Environmental, social, and governance (ESG) provides financial services businesses with a framework for funding and de-risking the shift to a greener world. It offers banks an enormous revenue opportunity by introducing green products and services to new and existing customers. However, greening finance requires changes in culture and mindset and expanding ESG considerations to include an economic perspective, thus creating ESGE (environmental, social, governance, and economic). This Viewpoint explains how banks can innovate and unlock ESG’s revenue potential.

FROM BUZZWORD TO BALANCE SHEET

In recent years, banks have aspired to become more sustainable by investing heavily in resources for greening their own operations and meeting regulatory targets, as detailed in the Arthur D. Little (ADL) Prism article, “Actively shaping the future — The new imperative for financial services.”

Banks now need to move their attention beyond compliance and take concrete steps to reap the economic benefits of innovating and launching new ESG products and services. Like a game of football, they must think both offensively and defensively. This approach addresses two client-related challenges:

-

Defensive — Keep existing clients. Corporate and retail clients are increasingly asking for green and sustainable products and services, on both the investment and lending sides. Corporates are also looking to work with like-minded partners, such as banks, as they accelerate and fund their own sustainability and green transition journeys. In research carried out by ADL and leading Austrian financial services provider Erste Group, 80% of Austrian corporates said that sustainability was of very high or high importance. However, 76% were unaware if their bank offered ESG products and services despite half the respondents (46%) citing sustainability as very important to their relationship with their bank. Half the companies that were aware of their bank’s ESG products were using them. Studies in other countries and our client work indicate similar results. Can you afford to lose nearly half your corporate clients through inaction?

-

Offensive — Grow client base. Over 60% of clients in the ADL/Erste Group study wanted their bank to do more on ESG by becoming greener as well as offering additional green products and services. Using ESG innovation to launch new products and widen portfolios gives banks the chance to reposition themselves in the market and win new business. Expanding ESG capabilities extends their reach and increases revenue potential.

Making the shift to offering ESG products and services entails a multistage process, which begins with focusing on clients and their specific needs, as outlined below.

1. Identify your starting point

Every bank’s ESG situation will differ, shaping the strategy and structure they need to adopt. How a bank embraces ESG and derives value will depend on multiple factors, including:

-

The bank’s business model.

-

The ESG goals (i.e., does the bank want to be a leader, follower, or merely defend its existing customer base?).

-

The distribution of client segments, such as retail and corporate, which includes micro-enterprises, small and medium-sized enterprises (SMEs), large organizations, and private banking (including affluent clients).

-

Client demographics, their access to capital, and how they impact awareness of and interest in ESG.

-

Business lines (e.g., lending, investments, services) identified as the most important for top-line growth, and how ESG can be factored in.

-

Operational geography and ESG awareness in countries and/or regions where the bank operates.

