13 min read • Financial services

ACTIVELY SHAPING THE FUTURE - THE NEW IMPERATIVE FOR FINANCIAL SERVICES

Each and every industry must become greener and more sustainable. However, as a key pillar of the global economy and wider society, the financial services sector is in a unique position. It not only must change how it operates to build sustainable business models, but it also has a crucial role to play in funding and de-risking the transition towards climate neutrality. The financial services sector can become the driver of green change.

Seizing the initiative around sustainability and demonstrating true leadership can transform how the sector is viewed – by consumers, regulators, and existing and potential employees. It provides the opportunity to fundamentally reposition financial services away from being seen as part of the problem, to leading the solution.

The stakes are high. Yet despite the enormous interest in environmental, social and governance (ESG) issues, the majority of financial services organizations are still in a passive, reactive mode. Many see growing green regulatory requirements as a cost to be met, not an opportunity to be grasped. While they trumpet their green credentials, often they achieve this through offsetting existing activities – planting trees, buying CO2 certificates and paying fines, rather than changing their business models.

To remain relevant and achieve competitive advantage, banks, insurers and asset managers need to move from a passive position to become active shapers of the green, sustainable future. Otherwise, traditional players risk being outflanked by new ESG-focused entrants, which is exactly what happened with fintech start-ups during digitization. Time is running out for financial services companies to make this fundamental shift.

How can players make this change and shape a sustainable future for themselves and the planet? In this article we look at how they can rebalance their capabilities, mobilize stakeholders, and move ESG from talk and commitments to concrete, positive action.

THE CURRENT LANDSCAPE

While sustainability is not a new topic, it has gained significant traction in financial services over the last few years, which has moved it center stage, driven by a range of stakeholders including governments and regulators, investors, and clients themselves. At the COP26 conference, a range of initiatives and plans were announced. Over 90 percent of global emissions are now covered by Net Zero commitments. However, this needs to be backed by concrete short- and mid-term action to ensure long-term commitments are met.

This has led to a range of plans, agreements, and frameworks, including:

– The UN Principles for Responsible Banking (PRB). This was created in 2019, and 275 signatories now represent over 45 percent of the global banking system by assets, mobilizing $2.3 trillion of sustainable finance. Similar sets of principles cover insurance and investment.

– The Glasgow Financial Alliance for Net Zero (GFANZ), which covers more than 400 financial institutions and includes the Net-Zero Banking Alliance (103 banks representing over 44 percent of global banking assets), the Net-Zero Asset Owner Alliance (70 institutional investers with $10.4 trillion of assets under management) and the Net-Zero Insurance Alliance (over 20 insurers representing more than 11% of world premium volume globally).

– The Global Alliance for Banking on Values (GABV), a network of independent banks using finance to deliver sustainable economic, social and environmental development. It comprises 67 financial institutions operating in 40 countries across the world. Collectively, they serve more than 60 million customers and hold over USD 200 billion in combined assets under management.

– The UN Environmental Program Finance Initiative (UNEPFI), in which 4,000 businesses have committed to aligning their business model to Net Zero by 2050 and the lower 1.5 degree target for global warming.

These bodies all aim to accelerate change through a systemic, comprehensive, science-based, time-bound, measurable, transparent, and immediate approach.

Regulators and supervisory authorities are also increasingly active. For example, the Bank of England has become the first central bank to add green criteria to its corporate bond-buying program, while the ECB has committed to including ESG considerations in its monetary policy, as well as making ESG a supervisory priority. This increases pressure on financial institutions.

Some progress has been made on both the debt and equity sides. For example, EUR 358 billion of green bonds were issued between January and September 2021. There are now approximately 4,000 green bonds outstanding, with volume of EUR 1,084 billion – this is 0.9 percent of all outstanding bonds. On the private equity side, firms are increasingly incorporating ESG considerations into their investments, with many ranking it as a top factor in value creation.

However, overall ESG activities have not met targets:

-

While 93 percent of PRB members are analyzing the impact of their activities, just 30 percent are setting targets to reduce the effects. Twelve percent have created processes to regularly consult stakeholders.

-

Figures from Bloomberg show that in the first nine months of 2021, banks organized USD 459 billion of bonds and loans for the oil, gas and coal sectors, alongside USD 463 billion worth of green bonds and loans.

-

While the availability of green finance has expanded, the sums required are immense. The UNEPFI estimates that an additional USD 60 trillion is needed to transition to low carbon, climate-resilient economies by 2050.

Communications and commitments are ahead of activities on the ground. This risks the credibility of financial institutions with stakeholders, and leaves them open to accusations of “greenwashing” and insufficient ESG focus. Additionally, there is a need to take immediate action if commitments are to be delivered – many changes required by 2030/2050 cannot be reached unless work begins now.

