neobank” competitors are now in favor. Their state-of-the-art digital technology, lower-cost structure, lower capital requirements, and greater flexibility in introducing products render them nimbler and more adaptable to changing consumer demands. Moreover, they are free from the high labor and capital costs of maintaining and upgrading obsolete technology. Because of all this, fintech firms command a much higher stock market price than banks, which is often not much less than that of many major technology firms.

To get a sense of the magnitude of the challenge banks face, we need look no further than Ant, the financial arm of Chinese marketplace Alibaba. Its technology can handle 120,000 transactions every second and reach a decision to grant a loan or not within just three minutes. This is the world’s purest example of digital finance’s tremendous potential, but the vivid signs of a banking revolution are everywhere – for instance, Europe’s three largest “neobanks”, Revolut, N26 and Monzo, have 23 million registered users between them, and that number continues to grow.

By contrast, the model of the traditional universal bank is dead, killed off by a changing marketplace and the emergence of a new breed of footloose financial players that command destructive technological power. Investors’ decisions speak louder than words. Price-to-book ratios for retail banks remain consistently below 1 in all major markets. Venture capital investment in fintech has grown at 20% per year from 2011 to 2021. The number of fintechs companies nearly doubled from around 12,000 in 2018 to almost 21,000 in 2020.

So is it really game over for established banks? Fortunately, not yet. Despite all the funding that has gone their way, there has been no sweeping market takeover by fintechs. Becoming a bank is extremely costly, and there is still a lot of customer stickiness to the brands that they know. Also, fintechs are swimming with a lot of other sharks. For example, the market for payment companies is seriously overcrowded, with many players starved of capital and staring down empty balance sheets. Recent market corrections in fintech valuations (Robinhood being a case in point) and turbulences in the decentralized finance landscape show how fintechs will need to work hard to stay ahead.

There is, therefore, still some time. However, banks are notoriously slow-moving organizations and have a track record of being poor at anticipating change and failing to adapt. Banks do have a future, but they must accept that it’s a different future. If bank leaders fail to make radical changes, they will perish. The time for those changes is now. Let’s consider what they need to do.

Priorities for legacy banks to strike back

To effect radical change, legacy banks need to consider six priorities to transform themselves into the sort of innovative, agile and forward-looking institutions required for a successful future (Figure 1).

1. Pick your battles and embrace the ecosystem

The place to start is to recognize and acknowledge that things have changed, and it’s no longer possible to be all things to all people. A legacy bank hoping to compete against fintechs and non-banks can no longer afford to dilute its resources by pursuing a “here and there, hedging your bets” strategy. Putting your eggs in different baskets may work for an investor, but not a legacy bank.

This means banks will usually need to move the dial by a factor of 10 rather than just readjust it and work in the margins. The best way to approach this is to make sure they develop a clear picture of the future – the point of arrival of the industry in three to five years’ time – and decide what their role should be within that future. For example, the continuing rise of fintechs brings with it new ways of doing business, such as “triangular strategies” that allow them to leverage assets and channels banks don’t have, and embedded finance, which, given the rise of e-commerce across many markets and channels, offers the opportunity for exponential growth. For instance, in the US, the size of the embedded finance market is forecast to equal that of Big Tech - in other words, approximately half the value of today’s global banking market.

As the traditional value chain is dissolved by these disruptors, it is being replaced by a much wider financial ecosystem consisting of many niches, which is creating a world where, at least for now, capital-intensive models still co-exist alongside those that are capital-light. In this hybrid business environment, the old-school British banking model, which has for so long underpinned financial services, is looking increasingly irrelevant and creaky. If retail banks are to maintain any kind of position in the market, they will need to turn to a balance-sheet-light model that revolves around selling third-party products rather than recycling deposits into new loans. For that, they will need a very different set of capabilities.

What is happening here to banks is, of course, part of a much bigger and wider economic shift in the marketplace. As Anne Bennett, CEO of the National Australian Bank, says: “The largest movie house owns no cinemas, the world’s largest taxi company owns no taxis, and increasingly, large phone companies own no telco infrastructure. What, then, is the future asset for banks?” Her answer: “Experience.”

Of course, the arrival point for every bank is different, but there should be a common factor between all – that this should be far away from where the bank is now. If it is not, the senior leadership team has not been thinking big enough. Without a clear strategy to follow, it is no exaggeration to say a bank could be heading for bankruptcy. And leaders need to be clear that this is much more than digitalization – digital is neither a strategy nor a business model in itself, but, rather, a means to enhance and implement a business model. In practice, banks will need to shed long-established activities, re-evaluate the levels of risk they are willing to accept, restructure systems and processes, and invest without quibble in the new technology that is needed.

2. Put the customer at the forefront of everything

For the future, the customer should be everything. This means any digital transformation must be firmly and fundamentally anchored in the customer value it provides. Traditionally, banks have often focused on demographics and purchase histories to decide on customer priorities, but this will no longer be adequate to move towards the much higher level of customer focus needed in the new environment.

