Ownership model of the future or marketing stunt?

The automotive and mobility market is in a state of flux. As new technologies give rise to innovative products and services, customer mobility demands are changing, forcing the industry to rethink its sales models and explore new concepts. While the possession of a car remains important for many, service-oriented offerings are expected to hold significant growth potential. Moreover, the ongoing economic turmoil is increasing customers’ tendency to opt for risk-reduced, flexible usage models. Today’s car subscription schemes offer a high degree of flexibility and are getting introduced by automotive OEMs, rental companies, and disruptors. Yet how do these car subscriptions differ from existing rental or leasing and financing offerings, and what is their true market potential?

Forms of car usership and trends

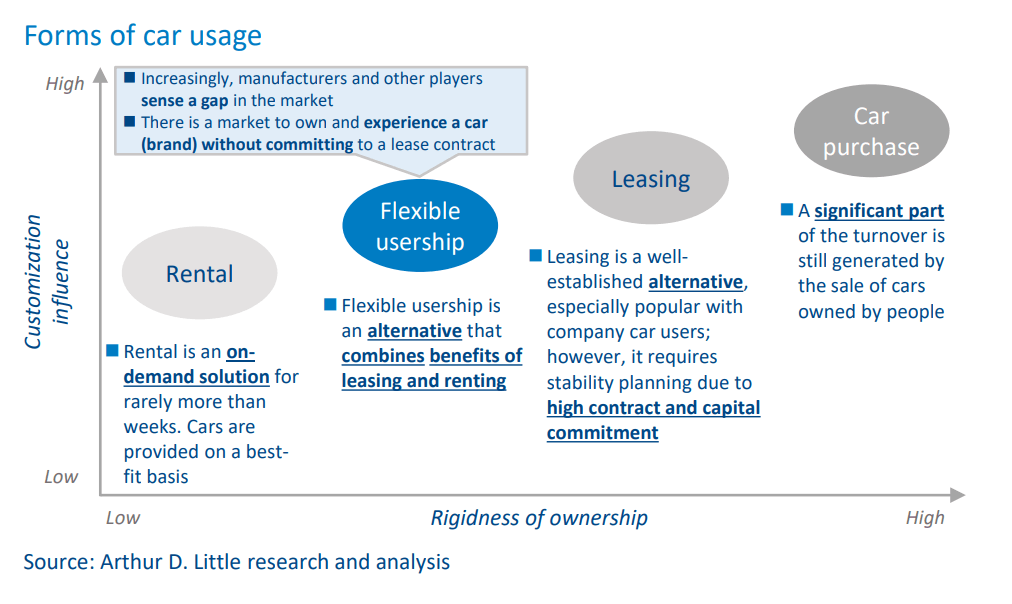

Beyond mere ownership, flexible forms of car use have emerged over the decades, from renting to leasing. Yet a gap remains in terms of customization and flexibility (see figure below).

Subscriptions target this gap, with pioneers having primed the market to some degree and the following key drivers supporting the offering:

- Use instead of own. Sociocultural factors, such as increasing environmental awareness, urbanization, and reduced importance of car ownership as status symbol, are leading consumers to ask for alternative mobility solutions over buying a car.

- Demand for convenience, flexibility, and customization. Customer needs vary. Therefore, a more fluid form between renting and leasing offers a better fit for many.

- Digitalization as enabler of new business models. Digitalization facilitates the development of efficient and innovative services and enables new business and operating models.