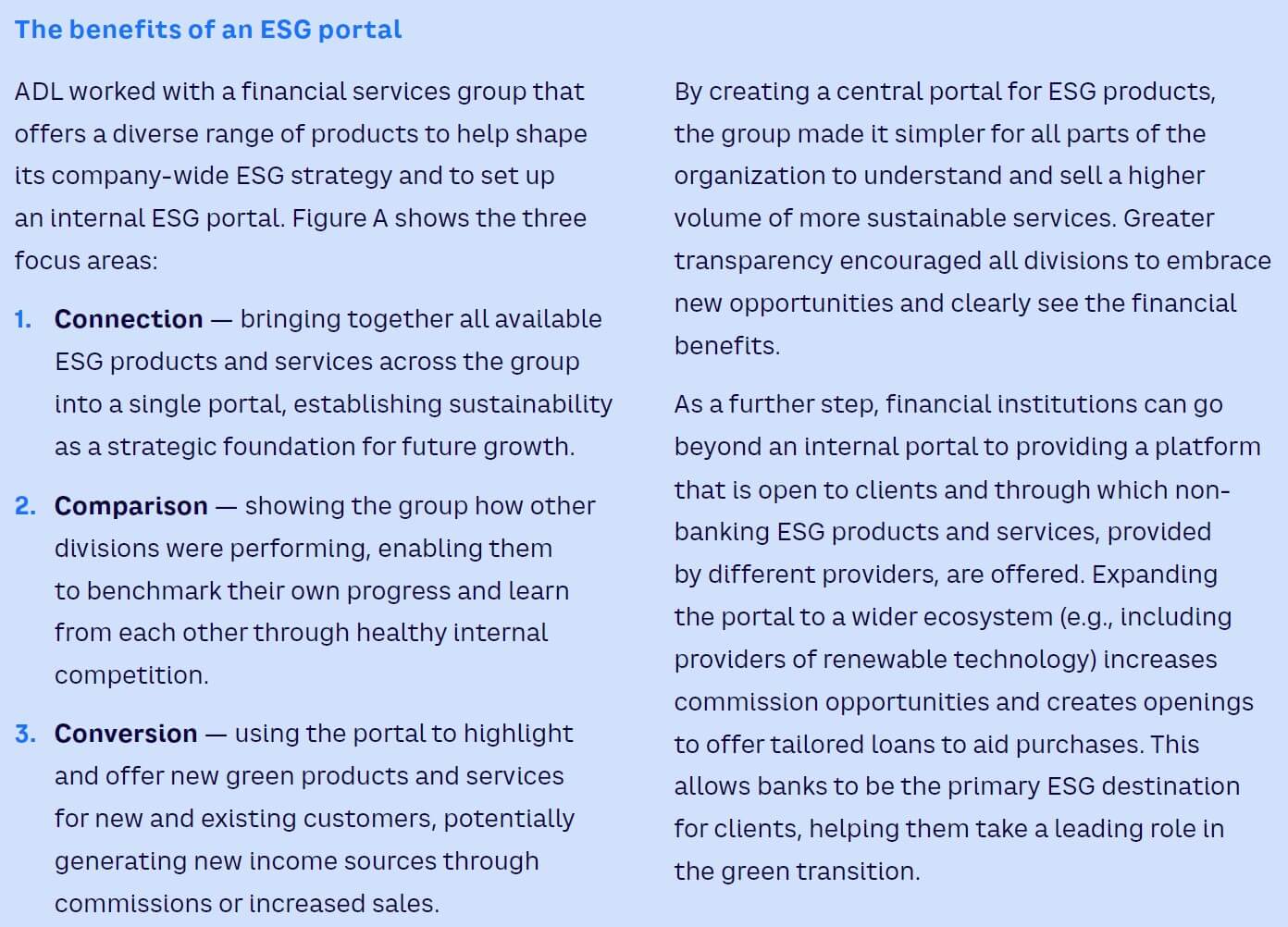

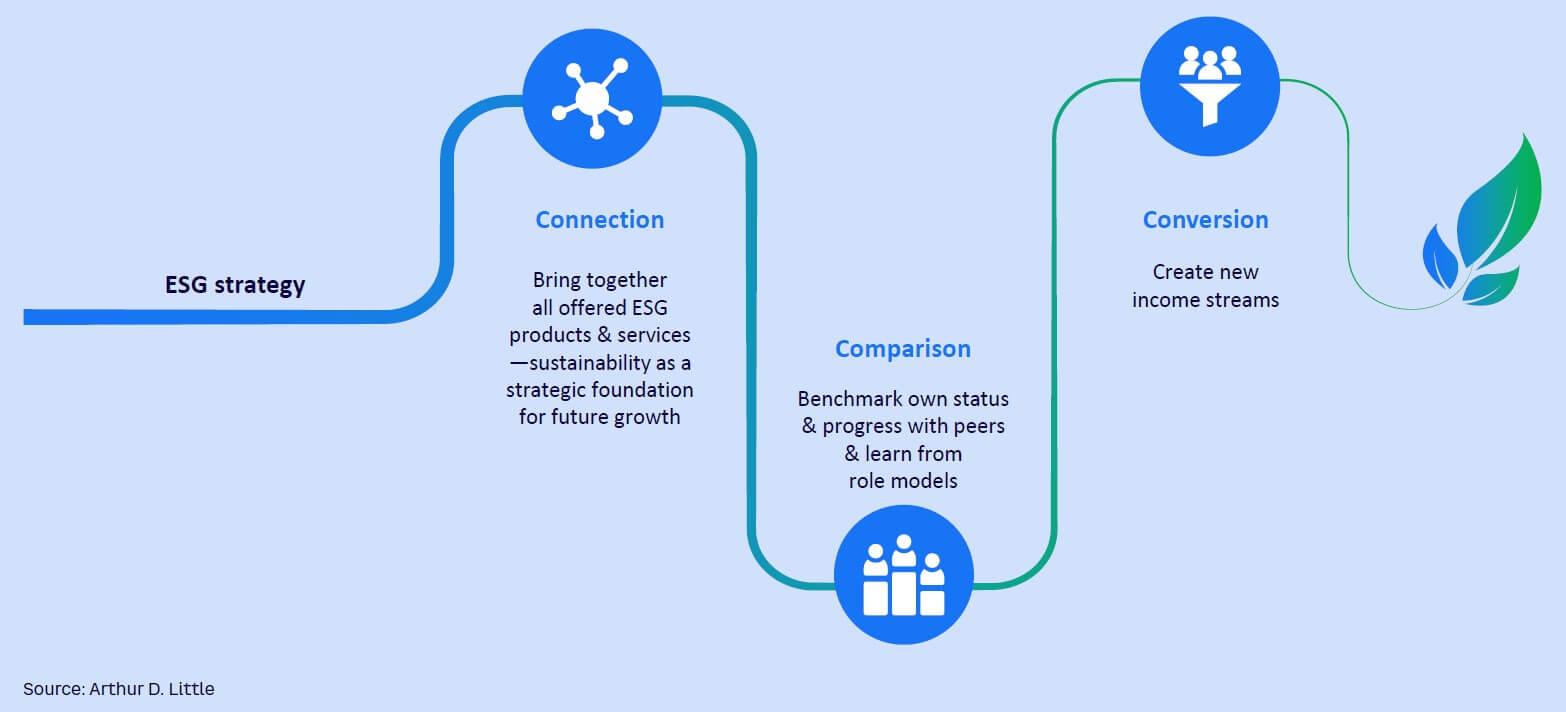

Alongside these factors, a whole ecosystem of new green technology players is emerging. These businesses feature a broad range of services from providing ESG data to supplying consumer products like solar panels. Banks can partner with these companies — both to meet their own ESG transition and reporting requirements and to equip their customers with solutions for better sustainability and to support them with green transition finance. Partnerships help increase engagement with customers and cement the bank’s position as a trusted provider of ESG products and services. Extending client relationships and opening new revenue streams are two additional advantages of partnerships.

2. Make the customer the heart of your ESG strategy

A growing global interest in ESG among retail and corporate customers provides banks with a clear opportunity to grow their offerings. However, every bank’s customer base varies in ESG awareness and large variances exist within demographics, countries, and sectors.

So start by talking to customers and listening to their needs; this will inform value creation by developing and delivering the right products and services. Rather than relying on generic surveys of the wider market, banks must focus on their own customers and what they expect. Gathering this information requires in-depth research and listening exercises to gain a clear understanding of opportunities based on what customers require. Upon accomplishing this task, banks should then repeat the exercise across the wider market to learn what potential customers expect and are looking for in ESG products.

3. Cultivate new ESG capabilities