There are certainly key challenges that must be overcome:

-

Uncertainty over the definition of key terms, leading to guesswork when setting and evaluating strategy.

-

The unavailability of quality ESG data across the supply chain to underpin decision-making. For example, while the EBRD is exploring the digitization of green finance, a lack of comprehensive, reliable end-to-end ESG data may hold back progress.

-

The absence of market standards when it comes to ESG ratings. For example, comparing the evaluations of different ESG rating providers across major banks shows wide variability between these different providers.

-

Missing incentives for financial institutions to focus on ESG while delivering expected shareholder returns.

-

A lack of knowledge and skills within banks, exacerbated by the need for a cultural shift to put ESG center stage.

Many of these challenges have been previously faced by other sectors on their ESG journey. However, unlike manufacturers or consumer goods companies, financial services companies don’t provide physical products. While they can – and must – achieve Net Zero in terms of their operational footprint, true sustainability requires ensuring that clients and customers are also Net Zero. That means leveraging customer relationships and driving ESG impact by changing their behavior and becoming an internal sparring partner to drive transformation, rather than simply excluding certain industries or clients.

HARNESSING THE OPPORTUNITIES

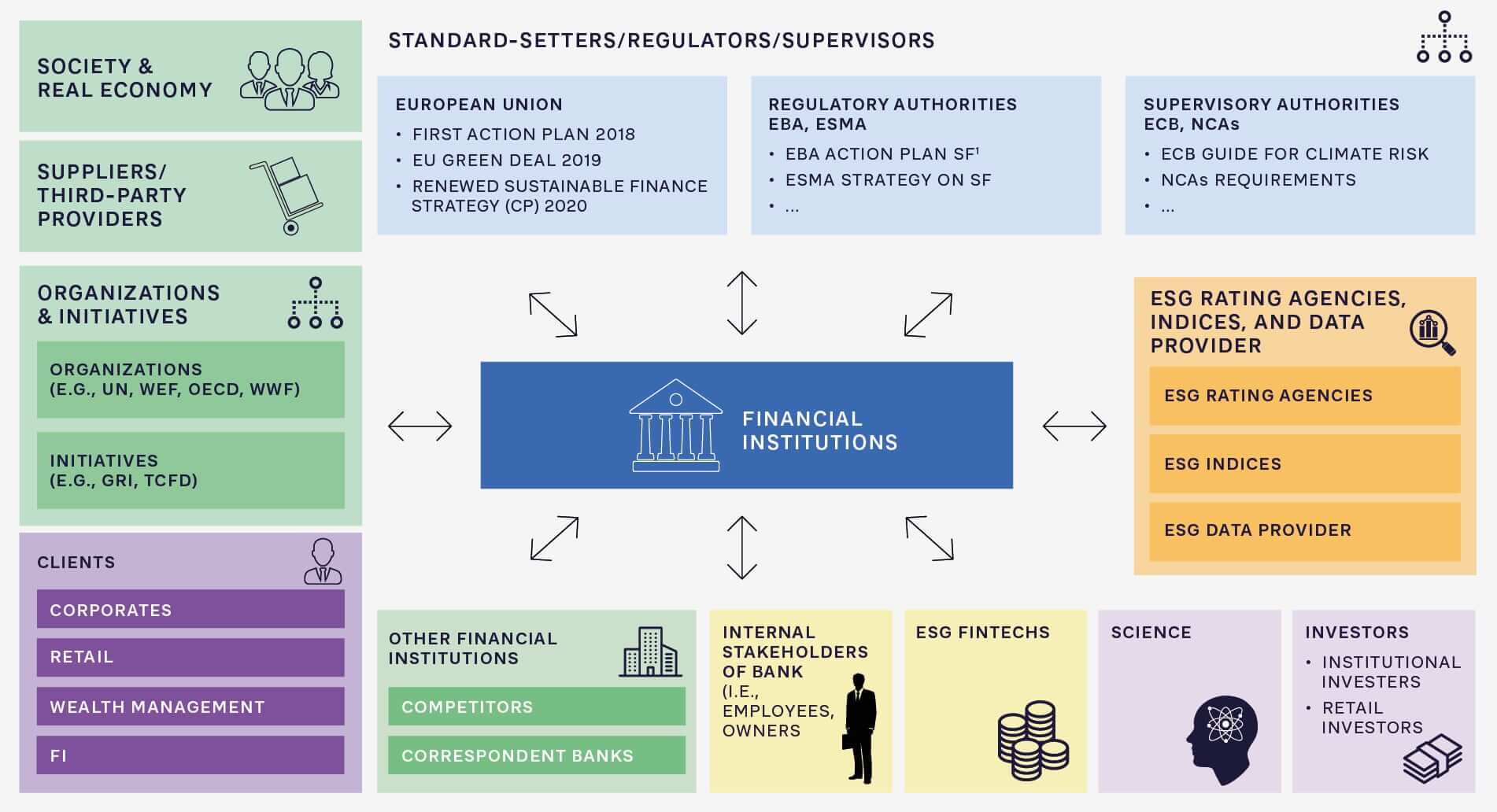

Shaping the future requires financial services companies to take an ecosystem approach that brings together public, private and third- sector partners. In such a complex environment, everyone needs to play a complementary role; however, as in an orchestral performance, it needs to be conducted well for the duration of the concert, with all players displaying commitment and ongoing dedication.

Figure 1 highlights the complexity and diversity of the ecosystems that financial institutions need to play in. These broadly fit into four stakeholder groups, as classified by the UNEPFI:

-

The financial institutions themselves, including employees and partners, as well as the wider financial sector

-

The real economy, such as customers that access and benefit from financial institutions

-

Policymakers and regulators, at both a national and supranational level

-

Science and technology providers delivering solutions for sustainability

FIGURE 1: THE ECOSYSTEM OF FINANCIAL INSTITUTIONS

Achieving success is a long-term process. After the sprint of initial discussions and signing up to commitments, ESG transformation is a marathon.

Senior management in financial institutions therefore needs to focus on transformational change in key areas:

1. Make ESG the board’s top priority

ESG is not just an add-on, but also must be an integral part of the business model. It cannot be siloed or delegated to risk or marketing teams. Financial institutions need to build a clear, credible, and holistic sustainable finance strategy. Mind-sets, culture and conduct must change. Led from the top, this strategy needs to establish the business case and define how the organization will position itself from an ESG perspective. This should also set out risk options, as well as show how technology can be used to mitigate these risks. All of this should be captured in long- and short-term roadmaps for transitioning to a desired ESG state.