Instead, banks need to employ technology to acquire a much greater understanding of those they do business with, and then use this to personalize every interaction with them. For example, state-of-the-art “chatbots” and other computer-supported conversation tools are now a bare minimum. Data analytics and the use of AI to recognize each customer and then accurately predict the purpose of their conversations is of even more value. Becoming a seamless problem solver, offering “one-call resolution” to save customers time and effort, will go a long way towards winning their hearts and minds. Regaining customers’ trust is essential to make the wheel turn in the traditional banks’ favor.

Given that open banking means disruptive third parties can now access customer data held with another financial institution, banks have no choice but to focus on becoming high-level, data-first organizations themselves, so they can monetize their wealth of customer knowledge. Again, this comes down to investing in the right technology and top-notch analysis. This creates opportunities, but generally only for early movers, as they are the ones that tend to capture the market and hold onto their customers. Life is then harder for those that come afterwards.

3. Invest in technology and innovation

Technology is the key enabler – from increasing productivity and cutting costs to reaching previously inaccessible market segments and enriching the customer experience. Unfortunately, technological obsolescence is rife in today’s banking environment. Those not paying attention to approaching end-of-life hardware and software situations will find themselves in front of a funding abyss as they scramble to replace their old IT infrastructure with something more fit for purpose. The effective adoption and use of next-generation technology is the road to greater customer engagement, faster product development, better operational management, and improved compliance, efficiency, and growth. It will also enrich the customer experience through stellar, hyper-personalized service.

Shifting to new technology will obviously necessitate the writing off of old systems and software, but this is a price that must be accepted. Fortunately, the cost of IT continues to fall and the adoption of cloud-based services can dramatically cut infrastructure costs. Banks must also become technology agnostic by using architectures for front-, middle- and back-office processes that allow for easy integration with third-party solutions and facilitate migration away from legacy IT solutions.

The pace of technological change in the financial sector is rapid, with breakthrough technologies regularly appearing. This means banks need to become proactive in innovation management, continually identifying emerging technologies and then using them to lever advantage. Becoming a truly innovative organization calls for new capabilities and ways of working, including becoming agile in the same way as the best non-bank fintechs. This means creating quickly, running parallel improvement sprints, seeking fast feedback, doubling down on winners, and killing losers. It also means being prepared to embrace working with new ecosystem partners in different ways. For example, some financial institutions have been successful in incubating and scaling up new businesses externally through partners without compromising the wider organization, such as Openbank by Banco Santander. (Refer to ADL’s Breakthrough Incubator model[1] for more on how this works.) A credible innovation strategy ensures that the products and services of tomorrow can be rapidly delivered.

Orange Bank is another example of what is possible. Orange Bank is able to bring out six to eight product innovations in a month, which is double what a legacy institution could deliver in a year, through taking a strategic approach to innovation and adopting modern innovation practices.

4. Put in place the right leadership and governance

Having the right person in charge is key to a legacy bank’s survival and future success. Needed above all is a leader who understands how to be ambidextrous – able to deliver significant growth and productivity improvements in the short term, while simultaneously redesigning a bank’s business model and moving it to the new point of arrival in the future. In most cases this means more emphasis on “Exploring” – innovating for the future – to better balance “Exploiting”, which has typically been the main focus for legacy banks.

This is quite different from being merely “forward-looking”, which involves doing little more than identifying a few industry trends and sketching out some possible options in response. The truly ambidextrous CEO must also be adept at peering through the blizzard of largely irrelevant information, slicing into the complexity of others’ opinions, and be willing to back their decisions even when they are based on incomplete information. Some good examples of banks that have risen to the challenge in this way are BBVA, JP Morgan and Goldman Sachs.

Closely linked to this is the subject of governance. The board appoints the CEO, but do the board members have the right skills, capabilities and foresight to understand the radical nature of the transformation needed? Will they tend to prefer an experienced “status quo CEO” to one who is truly ambidextrous? Therefore, it may be necessary to refresh the board by bringing in a more diverse mix of open-minded individuals representing a range of gender, race and experience profiles. This should include a strong awareness of such things as artificial intelligence, machine learning, robotic process automation and augmented reality.

5. Align values and culture

Bankers often tend to feel uncomfortable when pursuing anything that does not have hard financial edges. However, competing effectively with fintechs and meeting the changing needs of customers mean it is now essential for legacy banks to address issues around organizational personality and culture.

In this, the leader’s perceived values, attitudes and behaviors are key. A forward-looking ambidextrous leader can convince the organization that the old days of banking are gone, and that a different way of thinking is needed. This message needs to be pushed into every corner. Unfortunately, many bank executives do not yet understand the impact of something like digitization and how it impacts every aspect of the business, from core functions to organizational structure and culture.

