DOWNLOAD

DATE

MEET THE AUTHORS

Contact

The construction and building sector is an important piece of the decarbonization puzzle as it significantly contributes to global greenhouse gas (GHG) emissions. Pressed by increasingly demanding stakeholders, real estate companies are adopting ambitious midterm decarbonization targets. In designing such strategies, these companies should adopt a holistic approach, leading to a decrease of GHG emissions while defending their bottom lines and maintaining or even improving the quality of the service they provide to their customers. Arthur D. Little (ADL) has developed a client-focused decarbonization strategy that balances these strategic objectives with additional limiting conditions.

WHY REAL ESTATE COMPANIES PLEDGE TO BECOME GREENER

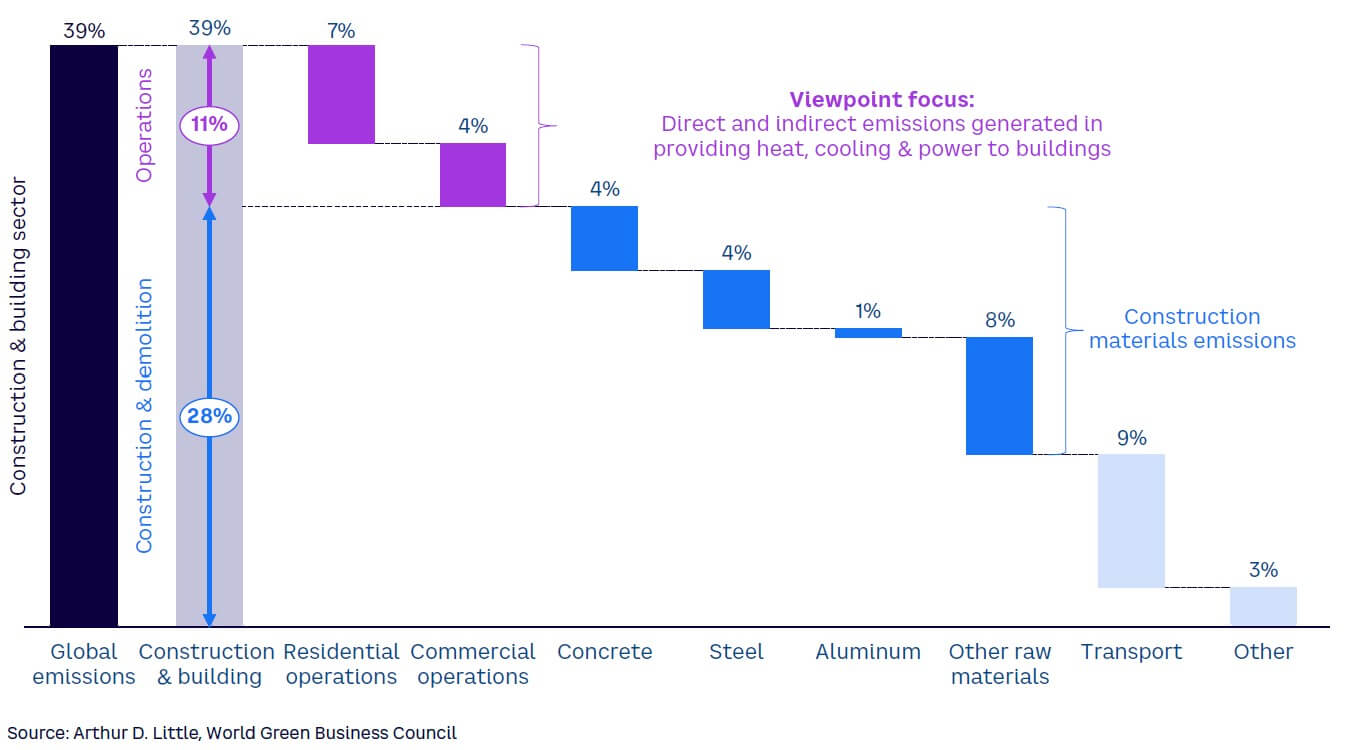

Accounting for the entire value chain — from downstream through own operations to upstream (scopes 1, 2, and 3) — the World Green Buildings Council reported that the construction and building sector accounted for 39% of global GHG emissions in 2019, just before the COVID-19 pandemic disrupted the industry (see Figure 1). The largest portion was generated during construction and demolition, primarily driven by construction materials that alone accounted for 17% of global GHG emissions. This Viewpoint focuses on the remaining portion of direct and indirect GHG emissions generated during building operations (in providing heat, cooling, and power). The emissions generated amounted to 11% of the global GHG emissions in 2019, with residential and commercial operations accounting for 7% and 4%, respectively.