After identifying opportunities and seeing how they link to overall strategy, banks need to focus on which initiatives and tools will help generate ESG success. Launching green versions of existing products through existing channels is not sufficient. Instead, banks must analyze the factors that lead to ESG lending leadership with target customers. These might include a stronger focus on user experience; integration to new ecosystems or partnerships; or promoting specific, need-based solutions.

Planning successful products involves identifying multiple factors, such as key performance indicators (KPIs), governance, processes, and data. Growth cannot happen without understanding the necessary actions and investments. After defining KPIs, the next step is deciding which initiatives and products to prioritize, taking the following factors into consideration:

-

ESG impact.

-

Economic impact.

-

Implementation time and effort.

-

Availability of required resources and expertise.

4. Build an ESG-first culture

ESG has evolved within financial services. It began as a niche area, before becoming a compliance responsibility, linked to a bank’s license to operate. Next, it evolved again as an essential piece of reputation management and corporate social responsibility (CSR). Now, further transformation will be brought on by embracing ESG’s business relevance and economic impact — and treating these capabilities as levers for value creation.

Banks should therefore use their understanding of client expectations and ESG value drivers to create and define concrete use cases in specific areas, such as SME lending. However, it is one thing to understand client needs, and another to effectively position and sell new ESG products. Often, the issue is cultural, with bank staff, particularly relationship managers, remaining focused on previous product lines that they know, understand, and feel confident about.

