DOWNLOAD

DATE

MEET THE AUTHORS

Contact

Pressure to decarbonize, green development, and geopolitical strife are straining Europe’s natural gas industry. Biomethane, a sustainable substitute to natural gas, is key to the EU’s strategy to reduce CO2 emissions and ensure supply will meet demand. Emerging regulations and new technologies have created a framework for future growth. In this Viewpoint, we explain the opportunities and obstacles for new and existing renewable energy business players.

THE REGULATORY PUSH

Geopolitical upheaval and the EU’s resulting decision to move away from Russian gas have strained Europe’s capacity to supply natural gas, endangering its industries and the households reliant on gas for heating. To limit future dependence on natural gas imports from third-party countries, the EU has started to enact policies to put forward biomethane as a key substitution.

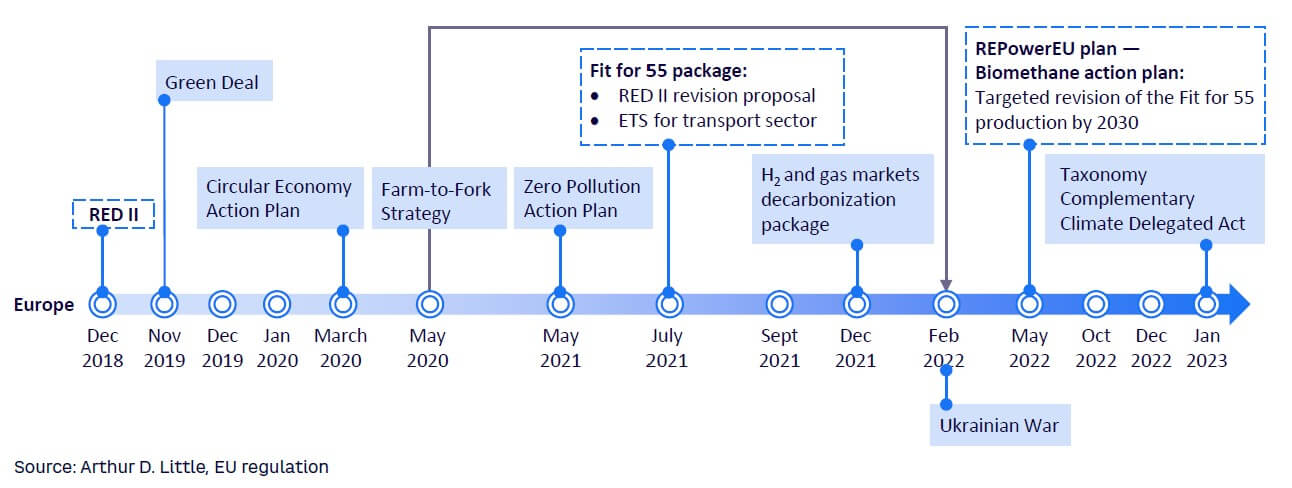

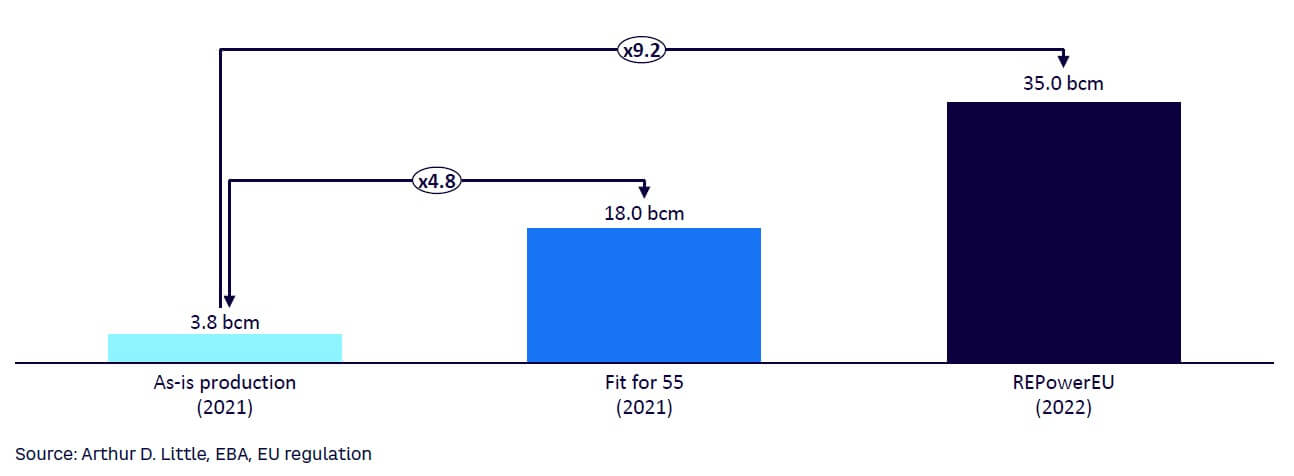

In 2018, before biomethane was the main focus, the EU adopted the second iteration of the Renewable Energy Directive (RED II), which increased renewable energy targets. Biomethane’s lack of prominence changed with two quick updates: Fit for 55 (2021) and REPowerEU (2022), which were both enacted in response to the European energy crisis (see Figure 1). Suddenly, biomethane became one of the key solutions to the decline in natural gas supply, with 2030 production targets increasing from 18 to 35 billion cubic meters (bcm) between Fit for 55 and REPowerEU, as shown in Figure 2.

MOVING FROM BIOMETHANE TO ADVANCED BIOMETHANE