Real estate companies are feeling the mounting pressure toward decarbonization from all key stakeholders as the industry rebounds from the effects of the pandemic. Decarbonization regulation is both broadening and deepening with regards to compulsory environmental, social, and governance (ESG) reporting, regulation of sustainable finance, and subsidy schemes. With the support of rating agencies, financial institutions are being obliged to look into carbon footprint when offering financing terms. A growing number of sustainability-conscious customers and employees are making further involvement with real estate companies conditional upon them acting sustainably.

Real estate companies worldwide are responding to the pressure by adopting GHG reduction targets and undertaking initiatives toward their fulfillment (see Figure 2). Major residential and commercial real estate companies alike have taken midterm commitments to double-digit carbon footprint reductions, with a few companies pledging carbon neutrality. Given the large quantity and diversity of real estate assets under management, achieving these targets will be no easy feat. Gaining credibility in the eyes of key stakeholders will require cross-country and cross-asset coordination of green initiatives under a single unifying, company-wide decarbonization strategy.

WHAT IT TAKES TO BE GREENER

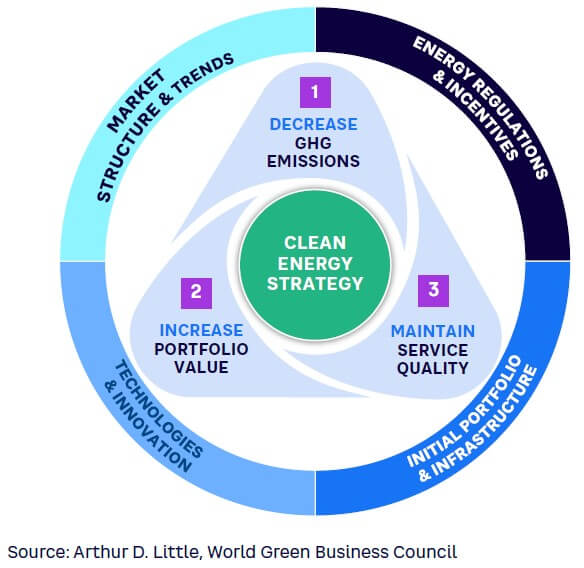

A sizeable and heterogeneous asset base spanning multiple countries is not the only source of complexity when it comes to a clean energy strategy. Although carbon footprint reduction is at the heart of such efforts, a holistic approach requires companies to consider additional objectives (see Figure 3). Chief among these is to increase the value of the underlying real estate portfolio. At the same time, customers should be shielded from any adverse effects brought about by the implementation of the decarbonization strategy, receiving the same level or even an increase in quality of service.

To be credible, a clean energy strategy must be implementable, taking note of all relevant limiting conditions with regards to the real estate company as well as external factors. Given the heavily regulated character of the energy industry, legal compliance is a key factor shaping any to-be strategy. Portfolios of real estate companies are rarely homogeneous, with assets differing widely in terms of technical condition, equipment, age, or lease structure. Clean energy strategies must take these portfolio and infrastructure characteristics into consideration.

Moreover, decarbonization has become the focal point of R&D only recently, meaning that clean energy strategies must also take stock of cutting-edge technologies and anticipate likely future developments. Recent geopolitical events remind us that in our heavily interconnected world, questions related to broader market context, such as self-sufficiency in primary fuels, cannot be omitted. Finally, offers by real estate companies do not simply exist in a vacuum but rather are pitted against each other in a densely populated competition space.

