DOWNLOAD

DATE

MEET THE AUTHORS

Contact

In times of energy transition, when intermittent decentralized generation is on the rise and large traditional generation assets are retiring, electricity systems increasingly need flexible solutions to ensure security of supply. Demand side management (DSM) is one such solution which energy firms should have on the radar. Although it can bring tremendous value to transmission system operators (TSOs) and an additional source of revenue for other market players, DSM is still surprisingly underdeveloped in most parts of Europe and beyond. The technical functionality is nevertheless straightforward: by adjusting energy demand when external signals are received, aggregators1 , industrials and even households can provide additional capacity and energy to the market, and be remunerated for it. So what is holding back some markets from unlocking these sleeping buffers in energy systems?

Four categories of DSM incentives are deployed on the international scene today

Two types of external triggers typically create DSM activity: Electricity system supply conditions and electricity market prices. We identify four main mechanisms as the pillars of the DSM market today.

- Wholesale and balancing markets: Access to energy markets to sell energy (or not consume it) in high price periods

- Grid and retail tariffs: Tariffs can vary depending on the time of day or season. Shifting consumption away from high tariff periods can generate savings for industrials or households

- System services: The third mechanism covers primary, secondary and tertiary control services agreed between demand side response (DSR) providers and the transmission system operator (TSO), and is designed to ensure security of supply2

- Capacity markets: Sufficient capacity in the market is guaranteed through contracts established before the target delivery period, with remuneration based on the capacity made available

There is no wrong or right mechanism: generators, aggregators and end users can choose to activate their flexibility based on a price or a system-need trigger. They will favor one mechanism over another, depending on their risk appetite, their capabilities, and their overall ability to deliver.

Even though there is an advantage for participants in DSM to secure additional revenues through contracts, they can be significantly penalized in case of non-delivery, risk which should be minimized by aggregator interventions.

By contrast, with price incentivized response, load is adapted to market or network price signals with a risk of market exposure or imbalance costs. Participants will not receive any payment as such – their reward is in avoided costs, which can be high. However, for industrial players the ability to reschedule production processes in line with grid tariffs or energy tariffs is not guaranteed.

Risk monetization is not the only decision factor for flexibility providers to select one DSM product over another. Indeed, time response, duration of activation, load direction (up or down), frequency of activation per year and availability of load are conditions which can constrain participation in the provision of DSM. For instance, a high number of activations over the same year, especially if in quick succession, will create increasing pressure on the production operations for an industrial and potentially offset a larger portion of the avoided costs than desired. Appropriate valuation of the applicable mechanism is required in order to compensate the related costs and therefore to ensure an appropriate level of participation.

Through various client assignments, we have found that some mechanisms are very well adapted to some production and consumption types – while others are not. The understanding and mapping of DSM mechanisms to flexibility providers’ constraints are key steps to enable optimal value extraction from DSM.

Although regulators and network operators understand the importance of DSM as a new source of flexibility, DSM is still surprisingly underdeveloped in Europe