A good example of this is RBS, which, despite the institution’s massive resources, was incapable of creating a successful digital bank because it was hamstrung by old ways of thinking that were a mismatch with the new model. This can be contrasted with the likes of N26 and Tandem, which achieved great things with very limited resources because they had an aligned mind-set focused on speed and meeting their customers’ needs in the best way possible. In addition, customer needs are changing. For example, just over half of Generation Z (those born between 1995 and 2010) say they trust their primary financial institution – a bank – most with their money.

Today, culture is often cited as the single best predictor of employee satisfaction, more so than compensation or work-life balance. However, the cultural values and day-to-day behaviors of banks are often out of sync with the types of individuals they need to recruit and retain, most significantly in terms of failure to be seen to respect employees adequately. Younger people in particular have different, and often stronger, beliefs and expectations regarding an organization’s values and culture. For example, the need to truly embrace environmental, social, and corporate governance (ESG), which reflects a firm’s collective consciousness beyond the purely commercial, is now a key priority for growing numbers of employees, consumers and investors.

6. Set aside the corporate ego

One of the challenges for all but the largest legacy banks is setting aside their corporate ego and realizing they can no longer go it alone. For those banks to deliver exceptional value to their customers – as they must – they have to be willing to work in partnership with fintechs, which have the digital knowledge and experience they need to access to make up for gaps in their offering.

Banks must be prepared to become part of a much wider ecosystem that is geared towards serving the broader needs of the customer. By doing so, they will be able to turn defense into attack and better protect their position. In such an environment, it isn’t generally possible for a financial brand to stand out as it did before. However, banks can, to some extent, mitigate this loss of visibility by ensuring they play a proactive role in shaping any platform they are part of. This means managing the process of developing the partner ecosystem strategically and purposefully, rather than, as is often the case, in a piecemeal and uncoordinated way.

There are some good examples of this in action. Santander, for instance, has launched “Trade Hub”, a proprietary platform that encompasses non-financial services. For many financial institutions, this coming together with third parties to provide sector-specific solutions will be the only way to secure a long-term future.

Despite the challenges of transforming a legacy bank, it can certainly be done. DBS, Singapore’s largest bank, is a great example of these six priorities in practice. (See Box 1.)

Insights for the Executive - How to start making the change

How do banks go about making the sort of radical transformation outlined above and become truly ambidextrous? The starting point is to make sure there is a shared sense of urgency and courage to embrace radical, disruptive change across the board and the executive. If you don’t think you need to shift, everything else is irrelevant. As Winston Churchill famously said, “Those that fail to learn from history are doomed to repeat it.”

A useful early step is to perform an honest stock-take of the bank’s current position. An initial “pulse check” can give banks an idea of their current capabilities. They can then follow this up with a benchmark survey to see how those capabilities stack up against those of other banks. After this “ambidexterity audit”, banks will have a much better idea of how to achieve a better balance between explore and exploit.

The most important early priority of all is to make sure that the bank has the right person to lead it to the ambidextrous future. This appointment needs to be an inspirational and entrepreneurial leader who understands the need for transformation and is willing to take risks and think differently – rather than merely maintaining the status quo.

Of course, it is all too easy to oversimplify the situation, and every institution will face differing circumstances and constraints. Deciding the strategy is one thing, but implementation is another entirely.

Nevertheless, timid board members who hide behind the excuse that transformation initiatives will disturb business as usual miss the point. In a brave new world of neobanks and digital fintechs, disrupting business as usual is precisely what needs to be done. If they feel they cannot, or prefer not to, participate in this, they should make room for organizations that are willing to do what is necessary.

As we have said, establishing the bank’s point of arrival in the future is vital. But this doesn’t mean trying to plan every step along the way. We can be fairly sure that Jeff Bezos, when he began Amazon in his garage, had no idea where his company would be in 25 years, or the degree of disruption it would cause. Once banks have reinvented themselves, they need to do it again and again, through a constant cycle of deconstruction and reconfiguration, similar to the Buddhist notion of an endless cycle of rebirth. In the end, the winners will be the banks that can overcome the inertia that legacy institutions have traditionally been incapable of surmounting and transform themselves for good.

Note

[1] “The Breakthrough Incubator: A proven approach | Arthur D. Little (adlittle.com)

RELATED INFORMATION

Driving Banks' Value Through M&A

The crisis in the financial markets is providing additional momentum for already increased M&A activity, with a number of sizeable institutions suddenly up for sale. How can banks manage post-…

Money's not all banks buy

Purchasing, as a rule, is not part of a bank or insurance company’s core business. As a result, financial services organisations often underestimate both the risks associated with purchasing and the…

@Banks: Stay Tuned With Your Customers

Two main ways could be undertaken: differentiate and renew value proposition with innovative services and products and make customers and their needs the focal point of the business model.Banks can…