2. Prioritize long-term value creation

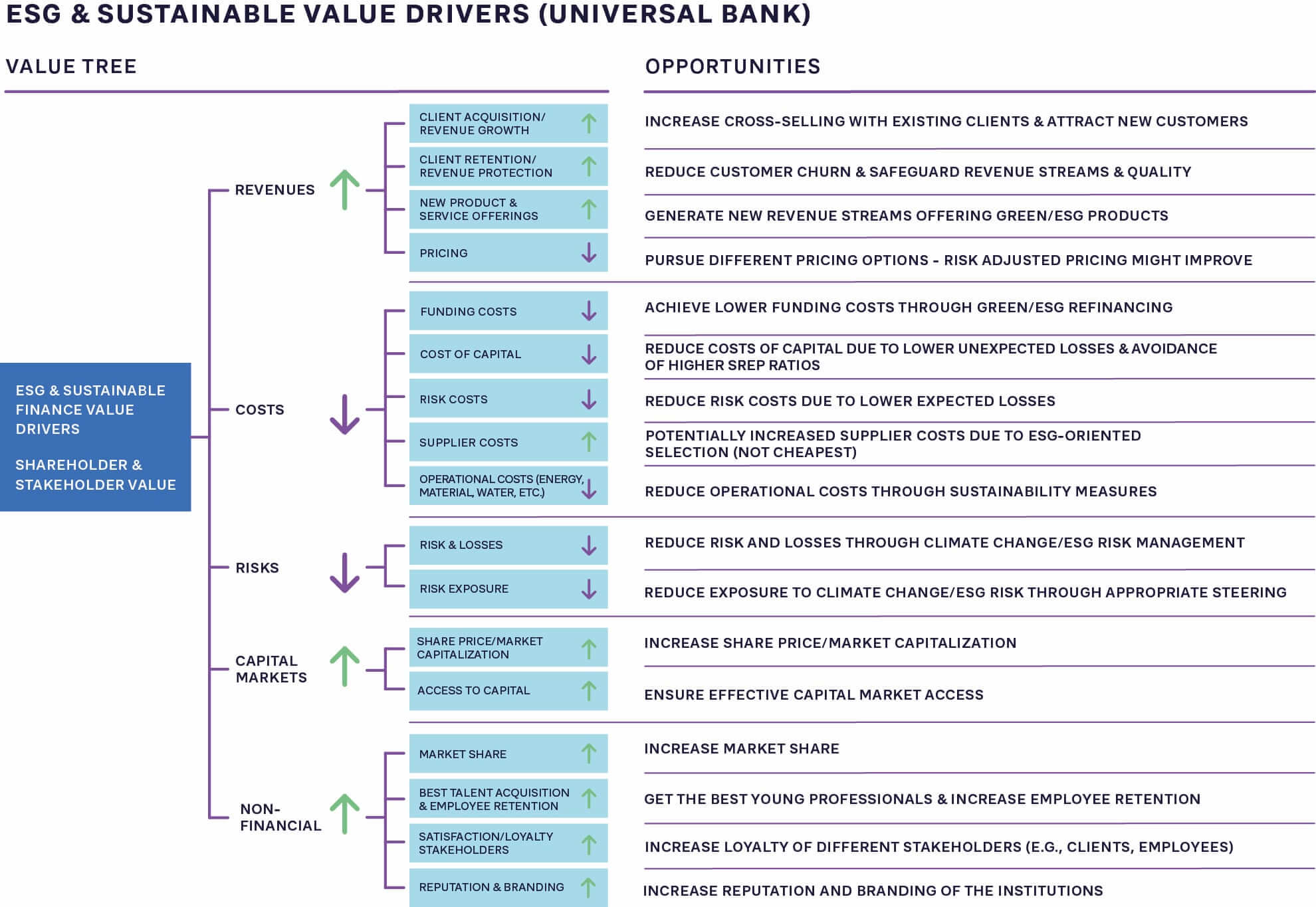

Ensure that ESG and sustainable finance-oriented strategies and business models prioritize long-term value creation for shareholders and stakeholders, rather than focusing simply on short-term returns for the bank itself. Strategy must be based not on today’s worldview, but on one that will apply in five to 10 years.

It is vital to redefine what success means – moving from measures such as return on equity to look at the bigger picture. Institutions need to adopt a “shared value”-oriented philosophy that takes into account different stakeholders and their needs, as well as incorporating the wider economy and society, remodeling incentives. ESG strategies unlock value drivers that impact the top and bottom line, as Figure 2 demonstrates.

FIGURE 2: ESG AND SUSTAINABLE VALUE DRIVERS

3. Take real action now across your ecosystem

“Wait and see” is no longer a viable option, especially if you want to gain any kind of first-mover advantage. Differentiate by making real commitments that go beyond regulatory bare minimums, build well- resourced ESG capabilities, and put in place the frontline processes to ensure you take action to deliver on them. For example, leading banks are remodeling their relationship management programs to better serve client needs through ESG early-warning and opportunity detection systems that increase transparency over their portfolios.

The sheer volume of risk-tolerant, flexible capital required to drive change goes far beyond the capabilities of a single institution or government. New partnerships – in the public, private and philanthropic sectors – will be required, and all sides will need to work together to define sector-specific pathways to Net Zero. For example, HSBC has launched a Climate Solutions Partnership with the World Resources Institute and World Wildlife Fund to finance companies and projects tackling climate change, backed by USD 100 million of philanthropic funding over five years.

4. Actively drive change in corporate and consumer customers

