From the first horse-drawn couriers to drone delivery via creating the “penny black” stamp, the automation of sorting, and so on, postal operators (“posts”) have always adapted. Moreover, given their public service spirit, they have shown great resilience to unforeseen obstacles. This explains their longevity. But digitalization of the economy is changing the context of posts — in a positive way as e-commerce increases but negatively as mail and retail networks use declines. Their resilience is being tested and will require major transformations; posts need to utilize their tools and assets to face up to this and continue their development.

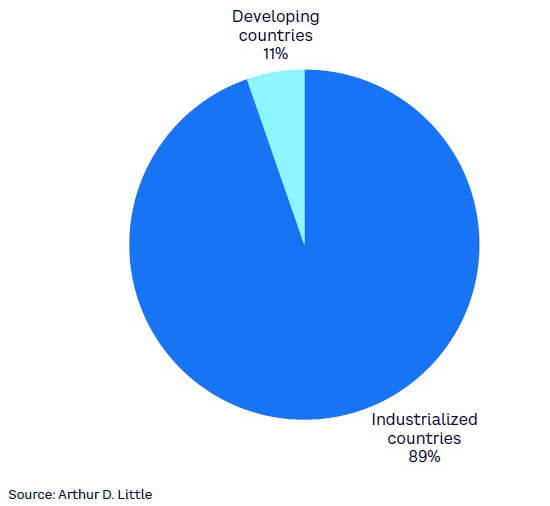

Historically, in order to fulfill their public service missions, posts have deployed large networks for the transport and distribution of physical mail and for direct contact with the public at large for various operations at the retail counter (e.g., delivery of undelivered documents or parcels, postage, payments, banking activities). The relative importance of these activities depends strongly on the country. In particular, mail is a predominant activity in industrialized countries, which account for nearly 90% of total volume processed worldwide (see Figure 1).

TRANSFORM TO STAY ALIVE

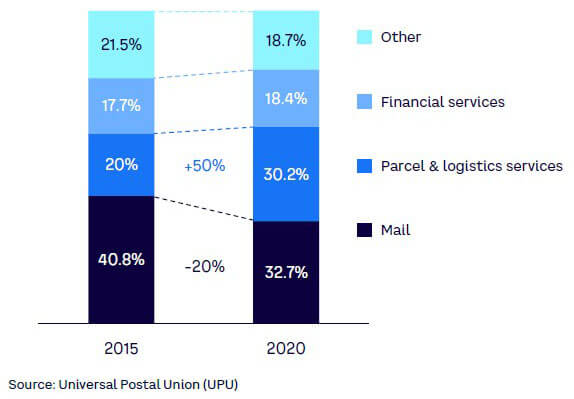

Whatever the breakdown of their business portfolio, all posts are experiencing a rapid transformation of their traditional activities, marked by an accelerated decline in mail volumes; a decreasing utility of their retail networks for historical purposes, which are largely being digitized (e.g., bill payment, government services, banking activities); and the rapid development of logistics and transport of parcel activities driven by the growth of e-commerce (see Figure 2 ). These underlying trends have been further amplified by the disruptions of the COVID-19 pandemic. However, despite the dynamics of demand that have been at work for more than a decade, mail (including personal/business mail, advertising, and magazines/newspapers) still accounts for a major share of the activity of posts — and is still higher than parcel and logistics activities in many countries.

We might think that changes in historical activities could have little effect on the profitability of posts as they counterbalance each other, but this is hardly the case. On the contrary, there is strong pressure on posts’ operating results due to the following challenges:

- Mail, where it has been a developed means of communication, was formerly a very profitable activity, thanks to nominal competition (with the exception of a few countries) and significant economies of scale in the context of high fixed costs. Today’s sharp drop in volumes has gradually reduced these economies of scale, and tariff increases are generally no longer sufficient to stabilize results, forcing posts to reconsider their service model and to request adjustments to the Universal Service Obligations (USOs).

- The decline in the number of people using general public networks for traditional operations is also having a very strong impact on the profitability of posts, given the high fixed costs (staff, real estate) of these networks.