HOW TO BUILD A CLEAN ENERGY STRATEGY

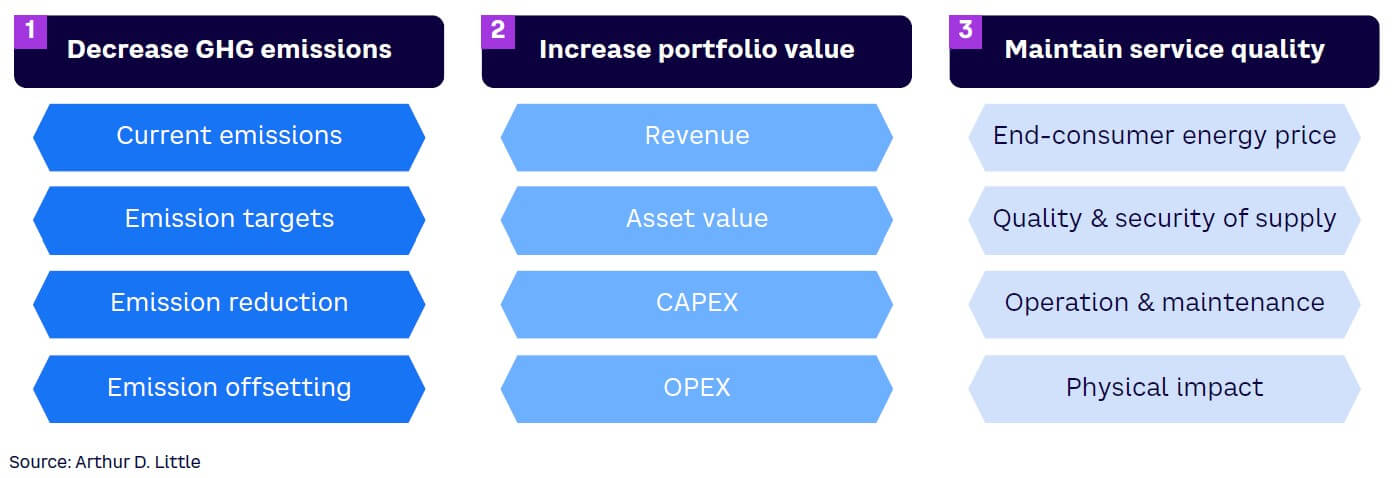

Given the multivariate nature of the exercise, a holistic clean energy strategy should be built using a bottom-up approach. Consequently, each strategic objective should be further broken down into key considerations to fulfill all three strategic objectives — decrease GHG emissions, increase portfolio value, and maintain service quality — while not omitting any relevant factors and ensuring feasibility of subsequent clean energy strategy implementation (see Figure 4).

Real estate companies can translate the high-level strategic objectives into specific measures by deeper analysis of these key considerations. Although the GHG-decreasing impacts of energy-efficiency improvements, heating and power technology upgrades, or carbon-offset purchases are apparent, in-depth analysis is required to determine the extent of implementation. At the same time, a deeper assessment of key considerations may uncover hidden opportunities or threats (such as in the case example shown in Figure 5). Analyzing potential revenue streams can reveal an opportunity to enter into the clean energy market as a utility provider.

Establishing credibility and comparability remains the core issue connected with carbon accounting until regulatory bodies adopt a transparent, unified, and binding set of rules. To state one such example, the EU is expected to adopt corporate sustainability reporting standards next year (the proposal for the directive is being discussed within the Council or its preparatory bodies). Until then, GHG inventory in Europe should be established in accordance with one of the two widely employed and mutually complementary EU industry standards (e.g., GHG Protocol or ISO 14064-1).

GHG emission-reduction targets should always include both direct and indirect emissions. Accounting for scopes 1, 2, and 3 avoids potential carbon-dumping concerns. Unlike other industries, total emissions generated by the company and its tenants during real estate operations can be accounted for relatively easily. As emissions primarily relate to energy consumption, the estimation of total emissions hinges on the calculation of emission factors and energy consumption. To further increase transparency, a clean energy strategy should support total emission-reduction targets with a set of prioritized, more concrete secondary targets. For example, a company could commit to eliminating certain fuels, such as coal, before a specific date.

Carbon footprint can be reduced either via emission reduction or offsetting. Emission reduction covers all the methods by which a company eliminates some of its scopes 1, 2, and 3 GHG emissions. These methods can be active, such as replacing or upgrading heating technology, or passive, such as improving building insulation. Emission offsetting refers to all the methods by which a company eliminates some GHG emissions falling outside scopes 1, 2, and 3.

In the current world of lackluster carbon-accounting rules, the stated impact of emission-offsetting schemes is often overestimated, adding to the problem of greenwashing. Moreover, due to lack of a direct link between the offset and company activities, carbon offsets are often seen as “carbon indulgences.” For these reasons, a company should employ offsets to eliminate the emissions that remain after applying all reasonable reductions. Only offsets in line with well-recognized standards such as the Gold Standard (considered the most rigorous climate standard by many NGOs) should be opted for.