Financial institutions have the opportunity to build a sustainable, diverse future by becoming a transformation partner of the businesses that they invest in and work with. Effective transformation requires close engagement with clients, to the extent of working alongside or inside companies to ensure they become greener and more sustainable. This approach works better than simply dropping certain types of customers because of their historic record on sustainability.

On the consumer side, banks need to educate customers, building their ESG financial literacy so they are actively seeking out and demanding sustainable financial products, and therefore driving change. Institutional investors are already setting strict targets for ESG compliance – banks need to ensure consumers are applying the same pressure if they are to be seen as relevant and on the side of sustainability. This is particularly important given current excess liquidity levels, high inflation and low interest rates, which are destroying monetary value in real terms. Educating consumers to reallocate their savings to ESG products unlocks major new funding opportunities.

5. Engage with regulators and policymakers early

The financial crisis and other misconduct led to not only greater regulation, but also an adversarial relationship between banks

and regulators. Rather than fighting, financial institutions should demonstrate why they deserve to be involved in setting – and leading – new ways of driving sustainability forward. This requires openness and a change of mind-set. Taking an active role in shaping sustainability policies will allow banks and regulators to jointly define the future rules of the regulatory game, and help move the needle at a systemic level.

Process and pioneers

As discussed in this article, the vast majority of large financial services companies have made long-term commitments to increasing sustainability. Many have also launched specific initiatives:

-

Citi’s USD 200 million Impact Fund invests in companies addressing today’s biggest societal challenges.

-

JPMorgan Chase has set up a Green Economy team to provide dedicated banking services and expertise to companies that produce environmentally friendly goods and services.

-

BNP Paribas has created a 250-person Low Carbon Transition Group to support corporate clients and investors in decarbonizing their exposures.