An atom of carbon with four atoms of hydrogen — when looking at the molecules, there is no major difference between biomethane and natural gas. The latter is a fossil fuel stored underground for millions of years, extracted to burn and release CO2 into the atmosphere. Biomethane, on the other hand, is a type of biogas produced on the surface from plant- and animal-based residuals. These residuals generate emissions through natural decomposition. No new CO2 is released into the atmosphere, which makes biomethane a carbon-neutral fuel.

However, all biomethanes are not created equal. The most efficient way to produce biomethane is by utilizing high-yield crops, such as corn or potatoes, but this approach is controversial: deforestation, crop monocultures, and the need for food security all go against the use of food crops for biomethane.

To prevent misuse of food crops, the EU is pushing the use of “advanced” biomethane, which is primarily produced from waste (e.g., plant residues, manure, communal waste, industrial wastewater). Subsidies, renewable targets, and certificates are the main drivers behind the promotion of advanced biomethane; so far, there are no restrictions on food-based biomethane production.

The EU remains the world’s largest producer of biogas/biomethane. Ranking the second-highest-producing region depends on specifics. China is the second-largest producer of biogas, where national policies have led to a spread of household-scale digesters whose output can be used for heating and cooking. Large-scale facilities are currently being built, but opportunities remain, given the abundance of input materials and large demand. The US is the second-largest biomethane producer, favoring landfill gas recoveries and a much larger focus on upgrading to biomethane. Other leading production hotspots across the world include Thailand (cassava waste), India (municipal waste), Brazil (landfills), and Argentina (agricultural waste). Most countries across the world have strong potential to produce biogas and biomethane thanks to the range of potential feedstocks for production.

