Arthur D. Little has already analyzed and reported the evolution trends in traditional and innovative powertrain technologies. In this report Arthur D. Little provides its perspective on the present and future of fuel cell vehicles (FCVs), providing a synthetic comparison with other technologies, as well as an overview of FCV benefits and the main obstacles to their adoption

Fuel cells are an expected market trend

FCV sales volumes are expected to be significant, but only in the long term, even with a favorable climate-policy scenario. Due to a recognized absence of CO2 emissions during vehicle operation, expectations of the future FCV market are growing following the adoption of the Paris Agreement. The agreement for the first time brought all nations into a common cause to undertake ambitious efforts to combat climate change.

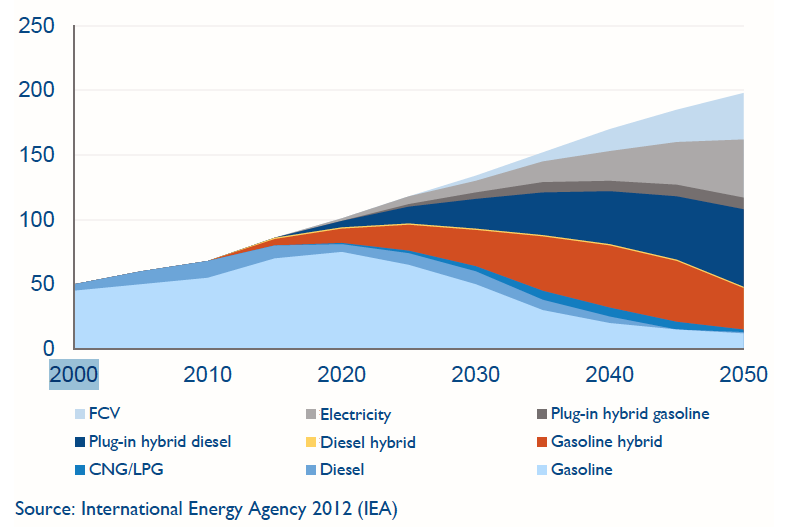

FCV sales volume predictions based on long-term powertrain mix scenario (Mln units)

Within a similar scenario, the international energy agency (IEA) estimates an FCV market share of about 17% by 2050 (35million annual unit sales).

Yet will hydrogen fuel cells fully demonstrate their benefits when the uptake scenario is still uncertain?

The slow FCV uptake will mainly be due to:

- OEMs’ need to achieve significant cost reductions.

- Market need of network infrastructures to build and localexperiments that have proven successful.

- Time required to identify and standardize the most efficientsolution for hydrogen production.

The role of public administration

To promote FCVs and break the initial impasse, various policy options could be evaluated:

- Government support through research, development, and deployment initiatives and grants (e.g. for building out the infrastructure for hydrogen distribution).

- Tax and/or subsidy policies to reduce the high initial cost of FCVs compared to conventional vehicles – directed at either consumers or manufacturers of FCVs and H2 suppliers.

- GHG reduction policies. For example, setting targets for GHG intensity for the entire transportation fuel supply.

Unlock a Powerful Difference

RELATED INFORMATION

Petroleum refiners and shippers struggle over marine fuel

The marine-fuel sector is facing lower-sulfur-content specifications, with the major change taking place in January 2020. Both petroleum refiners and ship owners could contribute to close the supply-…

The metaverse: What’s in it for telcos?

The Metaverse is a megatrend, presenting both a challenge and an opportunity for the telco industry. While some have dismissed it as a passing fad, we believe the Metaverse: (1) necessitates…

Mobile NFC – what’s all the hype about

Mobile Near Field Communication (NFC) has been discussed intensively over the past 24 months. Various players have geared up to enter the different market segments. Billions of dollars are at stake,…