-

Deutsche Bank has brought forward its target date for deploying EUR 200 billion in sustainable finance by two years to 2023.

However, as with digital disruption, ESG is providing opportunities for fintech start-ups to focus on specific areas and opportunities. Analyst company Medici lists over 150 ESG fintechs in its latest study, covering areas such as ESG-oriented products and services, impact investing, tech/ratings platforms, and inclusion initiatives such as mobile money.

Examples include:

-

Aspiration – a US neobank that does not invest customer money into fossil fuel projects. It currently has over 1.5 million customers for its banking service.

-

MioTech – an AI platform that empowers sustainable finance with ESG data and technology. Investors include Moody’s and Horizon Ventures.

While currently there are no ESG gamechangers that have broken through, this state of affairs is unlikely to last. Traditional players that potentially underestimated the likes of trading and banking fintech Revolut (worth more than Deutsche Bank, Japan Post Bank or UniCredit based on its last fundraising), broker app Trade Republic (valued at over USD5 billion) and payment processing provider Stripe (the most valuable venture-backed private company in the US) should not make the same mistake again.

INSIGHTS FOR THE EXECUTIVE

-

Make ESG real. Move from talk to action. Only then will financial services organizations be able to lead the transformational change that is required to deliver a Net Zero, decarbonized economy and benefit from the opportunities it brings. Failure will open the door to being overtaken by the growing number of ESG start-ups and fintechs, just as slowness to embrace digitization spawned new, disruptive competitors.

-

Make ESG bonuses relevant. Get buy-in from your people by ensuring that compensation and incentives from the board down have a substantial ESG component in order to support culture and behavior change. KPIs have to be clear, concrete and measurable – and focus on what individuals can actually influence through their daily actions. As well as changing incentives, clearly communicate what you expect of your people when it comes to ESG. Model the right behaviors yourself and roll out a code of conduct that makes a sustainable focus the norm.

-

Create an ESG unit with authority, reporting directly to the CEO. Set up a dedicated, well-resourced ESG group, located in the CEO’s office. It should be given sufficient power, cross-business scope and staffing to make a difference. Task this team with neutrally reviewing all ESG exposures with both existing clients and any new products that are launched or customers that are won. Go beyond external requirements with more detailed internal reporting to give multiple ESG lines of defense and position ESG as a differentiator with external stakeholders.

-

Create a clear plan to stop financing non-ESG-compliant business. Turn strategy into practice by reviewing the tools, actions, communications and KPIs of all client-facing business units and ensure they reflect your green objectives. Adjust your investment vehicles to make them ESG led in order to gain early- mover advantage. Bring ESG criteria into know-your-customer requirements to minimize any exposure to uncompliant businesses.

-

Make ESG products part of every customer’s portfolio. Educate consumers and businesses that they need to make ESG products central to their financial strategies. Start young – offer products that let children and their parents invest to build and benefit from a greener world. Don’t just rely on traditional bankers to create new ESG products and services. Bring in outsiders to work alongside them and drive innovative new products and services that will differentiate you going forward.

-

Stop hiding – be transparent. There has been a lot of talk about ESG and a backlash against greenwashers (those that are not as green, but try to ride the bandwagon), transition-washers (less advanced in ESG than they communicate) and competency-washers (less expertise than they claim). Commit to full transparency beyond what is required by regulations and take the lead, backed by the right skills, processes and actions.

-

Become a transformation partner. Ultimately, the only real ESG lever for financial services is to influence clients and their behavior. Move from being on the outside to become an effective internal transformation partner with clients. Only by effectively engaging will customers transform and real ESG impact be delivered.

13 min read • Financial services

ACTIVELY SHAPING THE FUTURE - THE NEW IMPERATIVE FOR FINANCIAL SERVICES

Each and every industry must become greener and more sustainable. However, as a key pillar of the global economy and wider society, the financial services sector is in a unique position. It not only must change how it operates to build sustainable business models, but it also has a crucial role to play in funding and de-risking the transition towards climate neutrality. The financial services sector can become the driver of green change.

DATE

Seizing the initiative around sustainability and demonstrating true leadership can transform how the sector is viewed – by consumers, regulators, and existing and potential employees. It provides the opportunity to fundamentally reposition financial services away from being seen as part of the problem, to leading the solution.

The stakes are high. Yet despite the enormous interest in environmental, social and governance (ESG) issues, the majority of financial services organizations are still in a passive, reactive mode. Many see growing green regulatory requirements as a cost to be met, not an opportunity to be grasped. While they trumpet their green credentials, often they achieve this through offsetting existing activities – planting trees, buying CO2 certificates and paying fines, rather than changing their business models.