THE ROLE OF PLANTS & WASTE

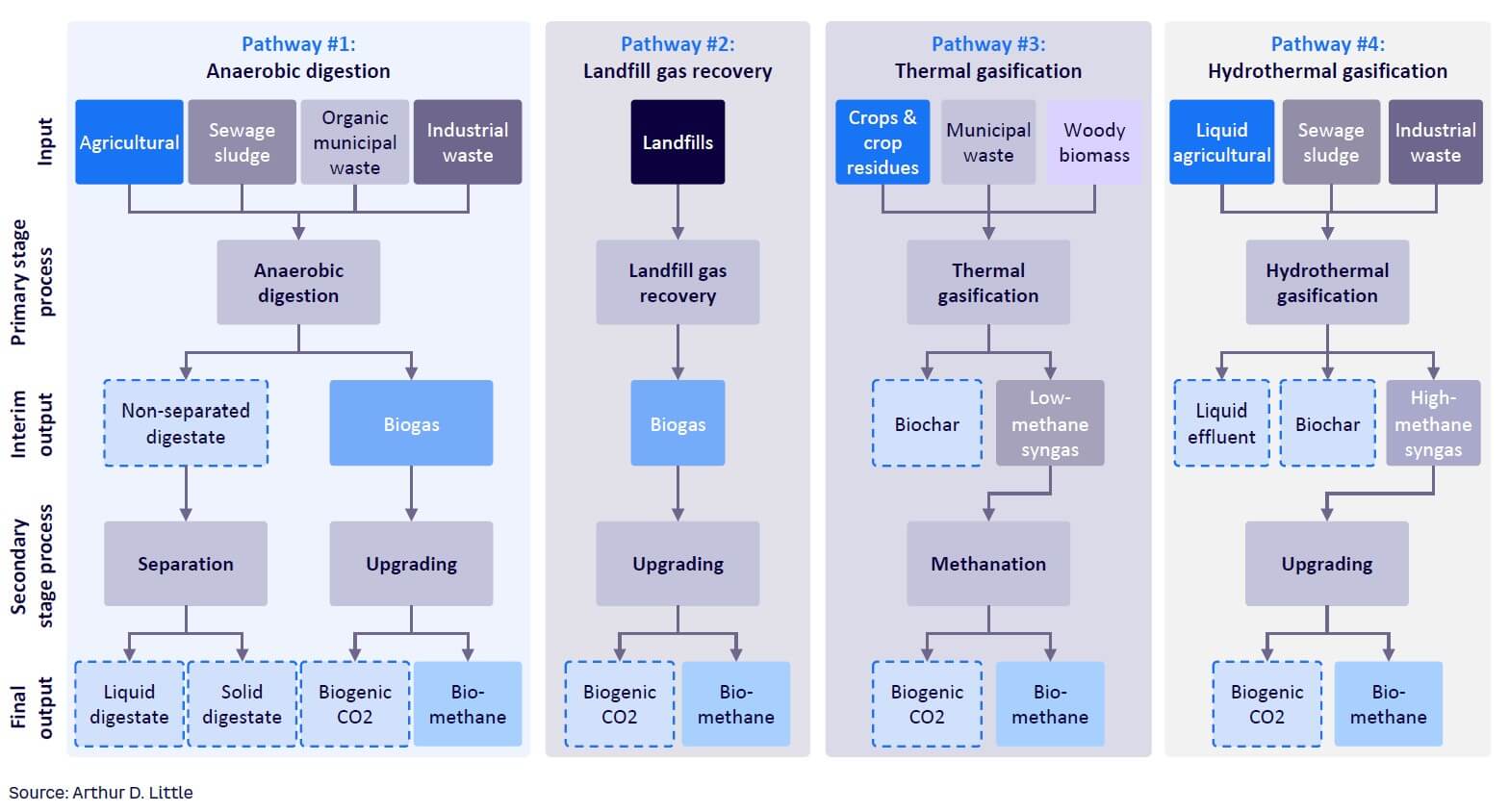

Biomethane can be produced from various feedstocks, ranging from food crops and plant residues to sewage sludge and different kinds of waste. Despite the many possible components, the general production process for biomethane is the same across most technologies and feedstocks. The first process transforms the feedstock into biogas or syngas (synthetic gas) with a methane content of around 50%-60%. The subsequent process separates methane from the other gases, resulting in 98% pure methane.

However, there is a catch: despite similar processes, different types of feedstocks require different technologies, which are summarized in Figure 3.

The four pathways are described in more detail below.