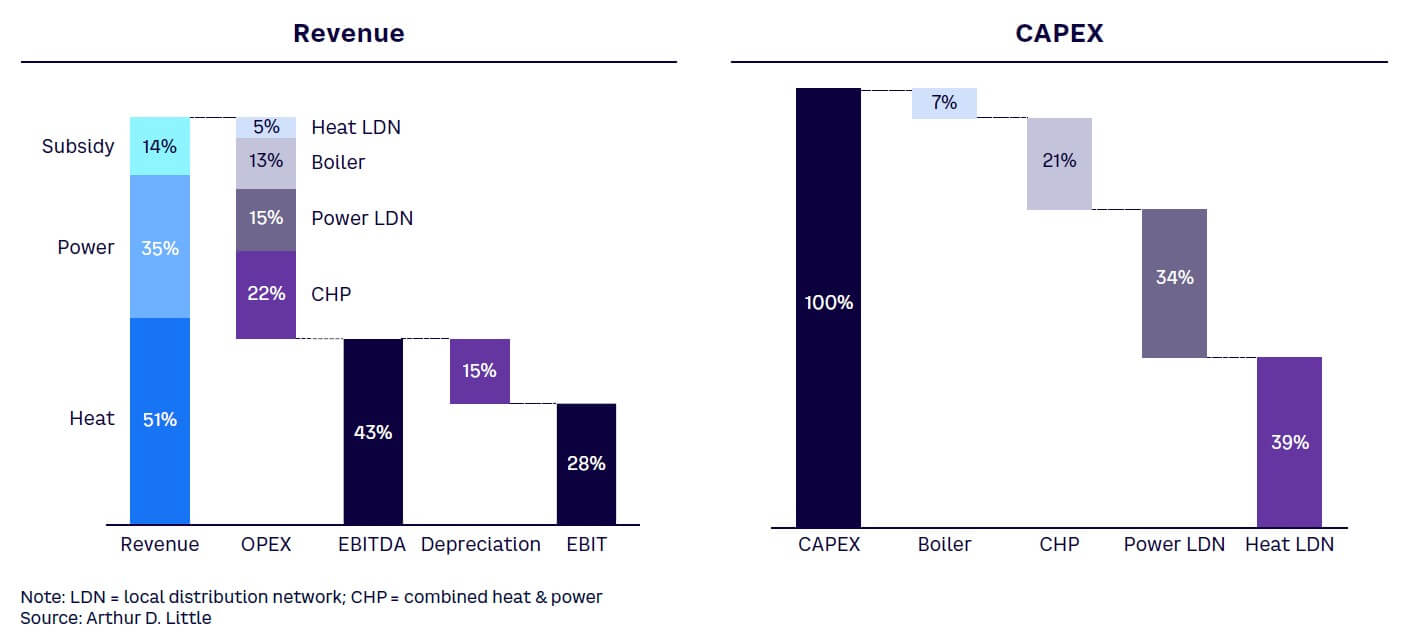

The strategic goal of increasing a real estate company’s portfolio value can be approached either by raising the yearly financial net inflows or the value of the overall asset base. (Figure 6 illustrates a case example of revenue and CAPEX breakdown.) Increasingly popular decentralized energy solutions and, specifically, local distribution networks, present an opportunity for real estate companies to enter into the utility business. They allow companies to replace the often inefficient centralized generation sources and cut out the middleman via a transmission network operator. The resulting price competitiveness of such technology solutions allows real estate companies to create a profitable additional revenue stream.

In terms of asset value, it is important to consider the increase in present value due to carbon-reduction initiatives. At the same time, bear in mind that the assets with the biggest carbon footprint will potentially erode the value in the future, when now-external carbon costs are internalized. If carbon-reduction measures prove to have negative present value, the company should consider redeveloping or even selling the asset.

Calculating OPEX, as the name suggests, requires the basic concept of a to-be operational model. At the very least, the company must decide whether to act as a utility provider and, if it does so, it must decide on the length of the value chain captured and the level of insourcing for different activities. CAPEX estimation then requires the basic concept of the implementation plan, since the implementation can often stretch to multiple years given regional installation workforce and budget limitations. Emission-reducing initiatives must be planned sequentially and in a sensible manner. For example, it is better to first insulate and then upgrade the heating system, and both initiatives are best done in quick succession to minimize the impact of the work on the tenants.