Car subscriptions on the rise

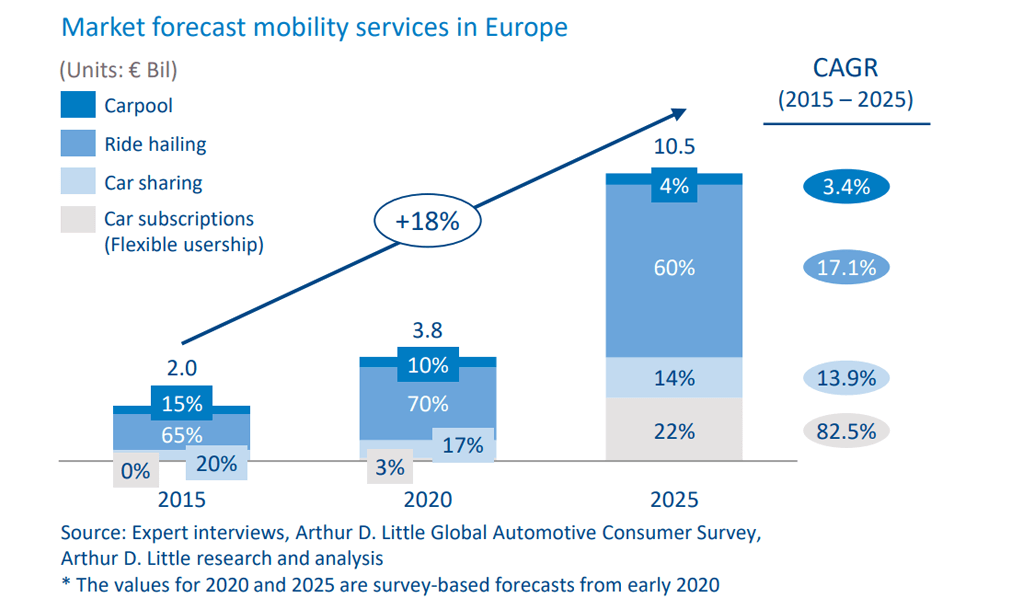

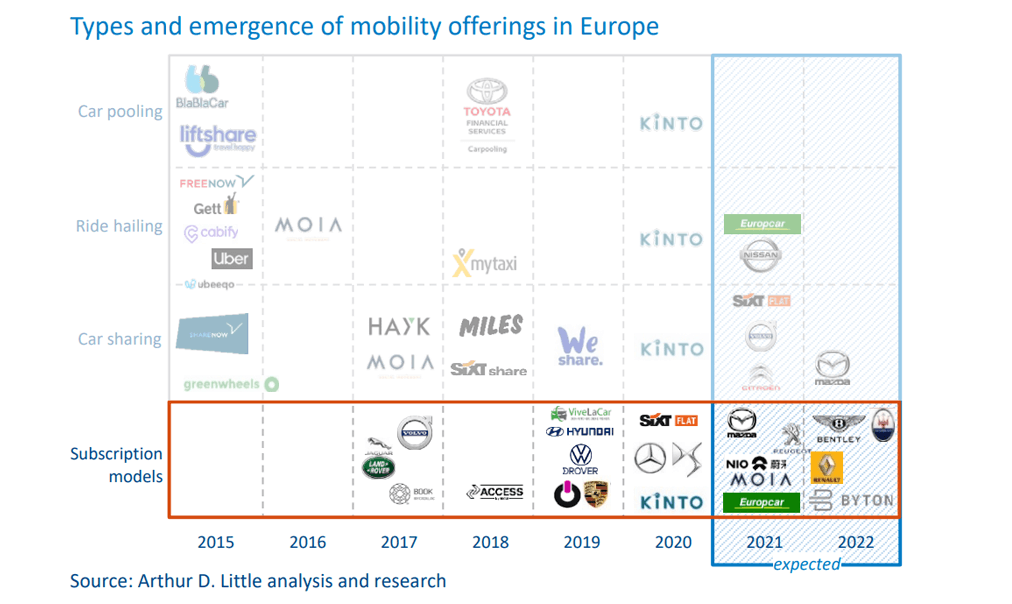

Subscription offerings are well established in many industries – whether it is software, media streaming, or mobile phone contracts. In today’s automotive industry, however, this pricing model only represents a niche product within the mobility-asa-service (MaaS) segment, with a market share of about 3%. Ride hailing still accounts for the largest share. Car subscriptions (flexible usership), by contrast, are set to be the fastest-growing service over the next five years (see figure below).

Differentiating service or marketing stunt?