Anaerobic digestion

A feedstock (or a mixture of feedstocks) with a high liquid content is decomposed by microorganisms into biogas. Most common technologies consist of continuous stirred-tank reactors, plug-flow (high dry content), and covered lagoons, with at least four new high-rate technologies currently under research and development. Only about 13% of the original mass is converted into gas; the remaining material is known as “digestate,” which can be used as a biofertilizer or further upgraded through separation of the digestate. As of 2021, anaerobic digestion was used by about 84% of biogas plants, making it the main type of biogas-production technology in Europe. Of these, about 74% of plants use agricultural products such as food crops, plant wastes, and manure.

Landfill gas recovery

Landfill gas recovery collects methane gas from solid waste deposited in a landfill, which methane-producing bacteria help decompose. The collected gas is a natural by-product of the decomposition of organic material in landfills, which typically contains 45%-60% methane, 40%-60% CO2, and a small amount of non-methane organic compounds. In a typical landfill, it takes five to 10 years for decomposition to produce a commercially viable quantity of methane gas. The potential for biomethane production from landfills is immense; the US Environmental Protection Agency (EPA) reported that municipal solid waste landfills were the third-largest source of human-induced methane emissions in the United States in 2020.

Thermal gasification

Thermal gasification is a process that converts woody biomass or other solid biomass into syngas. The first step involves breaking down the biomass using high temperature and pressure in an oxygen-deprived environment, resulting in a syngas mixture composed mainly of carbon monoxide, hydrogen, and methane. The syngas is then cleaned to remove acidic and corrosive components before the methanation process begins. During methanation, a catalyst promotes a reaction between the hydrogen and carbon monoxide or CO2, which produces methane. Any remaining CO2 or water at the end of the process is removed, resulting in a pure stream of biomethane.

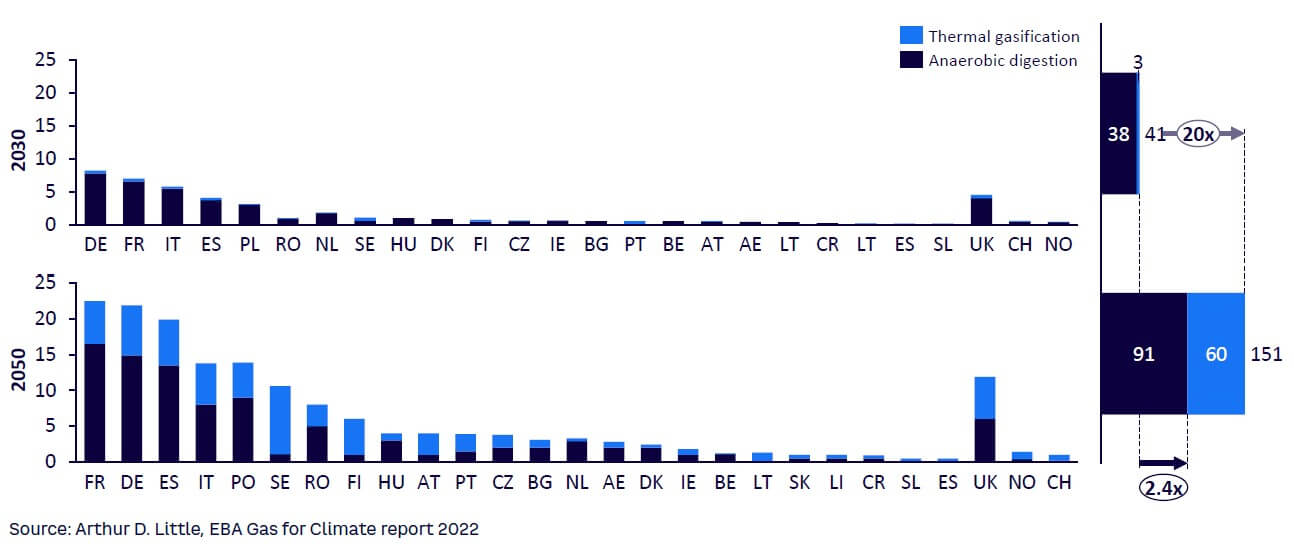

While thermal gasification with biomethane synthesis is still in the pre-commercial phase, there is significant potential to scale up this technology in the mid to long term. According to a report by the European Biogas Association and the Gas for Climate consortium, the potential for biomethane production from thermal gasification in the 27 EU member countries could reach 2.9 bcm by 2030 and 60 bcm by 2050, assuming a more significant introduction of methanation technology into the commercial phase by 2050.