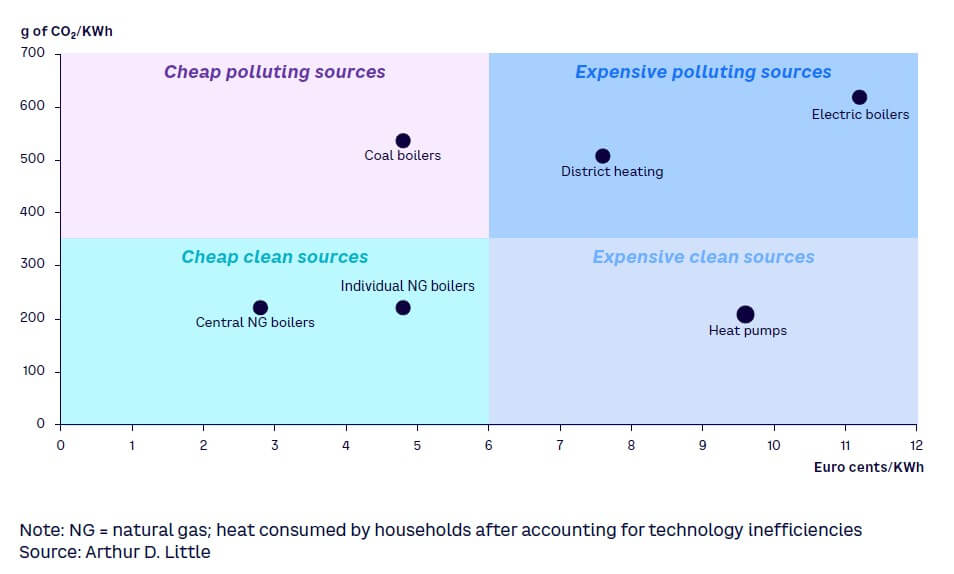

On top of the emission-reduction potential, energy system upgrades should be assessed by their financial impact on the end consumer, which is easily quantifiable by the figure on their utility bill (for an example of joint reduction potential and end-consumer price prioritization, see Figure 7). Utility prices must be kept in check to maintain the service quality at the same level. In this regard, being a utility provider covering as large a portion of the local generation-distribution-retail value chain as possible makes good sense. Becoming locally vertically integrated increases the size of the margin and puts the real estate companies in charge of the decision with regard to its redistribution between the shareholders and the tenants.

Emission-reducing energy system upgrades also must carefully weigh the fuel and technology to be employed. Recent geopolitical developments serve as a stark reminder that among other considerations, the choice of primary fuel determines the security of supply. The end consumer relying on natural gas as a heating fuel source can only hope that after more than a decade of stability and after the current unpredictably turbulent period, prices will once again settle at a level not too much higher than before. The choice of technology type and manufacturer can also have a significant impact on the extent and regularity of maintenance work.