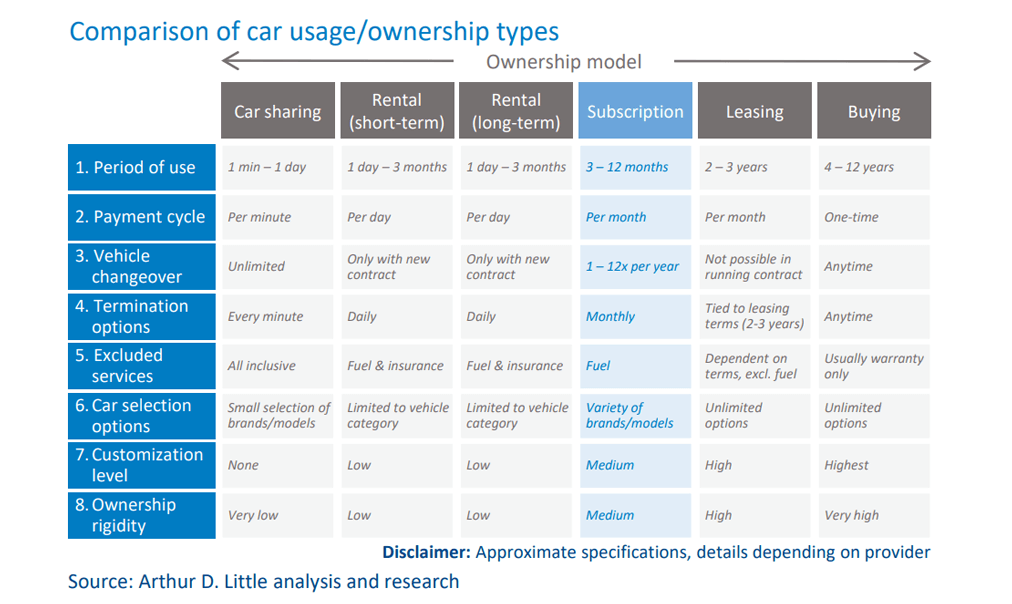

At first sight, subscription models appear highly attractive from the customer’s point of view. Especially in times of economic uncertainty and ever-changing mobility trends, these models match well with risk-averse customer groups that wish to remain flexible. On closer examination, however, other traditional offerings (e.g., long-term rental or leasing) reveal similar features (see figure below). So how do car subscriptions really differ from these offerings, or are they just a marketing stunt designed to appeal to a younger clientele?

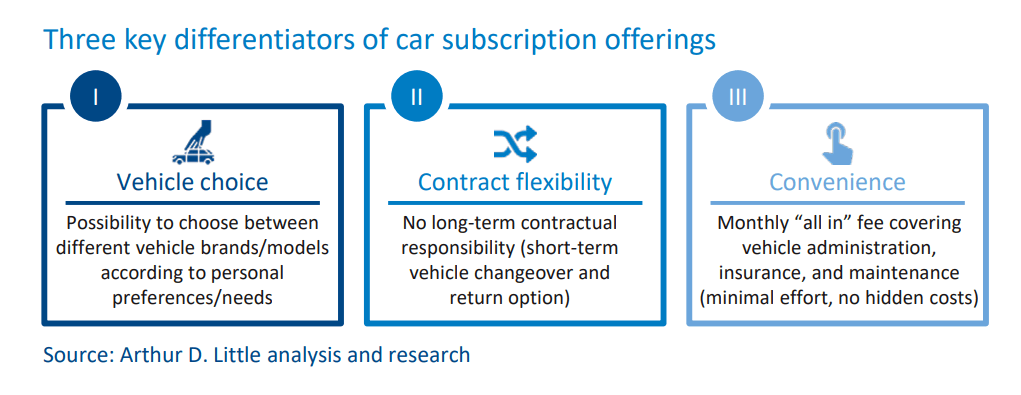

While it is true that car subscription services overlap with other MaaS offerings in certain aspects, they do have their raison d’être. Three key differentiators (see figure below) illustrate how subscription schemes bridge the gap between long-term rental and leasing:

- Vehicle choice. A subscription model allows customers to choose a specific vehicle, as opposed to a rental model, which only allows for the selection of a vehicle category. The choices range from configuring a new car, to choosing from an existing pool of available vehicles, to additional services (e.g., more comprehensive insurance cover). In addition, the possibility to change the make or model of the car according to personal needs and preferences, while staying within the same contract and operator, further increases attractiveness.

- Contract flexibility. Car subscriptions offer customers maximum flexibility. In contrast to leasing or long-term rentals, car subscriptions eliminate the need for long-term contractual commitment and thus ownership rigidity. The vehicle can usually be changed during the contract period or the contract terminated at short notice.

- Convenience. Car subscribers do not need to worry about additional efforts typically associated with owning a car. Instead, they can simply select and book their preferred car online, while the provider takes care of the formalities (e.g., vehicle registration and maintenance). The customer pays a monthly “all in” fee with no hidden charges, usually only excluding fuel charges. Thus, subscribers neither have to go through detailed car configurations nor arrange the used car sale at end of ownership.

Numerous players entering the MaaS market

As car subscriptions offer a promising opportunity to satisfy customers’ growing desire for flexibility, various players have positioned themselves in the ecosystem with varied offerings (see figure below).