Hydrothermal gasification

Hydrothermal gasification is a promising technology that uses a high-pressure, high-temperature thermochemical process to convert wet biomass and organic waste into synthetic gas rich in methane, hydrogen, and CO2. It offers multiple advantages, such as significantly reducing the amount of final waste and low energy consumption. The synthetic gas produced through hydrothermal gasification can be further upgraded to produce biomethane. The potential for the future of this technology is great, but so far, only a few projects are currently in the pilot and demonstration phases in Europe. The use of hydrothermal gasification could reach industrial scale by 2025, and there are projected industrial projects by 2030 with a cumulative production capacity of at least 1 terawatt hour (TWh).

INCREASING VALUE & DRIVING SUPPLY

Subsidies are a popular tool within the EU but Guarantees of Origin (GoO) certificates are beginning to tip the scales toward increased biomethane production.

GoOs are the main tool enabling biomethane producers to increase their revenues. At the same time, they enable industrial gas consumers to improve their sustainability targets. In simple terms, a GoO is a certificate that proves a megawatt hour (MWh) of methane has been produced in a sustainable way. The required information for a GoO includes the production year, location, and most importantly, the feedstock used, which translates into greenhouse gas (GHG) emissions savings. The use of GoOs for renewable gases was first stipulated in the 2018 RED II. Despite their recent introduction, GoO registers have already been implemented in most EU member states, enabling trade throughout the EU.

Most GoO trades are still mainly conducted “over the counter” (not listed or traded on a major stock exchange), resulting in low price transparency and high volatility. Despite these factors, some clear trends are beginning to emerge. In the most developed markets, such as Denmark or the Netherlands, the GoO for waste-based biomethane is almost twice as valuable as a GoO for food-crop biomethane. With natural gas prices around €50 per MWh, the GoOs are now more valuable than the commodity they represent.

The GoO market used to be mostly voluntary, with sustainability conscious companies buying GoOs to sell “green” gas products or make their gas consumption greener, thus improving their environmental, social, and governance (ESG) scores. But RED II put in place a mandate for fuel suppliers to ensure advanced biofuels (including biomethane) comprise at least 3.5% of road and rail fuel consumption by 2030. This requirement is pushing oil companies to access these markets, thus creating demand for GoOs. The national requirement to create standardized GoO platforms to make consumers aware of the renewable content of their renewable gases will foster those national markets. Since all platforms will be linked though the European Renewal Gas Registry (ERGaR) platform, the individual national markets will become interconnected and GoO will help to create a fostering biomethane development at the European level.

Who should be interested in investing in biomethane production? The answer is quite simple: anyone who wishes to benefit from ROIs of 10% or more. However, certain industries may find easier success in this venture. For example, those in the oil and gas, transportation, and energy utilities sectors may leverage their existing operational models, customer networks, and infrastructure to create synergy and improve their financial performance. Additionally, private equities and infrastructure funds can use their professional management and investments in automation to optimize plant operations and further improve financial performance. Therefore, these industries should consider making biomethane production a top priority in their investment plans.

DIGESTATE: OPPORTUNITY OR OBSTACLE?