To remain relevant and achieve competitive advantage, banks, insurers and asset managers need to move from a passive position to become active shapers of the green, sustainable future. Otherwise, traditional players risk being outflanked by new ESG-focused entrants, which is exactly what happened with fintech start-ups during digitization. Time is running out for financial services companies to make this fundamental shift.

How can players make this change and shape a sustainable future for themselves and the planet? In this article we look at how they can rebalance their capabilities, mobilize stakeholders, and move ESG from talk and commitments to concrete, positive action.

THE CURRENT LANDSCAPE

While sustainability is not a new topic, it has gained significant traction in financial services over the last few years, which has moved it center stage, driven by a range of stakeholders including governments and regulators, investors, and clients themselves. At the COP26 conference, a range of initiatives and plans were announced. Over 90 percent of global emissions are now covered by Net Zero commitments. However, this needs to be backed by concrete short- and mid-term action to ensure long-term commitments are met.

This has led to a range of plans, agreements, and frameworks, including:

– The UN Principles for Responsible Banking (PRB). This was created in 2019, and 275 signatories now represent over 45 percent of the global banking system by assets, mobilizing $2.3 trillion of sustainable finance. Similar sets of principles cover insurance and investment.

– The Glasgow Financial Alliance for Net Zero (GFANZ), which covers more than 400 financial institutions and includes the Net-Zero Banking Alliance (103 banks representing over 44 percent of global banking assets), the Net-Zero Asset Owner Alliance (70 institutional investers with $10.4 trillion of assets under management) and the Net-Zero Insurance Alliance (over 20 insurers representing more than 11% of world premium volume globally).

– The Global Alliance for Banking on Values (GABV), a network of independent banks using finance to deliver sustainable economic, social and environmental development. It comprises 67 financial institutions operating in 40 countries across the world. Collectively, they serve more than 60 million customers and hold over USD 200 billion in combined assets under management.

– The UN Environmental Program Finance Initiative (UNEPFI), in which 4,000 businesses have committed to aligning their business model to Net Zero by 2050 and the lower 1.5 degree target for global warming.

These bodies all aim to accelerate change through a systemic, comprehensive, science-based, time-bound, measurable, transparent, and immediate approach.

Regulators and supervisory authorities are also increasingly active. For example, the Bank of England has become the first central bank to add green criteria to its corporate bond-buying program, while the ECB has committed to including ESG considerations in its monetary policy, as well as making ESG a supervisory priority. This increases pressure on financial institutions.

Some progress has been made on both the debt and equity sides. For example, EUR 358 billion of green bonds were issued between January and September 2021. There are now approximately 4,000 green bonds outstanding, with volume of EUR 1,084 billion – this is 0.9 percent of all outstanding bonds. On the private equity side, firms are increasingly incorporating ESG considerations into their investments, with many ranking it as a top factor in value creation.

However, overall ESG activities have not met targets:

-

While 93 percent of PRB members are analyzing the impact of their activities, just 30 percent are setting targets to reduce the effects. Twelve percent have created processes to regularly consult stakeholders.

-

Figures from Bloomberg show that in the first nine months of 2021, banks organized USD 459 billion of bonds and loans for the oil, gas and coal sectors, alongside USD 463 billion worth of green bonds and loans.

-

While the availability of green finance has expanded, the sums required are immense. The UNEPFI estimates that an additional USD 60 trillion is needed to transition to low carbon, climate-resilient economies by 2050.

Communications and commitments are ahead of activities on the ground. This risks the credibility of financial institutions with stakeholders, and leaves them open to accusations of “greenwashing” and insufficient ESG focus. Additionally, there is a need to take immediate action if commitments are to be delivered – many changes required by 2030/2050 cannot be reached unless work begins now.

There are certainly key challenges that must be overcome:

-

Uncertainty over the definition of key terms, leading to guesswork when setting and evaluating strategy.

-

The unavailability of quality ESG data across the supply chain to underpin decision-making. For example, while the EBRD is exploring the digitization of green finance, a lack of comprehensive, reliable end-to-end ESG data may hold back progress.

-

The absence of market standards when it comes to ESG ratings. For example, comparing the evaluations of different ESG rating providers across major banks shows wide variability between these different providers.

-

Missing incentives for financial institutions to focus on ESG while delivering expected shareholder returns.

-

A lack of knowledge and skills within banks, exacerbated by the need for a cultural shift to put ESG center stage.

Many of these challenges have been previously faced by other sectors on their ESG journey. However, unlike manufacturers or consumer goods companies, financial services companies don’t provide physical products. While they can – and must – achieve Net Zero in terms of their operational footprint, true sustainability requires ensuring that clients and customers are also Net Zero. That means leveraging customer relationships and driving ESG impact by changing their behavior and becoming an internal sparring partner to drive transformation, rather than simply excluding certain industries or clients.