While established OEMs such as Porsche or Volvo leverage their brand image to reach new customers and thus tap into new revenue streams through subscriptions, new digital disruptors such as Fair and Cluno are gaining ground by offering a variety of brands and car models as part of their subscription business. Moreover, traditional car rental companies like Avis or Sixt are entering the market, benefiting from their high geographical coverage, existing branch network, and large customer base. Together with these assets and the existing car fleet, they create synergies that give them a distinct advantage in the business.

How to set up the right business model?

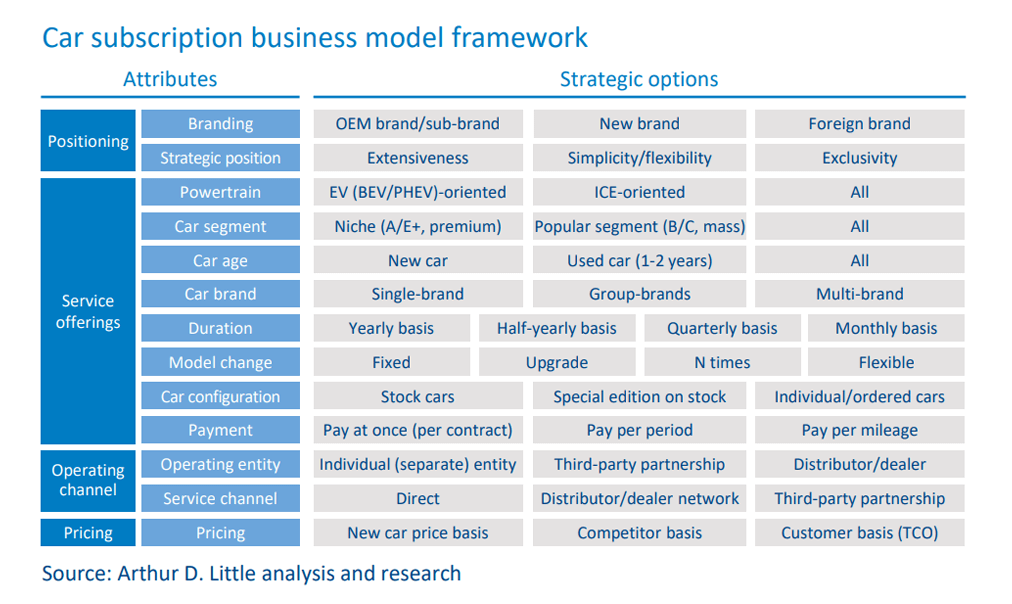

Due to the diversity of MaaS market players and their different approaches, it becomes clear that the range of options for a car subscription model are broad. Many decisions must be made, starting with branding, strategic positioning, and pricing – all the way to the sales and distribution channels as well as the operational units and the powertrain technologies offered (see figure below). Since almost all players are active in other areas of MaaS, synergies with existing services should be evaluated to optimize the vehicle lifecycle value.

Considering the overall strategic direction of the company, the specification of the subscription business model requires the involvement of many stakeholders in the organization and entails a thorough assessment of current capabilities and potential synergies with existing products.

Making car subscriptions profitable

For consumers, car subscriptions can be an economically attractive alternative to leasing, buying, or renting. Yet, at the same time, they must also represent a comparably sound and profitable option for the provider to ensure a sustainable uptake of such models in the future. Experience from business cases with subscription models shows that each scheme must be evaluated individually, based on regional market specifics and customer preferences. Nevertheless, there are some critical levers to optimize economic results:

- Contract flexibility. Customers lean toward subscriptions to increase their flexibility compared to leasing or buying. Changing the vehicle is a cost driver and less demanded than expected. Customers looking for new vehicles every three months can opt for long-term rental offerings. Those that have individual mobility needs (e.g., weekend travel) can be offered upgrade options, including short-term rental. Decisive for customers is the opportunity to end/change the contract more flexibly than leasing (i.e., on a monthly basis).

- Utilization. Maximizing the financial return from a vehicle requires an optimized “time under contract” and minimized changeover, refurbishment, transport, and idle times. This demands a professionalized back-end service infrastructure to handle large fleets with higher turnover rates than in traditional leasing business. Leveraging the know-how and structures of a rental operation is an advantage. Synergies to adjacent MaaS offerings need to be realized.

- Positioning and pricing. Customer preferences for increased flexibility should be reflected in a balanced pricing compared to leasing and rental. Premium features should be flagged and priced as extras to the base subscription. This can include shorter contract durations, more vehicle options, and upgrades to convertibles, sports cars, or transporters.