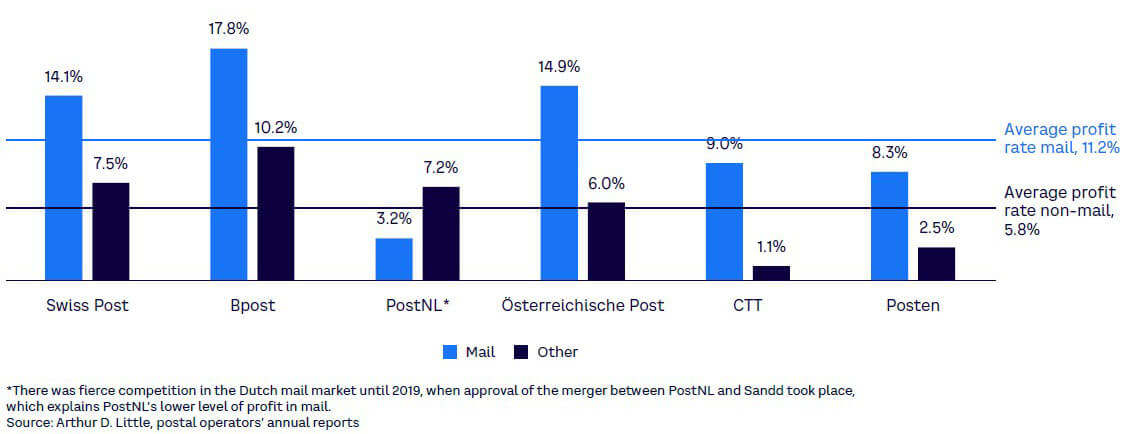

- The parcel business is historically much less profitable than mail (see Figure 3) due to intense competition (its dynamics attract the interest of both traditional players and startups with varied positioning) and, moreover, requires significant investment to meet growth in demand. Generally, economies of scale are much less than in its mail business counterpart and the seasonality of demand is very strong. Both factors limit improvement in results, despite the growth in volume processed.

In these circumstances, posts must manage the decline of their main activities over the long term, while at the same time organize development of growth areas and of e-commerce activities in particular. Therefore, transformation of the business model is no longer optional; it’s mandatory to stay valid.

There are three main strategic priorities for posts:

- Defend/maintain the profitability of their mail business for as long as possible, particularly by transforming their business model, which has not adapted to the significant changing personal/business communications needs.

- Capture the growth of e-commerce in the field of logistics and parcels and develop the competitiveness and profitability of this activity by relying on mail assets.

- Diversify the business portfolio by leveraging mail and retail assets and entering into attractive markets. These diversifications are also useful when it comes to completing the load of mail carriers and office networks in order to better employ them and contribute to the overall profitability of the company.

DEFEND PROFITABILITY OF MAIL IN ALL DIRECTIONS

Posts have long been adjusting to the decline in activity in mail and retail networks. Certainly, there is no “magic formula,” to overcome this challenge, but a combination of actions, when implemented simultaneously, make it possible to defend profitability when the decreases are not too severe.

In addition to promoting mail as an efficient means of communication to alleviate or slow the decline in demand, posts are taking several actions to mitigate costs:

- Offsetting most of the volume decline with targeted price increases.

- Reducing overheads and indirect costs, particularly in the IT and digital areas, by adapting systems.

- Adjusting work rhythms and reducing nonproductive time to achieve a competitive hourly labor cost.

- Adapting the logistics network (sorting and transport) downward, focusing on a smaller number of platforms.

- Optimizing automation and delivery routes.

- Increasing the mutualization of activities in the operational processes.

But this recipe for action has its limits and cannot be renewed indefinitely. Moreover, in the context of mostly fixed costs, decreases in activity end up being prejudicial. The most effective levers for action are therefore those that focus on reducing costs and making them more variable, as well as recreating economies of scale.

USOs, which have changed little in the past despite the transformation of communications media that may have made them partly obsolete, are responsible for a significant proportion of the fixed costs of posts. However, their adaptation or renegotiation are complex, require changes in directives and postal laws by countries, and can be subject to obstacles due to the symbols they represent. Consequently, in order to recreate the economies of scale that in the past have enabled mail to achieve very high levels of profitability, actions may include:

- Outsourcing part of the retail network to third parties.

- Creating and promoting nonurgent products with sufficiently attractive prices for these products to progressively concentrate most of the demand.

- Implementing new organizations at the delivery level (more than 60% of operational costs) with mail carriers working only every other day or every day but alternately distributing across two different rounds.

CAPTURE GROWTH OF E-COMMERCE

The growth of e-commerce is leading to a boom in the volume of business-to-consumer (B2C) parcels, which doubles every four to six years depending on the country, according to ADL analysis.

The four main purchase criteria of e-commerce customers (e-retailers) are:

- Price, because logistics and transport costs are high for merchants, retail margins are low and declining, and also because free delivery for the consumer is a key to success.

- Speed, because there is an elasticity in demand for fast delivery of purchases (impact on the conversion rate proven and impact on demand observed, for example, at Target in the US, where 50% of digital growth is linked to the “same day” delivery offer). This speed reduces the structural handicap of e-commerce compared to physical commerce and explains why “next day” delivery has become the market standard in many countries.

- Convenience/simplicity for the consumer, which is essential for removing barriers to online purchase and building lasting loyalty. Indeed, the delivery experience is a “moment of truth” for the consumer, as all surveys on the subject demonstrate. Depending on the product, this convenience can result from a dense network of parcel pickups/drop-offs (PUDOs) or lockers, as well as the options of delivery to a mailbox, to a neighbor, in the evening, during a chosen time slot (less than two hours), or on demand.

- ESG practices of the logistics providers, particularly with regard to the reduction of polluting emissions. This demand is still emerging among consumers but is becoming increasingly important among e-retailers as logistics and transport providers are investing heavily in this area, with many major players targeting net-zero carbon emissions by 2030.

