DOWNLOAD

DATE

MEET THE AUTHORS

Contact

In the last two decades all OEMs have found new space for growth by leveraging additional revenue streams that addressed downstream business and ancillary products and services. They realized that even though they were massively investing in marketing and sales activities that attempted to influence consumer perceptions in order to generate sales opportunities, they were achieving only 40% of customer spending.

At this time the situation has improved, but not changed significantly. The average customer share of wallet for many players in the industry reached a ceiling of around 55–60%. Nevertheless, further growth space can be found by hitting a higher share of overall customer spending and finding a better trade-off between volume and profit in mature markets. Arthur D. Little has identified and tested four pillars to unleash the full potential of the market, generating 5–6% of total revenue growth and from 4–5% profit increase. Transaction price optimization and value-based bundling are, among others, the most influential levers.

However, OEMs must be ready to transform their marketing and sales functions in HQs and national sales companies to benefit the most from our approach and make results sustainable in the long term.

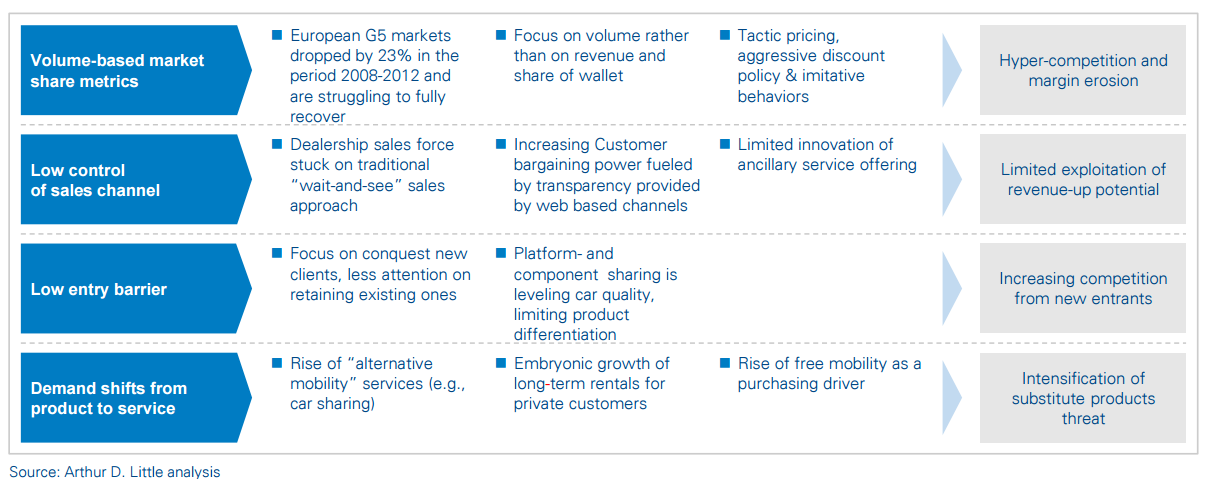

Four forces are threatening OEMs’ growth

Sales decline led automotive players to overreact in order to maintain volumes and market share, the sector’s historical metrics of success, which intensified the price war. OEMs tend also to imitate each other on short-term tactical promotions, increasing variable monetary expenditure to support dealers in achieving sales targets. Their focus remains on volumes instead

Four forces are threatening OEMs’ revenues and profit growth in mature markets

of trying to capture more revenues. These practices are eroding companies’ operating margins, limiting the benefits from the recent market recovery.

OEMs are losing control of sales channels too. The rise of digitalization, smartphones and social media has narrowed most information asymmetries, increasing customers’ bargaining power, since they can easily collect product and service information and compare competitors’ offerings and pricing in advance before visiting dealers for quotations.

Despite the more open and collaborative customer behavior, dealer salespeople still employ a traditional engagement approach, remaining hostage to customers and focusing attention on discounts to survive. With this approach they lose the opportunity to leverage customer proximity to sell more products and services. Furthermore, all ancillary products and services, sold together with the car, such as financing, insurance and extended warranties, are up against indirect competitors. Commercial banks and insurance companies are persuading salespeople with generous rewards to propose “non-captive” products and services.

Shared platforms, power train and components are commoditizing the core product: the “car”. The traditional product differentiation strategy, based on car features and performance, is becoming ineffective, which is exposing market leaders, especially for volume brands, to aggressive new entrants.

Unlock a Powerful Difference

RELATED INFORMATION

Unlock the hidden value of infrastructure

Airports, PT stations, railway stations, stadiums, highways, clinics and hospitals are diversifying their activities in retail and services to secure sustainable new growth relays and enhance…

Mastering customer retention

Profitable growth is a key topic for all insurers in all geographies. Traditionally, insurers have focused on maximizing new sales: new products, channels, segments, incentives, and so on. But over…

Creating Customer-Oriented Companies

If you had invested in an index mutual fund pegged to the Standard & Poors 500 at the beginning of 1990, you'd have done very well. But if you had invested in a fund consisting of companies that…