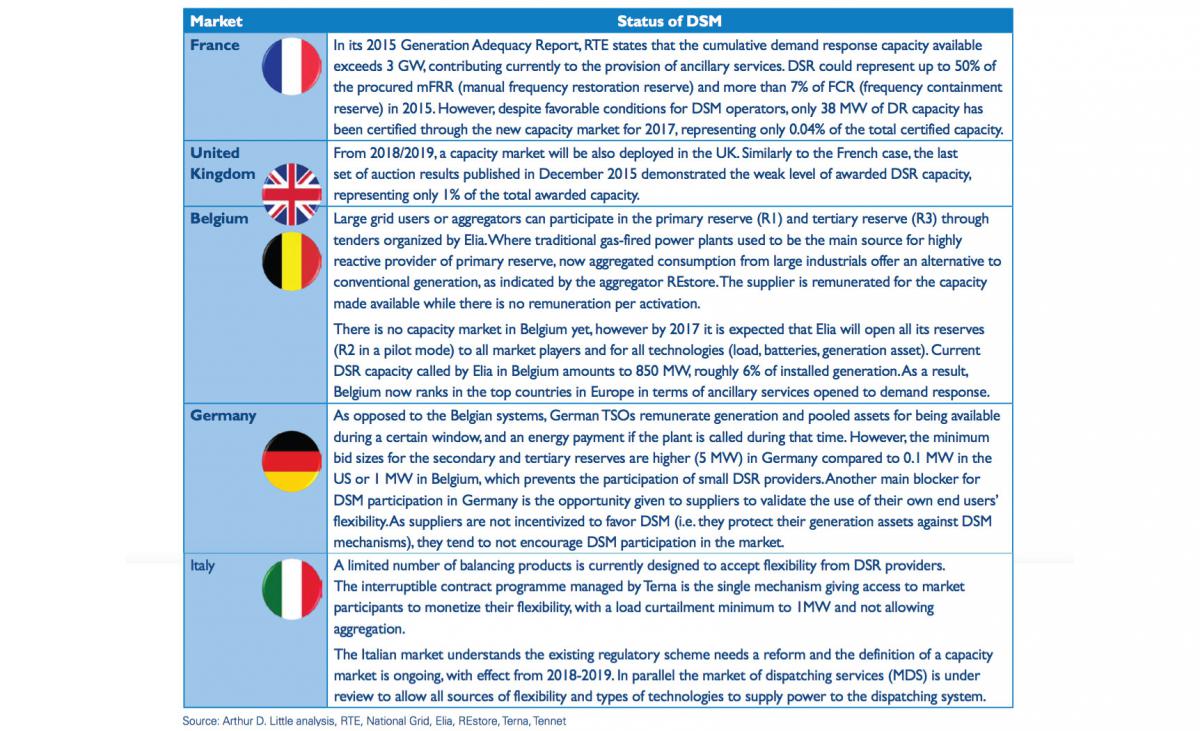

The majority of markets have developed DSM mechanisms, though at very different paces. The United States, supported by state regulators, is undeniably the leader for incentivizing DSM providers to participate in the market. Selected European markets have also embraced the importance of facilitating their access into the energy market to ensure security of electricity supply. However, the examples below in the table illustrate the very slow ramp-up in even the most advanced markets.

DSM facilitation has improved but more can be done

With many energy systems “under stress”, DSM penetration can and should be further stimulated. Not only does it help transmission system operators to manage their networks more effectively (i.e. deferred reinforcement capex, decreased network losses, reduction in costly temporary isolated generation), it also enables utilities, aggregators and electricity users to capture extra value in the struggling electricity markets. Unlocking this value-added requires various initiatives at different levels. Our experience and interactions with TSOs aggregators and industrials allow us to recommend four initiatives to increase participation in DSM:

I. Improve market design

Access to the DSM market must be facilitated via attractive and fair market mechanisms in order to improve the participation of end users and prevent discrimination between actors in the energy value chain. This is one of the key barriers in those markets where DSM penetration is low. The main actions here for TSOs and regulators should be:

- Treat demand side management on equal and transparent terms with generation in the provision of ancillary services and in capacity markets; and design specific mechanisms for DSR providers (i.e. and not to adapt mechanisms that were once designed for generation asset owners)

- Rationalize the number of mechanisms to limit overlaps, and therefore cannibalization, and also to limit their proliferation. Today, it is often difficult for demand side providers to identify which products are suited best to their operations

- Create viable and tailored products that enable aggregators (and their users) to unlock the real potential of demand response in the market

- Appropriately incentivize risks taken by utilities and industrials

- Develop specific value propositions to be put forward to the regulator if room for demand response in the market has not yet been created via regulation

- Create alignment between market players on the baseline methodology to be used to calculate the available load reduction of a given resource to respond to a need for flexibility