Anaerobic digestion, which is currently the most widely used method of biomethane production, also produces a by-product known as “digestate.” This mixture of partially decomposed organic material, nutrients, and microorganisms can be used as a fertilizer or soil amendment. It contains a variety of plant nutrients, including nitrogen, phosphorus, and potassium, as well as trace elements such as iron, manganese, and copper. After the anaerobic digestion process, the initial digestate is in a non-separated form. This product typically contains a mixture of liquid and solid matter, which can be transformed later into separate liquid and solid digestates. However, the existence of digestate is not as positive as it initially appears. Non-separated digestate is difficult to dispose of, as farmers find it more cost-effective to use artificial fertilizers.

The need to dispose of non-separated digestate prompted the EU, in an effort to reduce soil pollution, to establish targets controlling the use of farm substrates (e.g., slurries, manure) as a crop fertilizer or bio-stimulant. Farmers can no longer use substrates without measuring the amount of nitrogen and other nutrients going into the soil. Waste management directives will also require farmers to manage their substrates themselves, which incurs an additional cost. This directive increased substrate treatment costs and made farmers more willing to sell substrates to biomethane plants, while taking a portion of the digestate back for their own use.

In addition to the above, the EU has established a target for total fertilizer consumption to be 20% organic by 2030. Digestate from biomethane plans was included as a feedstock for organic fertilizer production, which has raised the possibility of developing organic fertilizer facilities at biomethane plants.

The above targets and regulations are creating clear opportunities to develop a circular economy by using a business model that complements biomethane project profitability through the transformation of digestate into value-added organic fertilizers. The current market prices of organic fertilizers are above €100/ton and are expected to keep converging with inorganic fertilizers, as organic fertilizer usage requirements increase.

LAND USE: FOOD OR METHANE?