HARNESSING THE OPPORTUNITIES

Shaping the future requires financial services companies to take an ecosystem approach that brings together public, private and third- sector partners. In such a complex environment, everyone needs to play a complementary role; however, as in an orchestral performance, it needs to be conducted well for the duration of the concert, with all players displaying commitment and ongoing dedication.

Figure 1 highlights the complexity and diversity of the ecosystems that financial institutions need to play in. These broadly fit into four stakeholder groups, as classified by the UNEPFI:

-

The financial institutions themselves, including employees and partners, as well as the wider financial sector

-

The real economy, such as customers that access and benefit from financial institutions

-

Policymakers and regulators, at both a national and supranational level

-

Science and technology providers delivering solutions for sustainability

FIGURE 1: THE ECOSYSTEM OF FINANCIAL INSTITUTIONS

Achieving success is a long-term process. After the sprint of initial discussions and signing up to commitments, ESG transformation is a marathon.

Senior management in financial institutions therefore needs to focus on transformational change in key areas:

1. Make ESG the board’s top priority

ESG is not just an add-on, but also must be an integral part of the business model. It cannot be siloed or delegated to risk or marketing teams. Financial institutions need to build a clear, credible, and holistic sustainable finance strategy. Mind-sets, culture and conduct must change. Led from the top, this strategy needs to establish the business case and define how the organization will position itself from an ESG perspective. This should also set out risk options, as well as show how technology can be used to mitigate these risks. All of this should be captured in long- and short-term roadmaps for transitioning to a desired ESG state.

2. Prioritize long-term value creation

Ensure that ESG and sustainable finance-oriented strategies and business models prioritize long-term value creation for shareholders and stakeholders, rather than focusing simply on short-term returns for the bank itself. Strategy must be based not on today’s worldview, but on one that will apply in five to 10 years.

It is vital to redefine what success means – moving from measures such as return on equity to look at the bigger picture. Institutions need to adopt a “shared value”-oriented philosophy that takes into account different stakeholders and their needs, as well as incorporating the wider economy and society, remodeling incentives. ESG strategies unlock value drivers that impact the top and bottom line, as Figure 2 demonstrates.

FIGURE 2: ESG AND SUSTAINABLE VALUE DRIVERS

3. Take real action now across your ecosystem

“Wait and see” is no longer a viable option, especially if you want to gain any kind of first-mover advantage. Differentiate by making real commitments that go beyond regulatory bare minimums, build well- resourced ESG capabilities, and put in place the frontline processes to ensure you take action to deliver on them. For example, leading banks are remodeling their relationship management programs to better serve client needs through ESG early-warning and opportunity detection systems that increase transparency over their portfolios.

The sheer volume of risk-tolerant, flexible capital required to drive change goes far beyond the capabilities of a single institution or government. New partnerships – in the public, private and philanthropic sectors – will be required, and all sides will need to work together to define sector-specific pathways to Net Zero. For example, HSBC has launched a Climate Solutions Partnership with the World Resources Institute and World Wildlife Fund to finance companies and projects tackling climate change, backed by USD 100 million of philanthropic funding over five years.

4. Actively drive change in corporate and consumer customers

Financial institutions have the opportunity to build a sustainable, diverse future by becoming a transformation partner of the businesses that they invest in and work with. Effective transformation requires close engagement with clients, to the extent of working alongside or inside companies to ensure they become greener and more sustainable. This approach works better than simply dropping certain types of customers because of their historic record on sustainability.

On the consumer side, banks need to educate customers, building their ESG financial literacy so they are actively seeking out and demanding sustainable financial products, and therefore driving change. Institutional investors are already setting strict targets for ESG compliance – banks need to ensure consumers are applying the same pressure if they are to be seen as relevant and on the side of sustainability. This is particularly important given current excess liquidity levels, high inflation and low interest rates, which are destroying monetary value in real terms. Educating consumers to reallocate their savings to ESG products unlocks major new funding opportunities.

5. Engage with regulators and policymakers early

The financial crisis and other misconduct led to not only greater regulation, but also an adversarial relationship between banks

and regulators. Rather than fighting, financial institutions should demonstrate why they deserve to be involved in setting – and leading – new ways of driving sustainability forward. This requires openness and a change of mind-set. Taking an active role in shaping sustainability policies will allow banks and regulators to jointly define the future rules of the regulatory game, and help move the needle at a systemic level.