II. Educate and support industrials to engage in management of demand

Although the benefits for industrials are real, much more flexibility can be unlocked. Some examples: United Utilities, a UK Water company, stated that it expects to make £5 million in revenue from DSM by 2020 by reducing power usage, including by turning off pumps at its treatment works. REstore, a European aggregator, stated that primary reserve capacities can earn €180k per MW per year in Belgium. Key actions to take (by TSOs, regulators, aggregators, utilities) are:

- Inform and educate industrials about additional revenue streams via demand response, and the economic value proposition. Indeed, industrials active in steel, paper, food & beverage, water treatment, glass industries and others have high interests to reduce their consumption or shift it to another time. Total, ArcelorMittal, Tereos are examples of high energy consumers which became DSR providers

- Support companies to identify adjustable manufacturing processes that are able to free up flexibility for the market when required

- Develop and tailor DSM products and mechanisms that are adapted to a company’s operations, to its risk appetite and to the expected benefits

III. Develop real time price signals

Real time price signals are required to incentivize and trigger DSM activation, but also need to integrate and reflect those activations. This is in the hands of the market manager, typically driven by TSOs:

- Implement time of use tariffs to incentivize shifting of consumption

- Design wholesale markets (day-ahead and intraday markets) capable of sending real time price signals for unlocking flexibility when required

IV. Collaboration of aggregators and energy suppliers

Partnerships between aggregators and energy suppliers can bring high added value although their implementation will only be possible in the absence of conflict of interests. Aggregators’ DSM technical knowledge and their capacity to advise industrials on shifting or reducing the consumption of their production assets, associated with the existing customer portfolio of energy suppliers, jointly work to the advantage of the industrial player by easing market access for them and enabling optimal leverage of the know-how each party brings to the table.

In addition to the above recommendations, infrastructural and technical solutions in support of demand response can be envisaged to facilitate reactivity and availability of assets.

We distinguish battery storage as one of the domains that is gaining more and more popularity across the energy value chain, and can be part of the answer to decrease risks on the DSM provider side and increase responsiveness. Alternatives like distributed generation and electric vehicles are other means to bring generation up or demand down to satisfy grid constraints. Positioning and subsidies from the EU and regional regulators are expected by various market parties in Europe, and should be part of the solution to facilitate and increase demand response usage in grid balancing.

Conclusion

Aggregators, energy suppliers and electricity network operators have demonstrated in a few European countries their willingness to rely on end users’ flexibility to respond to grid needs. So far, with great success, but still somewhat limited in scope.

The understanding of needs and constraints of DSM providers is, however, required to design the market appropriately in a way that will facilitate and increase flexibility activation.

On one hand, TSOs need to design and propose a range of simple mechanisms adapted to their real needs and to DSR providers constraints and expectations in terms of incentives, with a limited impact on operations and certainly not acting as a penalty for the DSR provider. Another critical activity here is to educate the market accordingly.

On the other hand, aggregators, integrated utilities and end users need to define their strategy to seize the “DSM business potential”. The value proposition needs to combine the additional revenues (upside) with pro-actively managing complexities and risks (technical and business constraints). In this, an openminded exchange with grid operators and regional regulators should aim to then converge into a clear setting out of the requirements to facilitate DSM deployment in regional markets.

The challenge will be to define a tailored and non-discriminatory solution for all flexibility owners along the energy value chain, sharing different expectations. Since real cases have proven to be beneficial for a broad range of stakeholders, capturing this value in the energy markets is definitely a prize worth active pursuit.

Unlock a Powerful Difference

RELATED INFORMATION

Arthur D. Little and iKnow

On May 6th 2015, iKnow-Who and Arthur D. Little announced their new partnership during an Extreme Innovation event held at the Turning Torso in Malmö, Sweden. The event, which hosted more than 35…

Taking demand-side response to the household level

Within an extremely limited period and without a break, Europe — and the world as a whole — is undergoing the second consecutive major shock spanning geographies and industries. Both businesses and…

Virtual Power Plants – At the heart of the energy transition

Energy utilities are evolving towards greater reliance on flexibility to respond to an increasing supply-and-demand imbalance. In that context, the role of aggregators has become predominant in…