Transformation therefore relies on a cultural change that can only come out of a behavioral shift. The following factors are key when involving and engaging relationship managers with ESG:

-

Training and education. Invest in training and certification for relationship managers by accessing the growing number of courses and exams administered by organizations such as the United Nations Environment Programme Finance Initiative (UNEPFI), banking associations, universities, and other financial trade bodies. For example, Deutsche Bank has committed to training its product experts to standards certified by the Chartered Financial Analyst (CFA) Institute or the European Federation of Financial Analysts Societies (EFFAS). In addition, J.P. Morgan runs an ESG Masterclass Series and Goldman Sachs provides ESG training globally to relevant employees.

-

Incentives and bonuses. Explore new forms of compensation that encourage relationship managers to engage with and responsibly sell ESG products. Be transparent and publish clear remuneration policies for all staff that involve ESG and CSR objectives as part of overall governance. For example, BNP Paribas has outlined on its website the rules it follows when calculating the annual variable remuneration of executive corporate officers, including factors such as the bank’s ranking for extra-financial performance in independent league tables.

-

Senior-level visibility. Demonstrate that ESG, and more importantly ESG products, form the core of the bank’s future. Lead programs from the top and heavily involve senior management and the board. Bring in a chief sustainability officer and other employees with the right skills at the senior level, backed by ESG product managers.

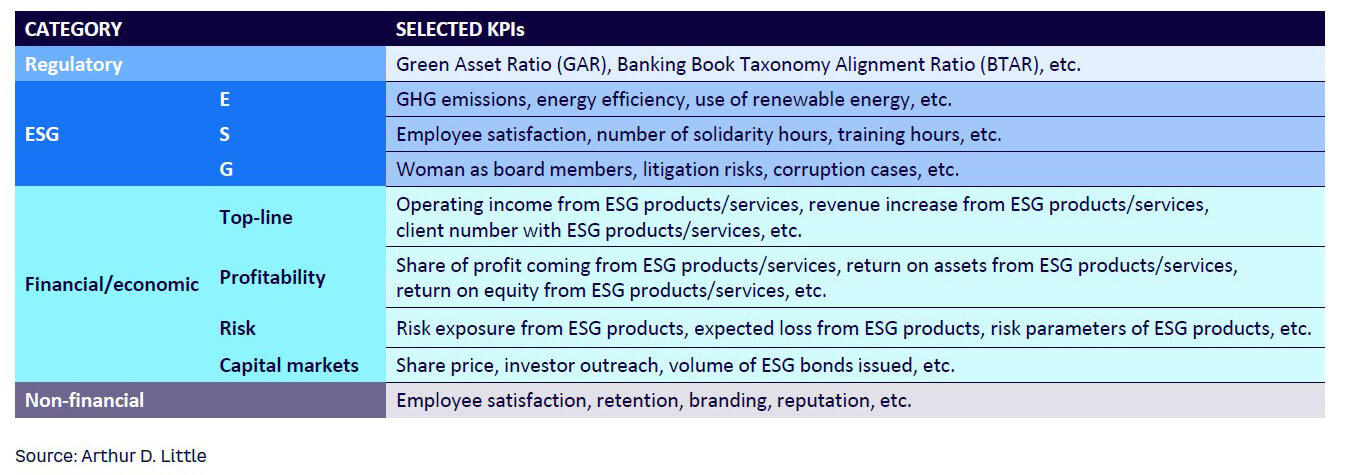

5. Tailor metrics to your program

There are manifold KPIs for measuring ESG progress, success, and its impact on the business. These ESGE KPIs can be split into four main groups, as illustrated in Table 1:

-

Regulatory KPIs:

-

Contribute products to regulatory metrics, such as the EU’s Green Asset Ratio (GAR). This indicator defines the proportion of green financed economic activities and investments as a share of total assets.

-

-

Non-regulatory ESG KPIs:

- May vary based on sector but could include:

- Environmental KPIs (e.g., CO2 footprint, use of renewable energy, and energy efficiency).

- Social KPIs (e.g., diversity, equity, and inclusion; training and education; and qualifications earned).

- Governance KPIs (e.g., actions taken against corruption and litigation risks).

- External ESG ratings, although there are wide differences among these standards.

Financial/economic KPIs:

-

Top-line indicators (e.g., revenue increase, new customers).

-

Profitability (e.g., return on assets, return on equity).

-

Meeting risk KPIs (e.g., expected loss from ESG products).

-

Capital market metrics (e.g., share price).

- May vary based on sector but could include:

-

Non-financial KPIs:

-

Employee satisfaction with company progress on sustainability.

-

Branding and reputation.