Process and pioneers

As discussed in this article, the vast majority of large financial services companies have made long-term commitments to increasing sustainability. Many have also launched specific initiatives:

-

Citi’s USD 200 million Impact Fund invests in companies addressing today’s biggest societal challenges.

-

JPMorgan Chase has set up a Green Economy team to provide dedicated banking services and expertise to companies that produce environmentally friendly goods and services.

-

BNP Paribas has created a 250-person Low Carbon Transition Group to support corporate clients and investors in decarbonizing their exposures.

-

Deutsche Bank has brought forward its target date for deploying EUR 200 billion in sustainable finance by two years to 2023.

However, as with digital disruption, ESG is providing opportunities for fintech start-ups to focus on specific areas and opportunities. Analyst company Medici lists over 150 ESG fintechs in its latest study, covering areas such as ESG-oriented products and services, impact investing, tech/ratings platforms, and inclusion initiatives such as mobile money.

Examples include:

-

Aspiration – a US neobank that does not invest customer money into fossil fuel projects. It currently has over 1.5 million customers for its banking service.

-

MioTech – an AI platform that empowers sustainable finance with ESG data and technology. Investors include Moody’s and Horizon Ventures.

While currently there are no ESG gamechangers that have broken through, this state of affairs is unlikely to last. Traditional players that potentially underestimated the likes of trading and banking fintech Revolut (worth more than Deutsche Bank, Japan Post Bank or UniCredit based on its last fundraising), broker app Trade Republic (valued at over USD5 billion) and payment processing provider Stripe (the most valuable venture-backed private company in the US) should not make the same mistake again.

INSIGHTS FOR THE EXECUTIVE

-

Make ESG real. Move from talk to action. Only then will financial services organizations be able to lead the transformational change that is required to deliver a Net Zero, decarbonized economy and benefit from the opportunities it brings. Failure will open the door to being overtaken by the growing number of ESG start-ups and fintechs, just as slowness to embrace digitization spawned new, disruptive competitors.

-

Make ESG bonuses relevant. Get buy-in from your people by ensuring that compensation and incentives from the board down have a substantial ESG component in order to support culture and behavior change. KPIs have to be clear, concrete and measurable – and focus on what individuals can actually influence through their daily actions. As well as changing incentives, clearly communicate what you expect of your people when it comes to ESG. Model the right behaviors yourself and roll out a code of conduct that makes a sustainable focus the norm.

-

Create an ESG unit with authority, reporting directly to the CEO. Set up a dedicated, well-resourced ESG group, located in the CEO’s office. It should be given sufficient power, cross-business scope and staffing to make a difference. Task this team with neutrally reviewing all ESG exposures with both existing clients and any new products that are launched or customers that are won. Go beyond external requirements with more detailed internal reporting to give multiple ESG lines of defense and position ESG as a differentiator with external stakeholders.

-

Create a clear plan to stop financing non-ESG-compliant business. Turn strategy into practice by reviewing the tools, actions, communications and KPIs of all client-facing business units and ensure they reflect your green objectives. Adjust your investment vehicles to make them ESG led in order to gain early- mover advantage. Bring ESG criteria into know-your-customer requirements to minimize any exposure to uncompliant businesses.

-

Make ESG products part of every customer’s portfolio. Educate consumers and businesses that they need to make ESG products central to their financial strategies. Start young – offer products that let children and their parents invest to build and benefit from a greener world. Don’t just rely on traditional bankers to create new ESG products and services. Bring in outsiders to work alongside them and drive innovative new products and services that will differentiate you going forward.

-

Stop hiding – be transparent. There has been a lot of talk about ESG and a backlash against greenwashers (those that are not as green, but try to ride the bandwagon), transition-washers (less advanced in ESG than they communicate) and competency-washers (less expertise than they claim). Commit to full transparency beyond what is required by regulations and take the lead, backed by the right skills, processes and actions.

-

Become a transformation partner. Ultimately, the only real ESG lever for financial services is to influence clients and their behavior. Move from being on the outside to become an effective internal transformation partner with clients. Only by effectively engaging will customers transform and real ESG impact be delivered.

RELATED INFORMATION

Middle East banks drive growth in ESG finance, face calls for ESG strategy

Financial institutions in the Middle East have adopted environmental, social, and governance (ESG) as a key strategic element in their commitment to going green. As more reporting requirements become…

From green finance to greening finance

Environmental, social, and governance (ESG) provides financial services businesses with a framework for funding and de-risking the shift to a greener world. It offers banks an enormous revenue…

ESG – The irreversible mega-trend

Why ESG and sustainable finance are the new normal for financial institutions Environmental, social, and governance (ESG) and sustainable finance can no longer be thought of as nonessential niceties…