- Vehicles. Depending on whether an offering involves brandnew vehicles that can be individualized by the customer, standardized new vehicles, or young used cars (e.g., company cars or leasing returns), each approach impacts the subscription model business case differently. There is no universal right or wrong. OEMs must consider the total customer lifetime value, residual values, production utilization, and sales performance in channels (e.g., rental or leasing) and weigh offered services versus occurring costs.

Key challenges for operationalization

Revenue optimized vehicle lifecycle management

One challenge that is complex to master, but decisive for profitability, is the asset, revenue, and lifecycle management of the vehicles utilized for the car subscription. Most of today’s players, especially car manufacturers, obtain vehicles for subscriptions largely from a pool of former company cars or early leasing returns. Sub-brands of OEMs (e.g., KINTO, the MaaS sub-brand of Toyota) often lease vehicles directly from the parent company. Although we see a clear trend toward used cars among car subscriptions, new vehicles can nevertheless offer competitive advantages, such as the ability to exploit sales margins, a lower risk of default, compensation for lost revenue during economic downturns, and the ability to charge “first-time users” for a new car.

Conflict with existing sales structure

MaaS offerings, including car subscriptions, often challenge the established sales organization. Independent dealers want to preserve their established business model while maintaining the customer interface. Thus, dealers need to be carefully integrated into the business model to fully support it. Our experience shows that dealers likely neglect the promotion of MaaS offerings while influencing customers in favor of traditional vehicle offerings. Various options for addressing this issue emerge. As discussed in our 2020 Viewpoint “Future car sales – how to go direct,” new mobility offerings like car subscriptions are a good strategic entry point for direct and online sales models and thus reduce dependence on dealerships. The second option alongside the use of existing sales structures is to establish partnerships with third parties. These can include sales, maintenance, and repair services. A combination of direct sales with efficient fulfillment partnerships can also be a viable approach.

Demarcation and cannibalization of leasing and financing

Another challenge often leading to friction within the organization is the demarcation and cannibalization of leasing and financing offers. Organizational measures can help in this case. Either the responsibility for car subscriptions lies explicitly with the responsible unit for leasing and financing, or they are kept entirely out of the strategy and implementation processes. In our experience, with any overlapping product/service solution, conflicting interests inevitably lead to friction between parties involved, which must be actively managed.

Single or multi-brand approach

Multi-brand OEMs must decide whether they offer multiple brands in a single offer. Sub-brands tend to prefer an individual solution that matches their brand perception. However, in our experience, the synergies from marketing vehicles of different brands combined with an extensive product lineup outweigh the risk of a diluted brand perception. When positioning of a group’s brands are very different, as in the case of VW Group and Porsche, an individual brand solution can still be beneficial.

Conclusion and outlook

Car subscriptions bridge the gap between leasing and rental. They offer high flexibility and reduce risk, commitment, and rigidity inherent in car ownership. This has proven particularly attractive in times of economic uncertainties and primarily targets a younger, up-and-coming clientele. However, subscription models must be well marketed and positioned, as the increased flexibility leads to additional complex processes, demanding a higher price point than traditional leasing offers.

Multiple players with different backgrounds, from digital disruptors and rental companies to established multi-brand OEMs, are pushing into the market. While rental companies can realize considerable synergy potential with their existing business, OEMs may explore and pilot new online-focused direct sales models and third-party partnerships, especially for fulfillment processes.

The key is a business model that aligns with the company’s capabilities and positioning while addressing branding, service offerings, or lifecycle and asset management of the vehicles. The business model must also ensure profitability by calibrating key levers, such as vehicle utilization, changeover, and car selection. Operationalization challenges, which often originate within the company itself, require smart and pragmatic solutions.

Although car subscriptions currently represent only a niche among MaaS offerings, they have significant growth potential due to changing customer preferences. It is now time to make strategic decisions on how to shape this business.

Unlock a Powerful Difference

RELATED INFORMATION

Transforming car sales in a perfect storm

The effects of the COVID-19 crisis on automotive markets highlight the fragility of the traditional car distribution system and intensify the existing need for change. Ongoing transformations such as…

Powering up India’s used car market

The used car market is likely to reach approximately US $80 billion in the next five years and is witnessing increased formalization, with technological advancements reducing traditional friction…

CAR-T on site: Forgoing the extra mile

CAR-T (chimeric antigen receptor T-cell) therapy involves the use of genetically re-engineered versions of a patient’s own T-cells to find cancer cells and defeat them. As of March 2020, there are…