There are three main positioning options for competitors in this market:

- The low-cost operator seeking to capture the maximum volume of traffic and all types of product categories to cover its fixed costs.

- The operator differentiating through service (e.g., same day, delivery slot) and targeting fewer product categories (e.g., food, wine, household appliances).

- The niche operator for complex products requiring, for example, installation or delivery by two people, which limits the number of product categories targeted.

Thanks to their historical mail and retail assets, posts can compete on all fronts by simultaneously offering low cost and high value-added offerings, all of which can be very competitive. Thus, they can combine the following three positioning aspects:

- A dense network of PUDO points, potentially complemented by lockers.

- A delivery system to mailboxes of small parcels, whose delivery can be mutualized with that of mail and thus be very competitive.

- The use of mail distribution centers as microhubs in cities, enabling delivery by soft modes (cargo bikes, in particular) for more ecological and economical delivery and to develop delivery services (evening or time slot delivery), thanks to the proximity of these urban distribution centers.

This need to develop competitive and differentiated offers for parcel delivery is particularly important for some posts that are additionally challenged by players like Amazon on logistics and last-mile delivery.

LEVERAGE NETWORK ASSETS TO DIVERSIFY REVENUES

For a long time, posts have been diversifying away from the business of communications and transport of small domestic goods. They have been building leaders in financial services and banking/insurance, such as Japan Post, Poste Italiane, and La Poste, with activities that initially benefited from the mutualization of the retail network, but also by going outside their own countries to extend their networks and cover transnational express and parcel exchanges as the globalization of the economy progressed (e.g., Deutsche Post DHL, Royal Mail/GLS, La Poste/DPD, Japan Post/Toll). (Note: here, we do not address these diversifications at the international level or in the field of banking/insurance.)

Diversifications are necessary for postal companies because the sharp decline (or even the potential disappearance) of their historical activities in mail and retail completely challenges their domestic business models. Diversifications may take the form of positions in new businesses that have no particular connection with traditional activities or, conversely, of developing in coherence and synergy with them. In this case, their purpose is twofold:

- Enhance the value of commercial or productive assets (the networks) in attractive new markets, where these assets can contribute to the creation of a competitive advantage.

- Bring additional workload to the different networks by contributing to cover part of their fixed costs, which are important.

For posts, these diversifications can be done in three main domains close to their historical activities: (1) physical distribution (valorization of the retail network), (2) communications (by extension of the usages of the mail), and (3) logistics and transport (valorization of the mail-parcel network). Lessons to be learned from such diversifications include:

- The diversification of the retail networks of posts has most often been a failure, which explains the very high level of outsourcing of these networks by posts that do not offer banking or insurance services. The main significant exception is the development of mobile virtual network operators (MVNOs), whose offer is marketed in post offices (e.g., in Italy and France).

- The diversification of posts into digital communications has most often been a failure, consuming a lot of cash for disappointing results. However, there are exceptions, especially when they have been initiated in collaboration with governments to support paperless policies.

- It is in the field of logistics (and reverse logistics, or the circular economy) that diversifications are both the most natural (in line with the assets and know-how of the posts) and the most attractive, with developments in terms of service (same-day delivery, time-slot delivery), format (from letter to pallet), and products (e.g., fresh food, healthcare, sensitive products).

Conclusion

Transform on three pillars and prepare for next transformations

For posts, in the context of a severe decline, or even disappearance, of their historical activities, and with the simultaneous very strong growth in e-commerce, doing nothing is not an option. In fact, their salvation will come from in-depth transformation. In the short term, three major reorientations are necessary:

- Transformation of the historical business model.

- Development of a strong competitive position on the e-commerce parcel, thanks to the historical assets.

- Diversifications in new businesses.

All this must be carried out simultaneously with a dual ecological and digital revolution. Moreover, posts must follow an in-depth transformation, one that will continue to evolve and always anticipate the next move, because a vast array of new technologies — net-zero carbonization, robotic process automation, autonomous vehicles, or blockchain — will demand continuous transformation in an increasingly digital environment. More than ever, CEOs and their teams need to work with an ambidextrous mindset that balances creativity and rigor in solving today’s most pressing challenges and seizing tomorrow’s most promising opportunities.

Unlock a Powerful Difference

RELATED INFORMATION

Arthur D. Little demonstrates that innovators need to go back to the future to drive change

As part of celebrating 125 years of strategic consulting, Arthur D. Little today outlined how society can learn lessons from history in order to power future innovation. Based on its own experience…

Arthur D. Little: E&P companies need to improve technology strategies and strengthen technology management processes to increase business performance

Mid-sized E&P companies can achieve better business performance through improved technology practices and stronger technology management processes, according to Arthur D. Little’s latest…

Saudi telecoms regulator receives 19 applications from European, Asian and Gulf operators

Arthur D. Little (ADL), the global strategy management consulting firm with a significant presence in the Middle East, has witnessed immense success in its role as an adviser in the liberalisation of…