-

PUTTING ESG INTO PRACTICE WITH SME LENDING

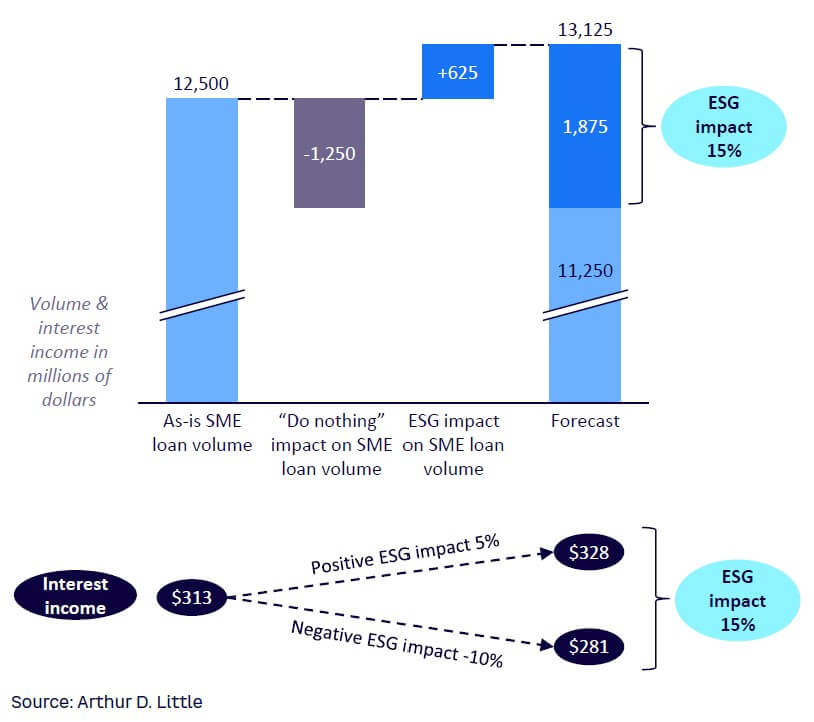

Banks should acknowledge increased interest from SMEs in ESG products — and take action to meet their needs. After all, doing nothing leads to top-line reduction, while doing something provides a good chance of increasing revenues.

We have derived a business case for ESG within SME lending from our past project experience and discussions with clients that have expanded our knowledge. This business case example, outlined in Figure 1, shows the potential financial opportunity within a country with an annual volume of SME loans valued at US $250 billion.

A bank with a 5% market share (equivalent to $12,500 million) and a 2.5% interest rate will earn $313 million in interest income. This market share can be increased to $13,125 million without changing pricing through a combination of:

-

Attracting new clients from rivals. Offering ESG investments increases loan volume by a conservative 5% (+ $625 million).

-

Preventing churn of existing clients. Removing the risk of income loss of 10% in the medium-to-long term decreases (-$1,250 million).

This equals a 15% ESG impact on SME loan volume and a rise in interest income to $328 million. Further revenues can be gained through cross-selling opportunities, which could include offering CO2 certificates and ESG advisory services.

Conclusion

SEIZING THE ESG REVENUE OPPORTUNITY

Despite current economic and geopolitical headwinds, ESG is a long-term trend that will only accelerate — and banks need to be ready. ESG provides an enormous revenue opportunity for them to deliver new, tailored products to keep their existing customers and win new business. Therefore, banks need to move from greening the organization to underpinning greater sustainability across customers through new products that can drive future growth. Achieving this requires a focus on seven best practices:

-

Move from ESG to ESGE, fully integrating ESG into your economically sustainable business model.

-

Encourage cultural change by promoting awareness of ESG, particularly with customer relationship managers.

-

Understand customer expectations and the products and services they need and want.

-

Create specialized ESG products tailored to different business lines.

-

Build a wider ecosystem by building new partnerships beyond financial services.

-

Engage all stakeholders in an ongoing dialogue as ESG evolves.

-

Invest in the right people and competencies by looking beyond traditional banking skill sets.

Unlock a Powerful Difference

RELATED INFORMATION

Islamic finance comes of age

With the recent announcement by the Saudi capital market of four IPOs in April 2009, Islamic finance is riding high. The traditional values of Islamic finance are growing in appeal for Western…

ACQ Finance honors Arthur D. Little with two annual awards

Today ACQ Finance Magazine announced that Arthur D. Little have been honored twice in the publication's first annual Country Awards for Achievement in the private equity field Arthur D. Little Nordic…