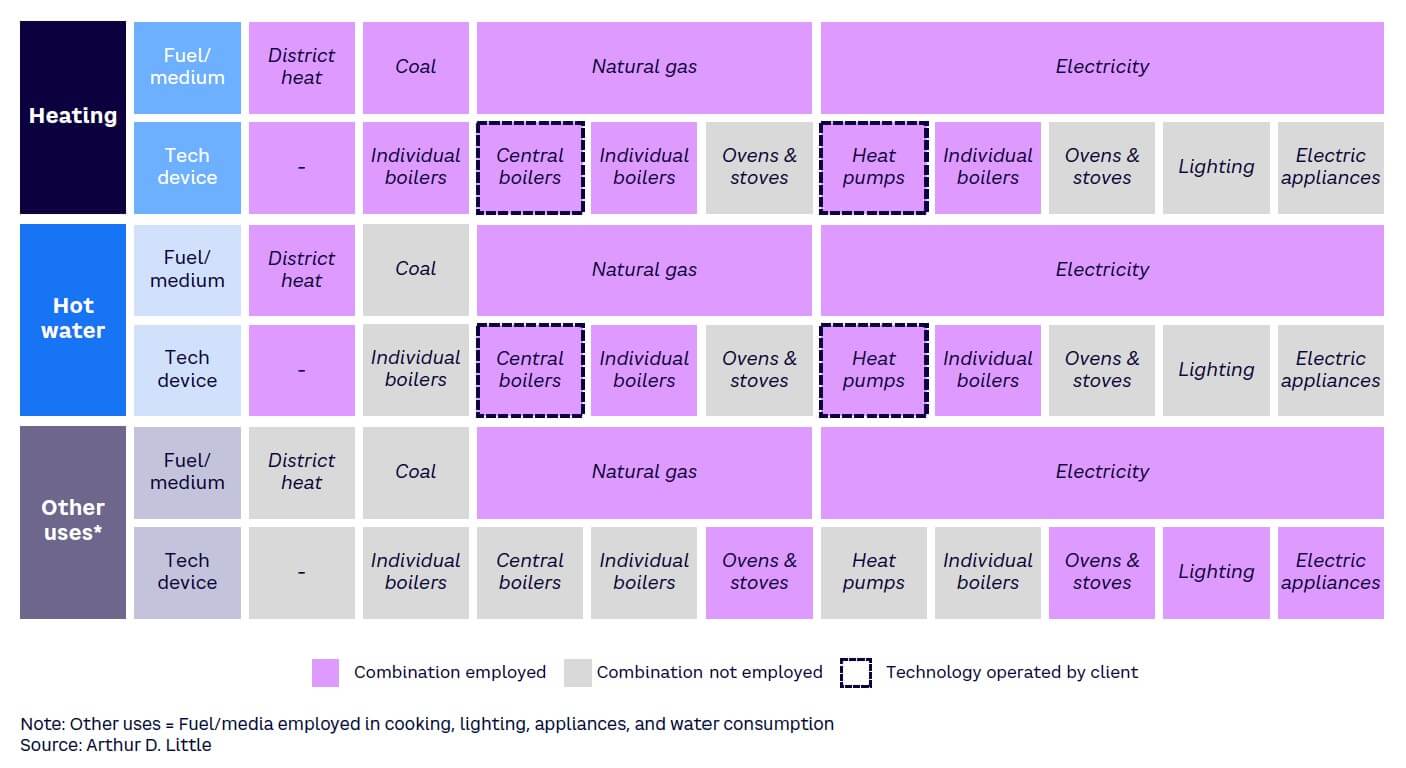

It is important to remember that the blueprint of the carbon-reduction initiatives should aim to marry the world of physical objects. Heat pumps with above 100% efficiency statistics look great on paper until a particularly noisy model keeps tenants awake at night. The operation and maintenance of bulky combined heat and power units require dedicated premises with sufficient floorspace. Restraint also must be applied in the calculations of photovoltaic potential, as the rooftop orientation, gradient, and presence of skylights or rooftop windows may all hinder implementation.

Conclusion

SOLVING DECARBONIZATION PUZZLE IN REAL ESTATE

As we have demonstrated, a holistic approach to a decarbonization strategy boils down to a complex multivariate optimization with a large number of specific limiting conditions and considerations. In developing clean energy strategy, real estate companies should:

- Employ recognized carbon-accounting standards covering scopes 1, 2, and 3 GHG emissions and set primary GHG-reduction targets supported by specific secondary targets.

- Prioritize emission-reduction initiatives and employ carbon offsets aligned with recognized standards to eliminate residual carbon footprint.

- Assess the profitability of decentralized energy solutions market entry and net present value of upgrading, redeveloping, or selling off the assets with the highest carbon footprint.

- Ensure that any financial or nonfinancial potential negative impact on tenants is minimized.

Unlock a Powerful Difference

RELATED INFORMATION

MTC Kuwait bids US$ 6.1 billion for Saudi Arabia’s third mobile license

Mobile Telecommunications Company, the mobile phone operator in Kuwait, has bid 22.9 billion riyals ($6.1 billion) for Saudi Arabia's third mobile license. On March 17th, the board of directors of…

A Conversation Profits with Principles – The Transformation of Royal Dutch/Shell

With more than 100,000 employees and assets valued at $80 billion, the Royal Dutch/Shell Group is a global giant in the energy industry, involved in the whole production process of fossil fuels – –…

Viewpoint Maastricht Doesn't Matter – European Business Strategies Do

European market integration has been one of the great economic success stories of the past 30 years. But the movement seems to have lost steam. In fact, as the much-hailed "Europe '92" arrived, most…