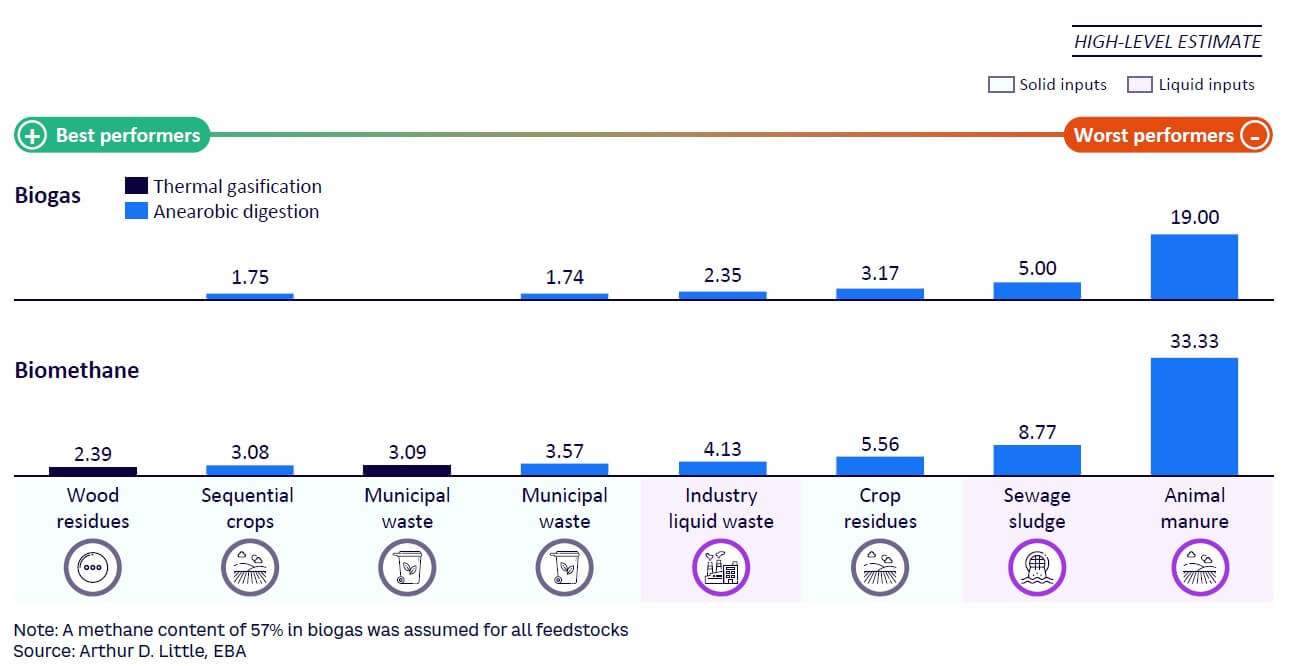

As previously discussed, anaerobic digestion, which primarily uses agricultural products as feedstock, is currently the most commonly used technology for producing biogas. Since it utilizes waste, anaerobic digestion appears to present a win-win situation. However, when production yields are taken into account, it paints a slightly different picture, as illustrated in Figure 4.

A medium-sized household with two to three people consumes about 13 MWh of methane in a year. To cover this consumption, the biomethane plant needs five tons of food crops, seven tons of plant waste, or 40 tons of manure. This translates to 0.13 hectare (ha) for food crops, 1.13 ha for plant waste, and two cows for manure. This represents just one medium-sized household.

A typical biomethane plant has a production capacity of about 2.4 MW (although it can go above 11 MW). To produce the 19.2 GWh of energy needed to run it for a year (with 15% downtime), the plant needs 7,200 tons of food crops (185 ha), 10,000 tons of plant waste (1,820 ha), or 60,000 tons of manure (2,740 cows). This requires a significant logistical endeavor and a vast amount of agricultural land, especially when waste products are used. In a world where food scarcity is a wide-ranging problem, should we use 7,200 tons of food to produce gas for fewer than 1,480 households in a year?

The EU’s support for waste-based biomethane makes its position clear, which should dissuade biomethane plant owners from using high-yielding energy crops. Nonetheless, securing enough waste materials to produce biomethane is a significant limiting factor, as are the logistics to do so. Resolving this issue begins when these technologies (thermal and hydrothermal gasification) shift from developmental to operational. Thermal and hydrothermal gasification will allow the use of high-yielding feedstock such as municipal waste or wood residues, thus leaving food crops for human consumption. However, this may take some time, as the Gas for Climate report estimates thermal gasification will pick up only after 2030, as shown in Figure 5.

Conclusion

THE EU’S PATH TO MORE SUSTAINABLE BIOMETHANE PRODUCTION

At first glance, biomethane appears a renewable and environmentally friendly natural gas alternative. And it can be, but currently a significant number of biogas and biomethane plants are powered by agricultural products — mostly high-yielding food crops. In response, the EU has proposed schemes to promote the production of biomethane from waste. Investors looking to diversify their energy portfolios now have multiple subsidies and revenue streams:

- Commodity sales

- Investment and operational subsidies

- GoOs certificates

- By-product sales

What was once a side business for agricultural producers is becoming a stand-alone business. New technologies will provide an efficient, sustainable business model for producing biomethane from waste, removing the large farm requirement. Energy players can be at the forefront of biogas and biomethane production development and leverage synergies with their other business models.

Unlock a Powerful Difference

RELATED INFORMATION

Capturing business opportunities arising from climate change

New business models emerge in anticipation of the impacts of climate change Climate change is certainly no longer a novel topic and much has been said about its impacts and strategies for mitigation…

Arthur D. Little Japan and Arthur D. Little Ltd (Thailand) have been Commissioned by AOTS for the project 'Promoting Cooperation for Decarbonization in Mae Mo district, Kingdom of Thailand'

Arthur D. Little Japan, Inc. (Head Office: Minato-ku, Tokyo; Managing Partner: Yusuke Harada; hereinafter "ADL"), in collaboration with Arthur D. Little Ltd. (Thailand) have started to support the…

A smart partnership: Arcus, T-Systems and Arthur D. Little combine forces to accelerate smart city deployment

Frankfurt, November 11 2019 - Arcus Infrastructure Partners (“Arcus”), an infrastructure fund with a focus on European infrastructure investment, Deutsche Telekom’s ICT subsidiary T-Systems and…